Advertisement

- Germany

- /

- Other Utilities

- /

- DB:MNV6

Don't Race Out To Buy Mainova AG (FRA:MNV6) Just Because It's Going Ex-Dividend

It looks like Mainova AG (FRA:MNV6) is about to go ex-dividend in the next 3 days. This means that investors who purchase shares on or after the 28th of May will not receive the dividend, which will be paid on the 28th of May.

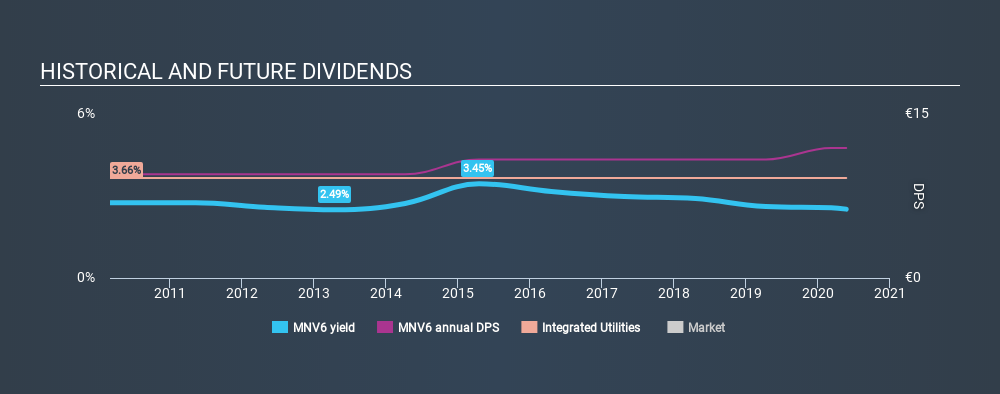

Mainova's next dividend payment will be €10.84 per share. Last year, in total, the company distributed €11.89 to shareholders. Based on the last year's worth of payments, Mainova stock has a trailing yield of around 2.5% on the current share price of €472. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for Mainova

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Mainova distributed an unsustainably high 142% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. A useful secondary check can be to evaluate whether Mainova generated enough free cash flow to afford its dividend. Fortunately, it paid out only 42% of its free cash flow in the past year.

It's good to see that while Mainova's dividends were not covered by profits, at least they are affordable from a cash perspective. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Very few companies are able to sustainably pay dividends larger than their reported earnings.

Click here to see how much of its profit Mainova paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're discomforted by Mainova's 18% per annum decline in earnings in the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Mainova has delivered an average of 2.3% per year annual increase in its dividend, based on the past ten years of dividend payments. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. Mainova is already paying out 142% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

Final Takeaway

Has Mainova got what it takes to maintain its dividend payments? It's not a great combination to see a company with earnings in decline and paying out 142% of its profits, which could imply the dividend may be at risk of being cut in the future. However, the cash payout ratio was much lower - good news from a dividend perspective - which makes us wonder why there is such a mis-match between income and cashflow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

So if you're still interested in Mainova despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. To help with this, we've discovered 4 warning signs for Mainova (2 don't sit too well with us!) that you ought to be aware of before buying the shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About DB:MNV6

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor