Advertisement

- Germany

- /

- Wireless Telecom

- /

- XTRA:1U1

Factors Income Investors Should Consider Before Adding 1&1 Drillisch AG (ETR:DRI) To Their Portfolio

Today we'll take a closer look at 1&1 Drillisch AG (ETR:DRI) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

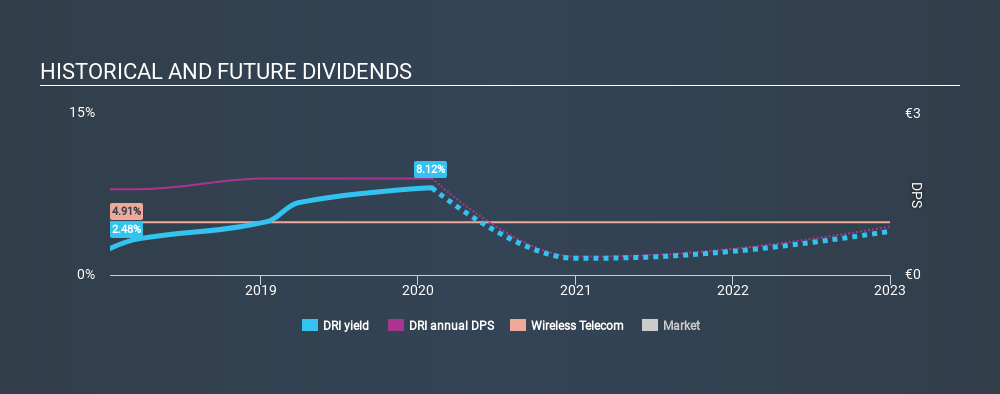

1&1 Drillisch pays a 8.1% dividend yield, and has been paying dividends for the past two years. It's certainly an attractive yield, but readers are likely curious about its staying power. There are a few simple ways to reduce the risks of buying 1&1 Drillisch for its dividend, and we'll go through these below.

Explore this interactive chart for our latest analysis on 1&1 Drillisch!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. 1&1 Drillisch paid out 81% of its profit as dividends, over the trailing twelve month period. Paying out a majority of its earnings limits the amount that can be reinvested in the business. This may indicate a commitment to paying a dividend, or a dearth of investment opportunities.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. 1&1 Drillisch's cash payout ratio last year was 3.6%, which is quite low and suggests that the dividend was thoroughly covered by cash flow. It's positive to see that 1&1 Drillisch's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

While the above analysis focuses on dividends relative to a company's earnings, we do note 1&1 Drillisch's strong net cash position, which will let it pay larger dividends for a time, should it choose.

Remember, you can always get a snapshot of 1&1 Drillisch's latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. The company has been paying a stable dividend for a few years now, but we'd like to see more evidence of consistency over a longer period. During the past two-year period, the first annual payment was €1.60 in 2018, compared to €1.80 last year. Dividends per share have grown at approximately 6.1% per year over this time.

The dividend has been growing at a reasonable rate, which we like. We're conscious though that one of the best ways to detect a multi-decade consistent dividend-payer, is to watch a company pay dividends for 20 years - a distinction 1&1 Drillisch has not achieved yet.

Dividend Growth Potential

Dividend payments have been consistent over the past few years, but we should always check if earnings per share (EPS) are growing, as this will help maintain the purchasing power of the dividend. Earnings have grown at around 5.1% a year for the past five years, which is better than seeing them shrink! EPS have been growing at a reasonable rate, although with most of the profits being paid out to shareholders, we question if the company will be able to keep growing its dividends in the future.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. 1&1 Drillisch's payout ratios are within a normal range for the average corporation, and we like that its cashflow was stronger than reported profits. Second, earnings growth has been ordinary, and its history of dividend payments is shorter than we'd like. Ultimately, 1&1 Drillisch comes up short on our dividend analysis. It's not that we think it is a bad company - just that there are likely more appealing dividend prospects out there on this analysis.

Earnings growth generally bodes well for the future value of company dividend payments. See if the 13 1&1 Drillisch analysts we track are forecasting continued growth with our free report on analyst estimates for the company.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About XTRA:1U1

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor