Advertisement

Does Recent 23.7% Gain Signal More Upside for Lufthansa in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

If you are weighing whether Deutsche Lufthansa deserves a place in your portfolio, you are not alone. The stock is always a topic among investors who notice its resilience and potential for a rebound. Over the past year, the share price has gained 23.7%, cruising well ahead of broader market worries. While recent weeks have seen a dip of around 5% over both the past 7 and 30 days, the year-to-date gain still stands at a strong 19.2%. If we zoom out even further, the five-year return shows a healthy 40.5% climb, suggesting that investors willing to stomach volatility have been rewarded in the long run.

These moves have not developed in a vacuum. Persistent rumblings about travel demand, shifts in fuel prices, and evolving competitive dynamics can all make shares of major carriers like Deutsche Lufthansa especially interesting. Sometimes, market mood swings around global airlines can feel unpredictable, but these outside factors contribute to both risk perception and the opportunity for significant recovery.

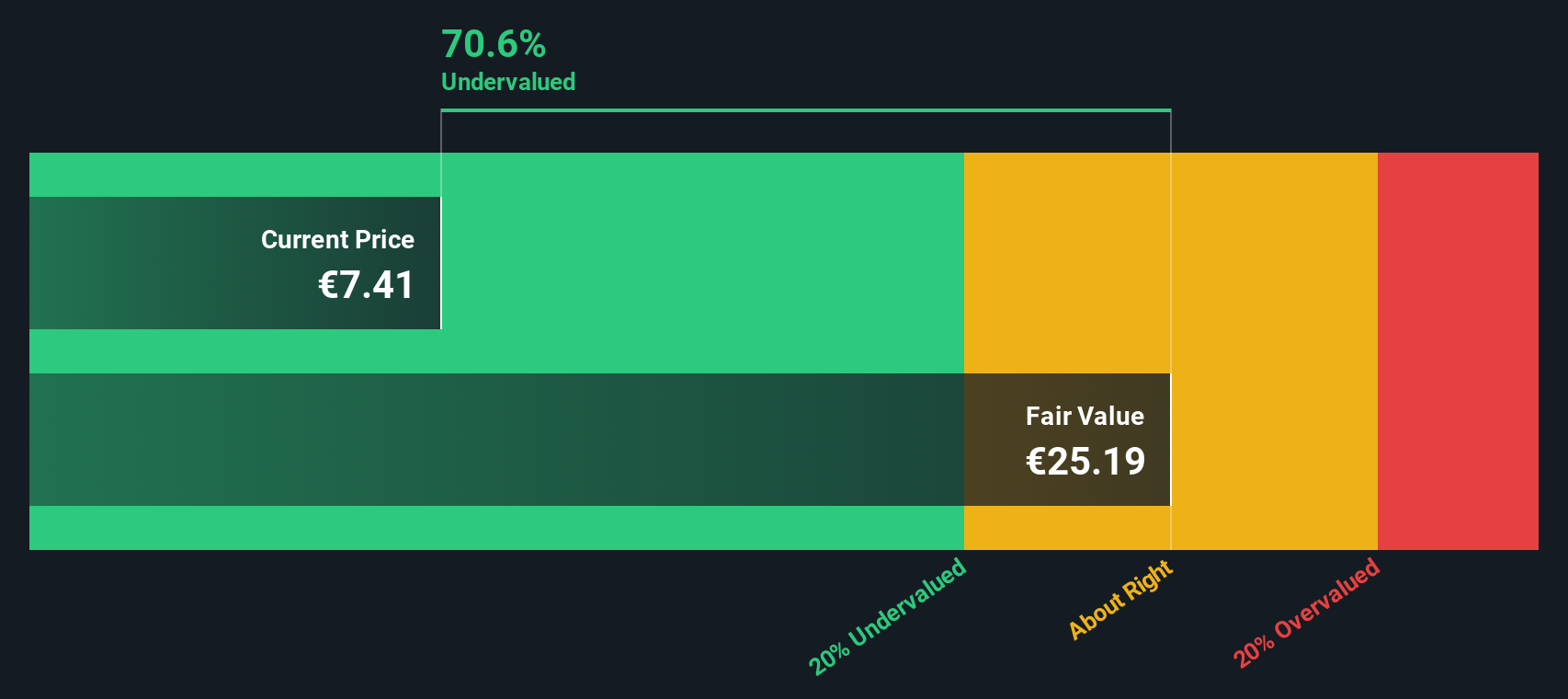

So, is Deutsche Lufthansa undervalued right now? According to a composite valuation score, the company passes five out of six checks for undervaluation, landing it a robust score of 5. That sets the stage for a closer look at how this score is calculated, which methods matter most, and how investors can get beyond the headlines. From traditional multiples to deeper, forward-thinking valuation techniques, let us break down what drives the numbers and why there may be an even clearer picture waiting if you look further.

Why Deutsche Lufthansa is lagging behind its peers

Approach 1: Deutsche Lufthansa Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) method estimates a company's value by projecting its future cash flows and discounting them back to today's value. This offers a forward-looking assessment based on expected profitability. For Deutsche Lufthansa, the current Free Cash Flow stands at €235.1 million, reflecting the operational cash generated over the last twelve months.

Looking ahead, analyst estimates suggest meaningful growth in Free Cash Flow over the next several years. By 2027, projections see Free Cash Flow reaching €1.54 billion. Simply Wall St extrapolations continue this upward trend, forecasting over €1.2 billion per year through 2035. While near-term growth relies on analyst estimates, further projections are based on established trends and industry expectations.

Based on these forecasts, the DCF model derives an intrinsic value of €12.53 per share for Deutsche Lufthansa. With the DCF indicating the stock is trading at a 41.4% discount to this estimated fair value, the implication is that shares currently appear significantly undervalued relative to underlying cash flow potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Deutsche Lufthansa is undervalued by 41.4%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

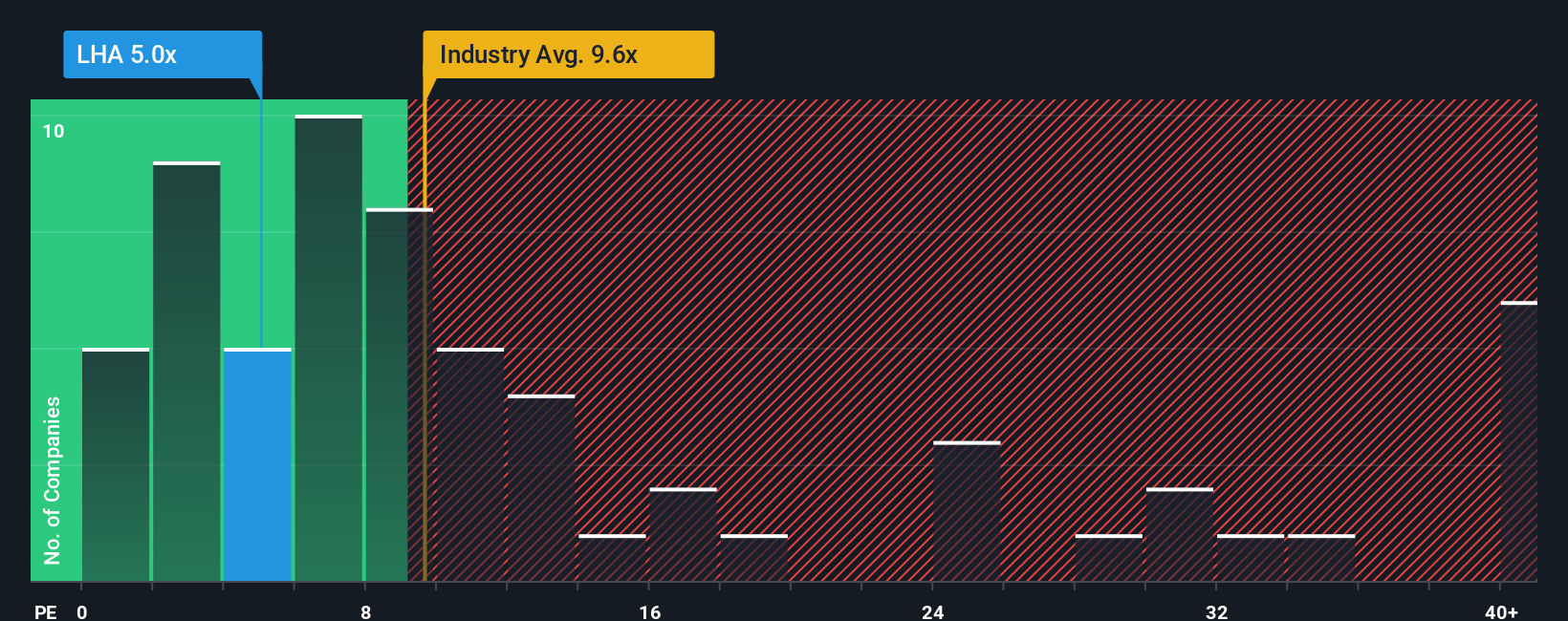

Approach 2: Deutsche Lufthansa Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for established, profitable companies like Deutsche Lufthansa because it ties the company’s share price directly to its actual earnings. This makes it a straightforward way to assess whether a stock is expensive or cheap relative to its profits.

Of course, not all companies deserve the same PE ratio. Generally, higher growth expectations, stronger profitability, and lower risk justify a higher “normal” or “fair” PE, while lower growth or higher risk push it down. That is why context is important when evaluating what a fair multiple should be.

Looking at the numbers, Deutsche Lufthansa currently trades on a PE ratio of just 5x. This is far lower than both the industry average of 9.3x and the peer average of 10.8x, which suggests the market is being cautious or perhaps undervaluing its earnings power. However, Simply Wall St’s proprietary “Fair Ratio,” which incorporates specific factors like the company’s earnings growth outlook, profit margins, risks, industry, and market cap, is 10.9x. This “Fair Ratio” is a more tailored benchmark than basic peer or industry averages and provides a holistic view based on what really matters for this stock.

Since Lufthansa’s actual PE is significantly below its Fair Ratio, the company appears undervalued based on earnings.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Deutsche Lufthansa Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply your story about a company, linking what you think is happening with the business, your expectations for its future growth, and the fair value you believe it deserves.

Unlike traditional models, Narratives begin with your unique perspective. Maybe you see cost pressures rising, or believe in the company’s bold fleet modernization. From there, you can estimate future revenue, earnings, and margins, automatically connecting your story to a financial forecast and a fair value estimate.

These Narratives are easy to create, compare, and update right on Simply Wall St's Community page, a tool used by millions of investors worldwide. They update dynamically as new information such as news or earnings comes in, so your view always stays relevant and informed.

Most importantly, Narratives help you make smarter decisions by letting you compare your Fair Value to the current Price, putting your judgment front and center rather than simply relying on consensus estimates.

For example, looking at Deutsche Lufthansa, some investors see mounting cost pressures and assign a fair value as low as €5.0, while others, impressed by modernization and premiumization, see fair value as high as €12.0. The key is that now, your insight and expectations drive your decisions.

Do you think there's more to the story for Deutsche Lufthansa? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:LHA

Deutsche Lufthansa

Operates as an aviation company in Germany and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor