Advertisement

KATEK SE Beat Revenue Forecasts By 11%: Here's What Analysts Are Forecasting Next

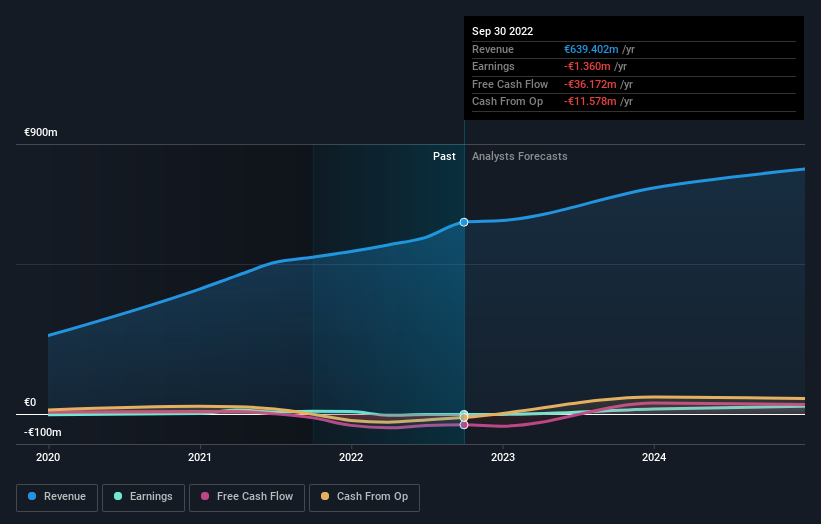

Shareholders of KATEK SE (FRA:KTEK) will be pleased this week, given that the stock price is up 12% to €18.20 following its latest quarterly results. It was a mildly positive result, with revenues exceeding expectations at €180m, while statutory earnings per share (EPS) of €0.70 were in line with analyst forecasts. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Check out our latest analysis for KATEK

Taking into account the latest results, the consensus forecast from KATEK's two analysts is for revenues of €753.6m in 2023, which would reflect a notable 18% improvement in sales compared to the last 12 months. KATEK is also expected to turn profitable, with statutory earnings of €1.25 per share. In the lead-up to this report, the analysts had been modelling revenues of €715.8m and earnings per share (EPS) of €1.23 in 2023. So it looks like there's been no major change in sentiment following the latest results, although the analysts have made a slight bump in to revenue forecasts.

As a result, it might come as a surprise that the consensus price target has been cut 7.7% to €30.00, which could suggest that these earnings are considered less valuable by the market than previously.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that KATEK's revenue growth is expected to slow, with the forecast 14% annualised growth rate until the end of 2023 being well below the historical 26% p.a. growth over the last three years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 11% annually. Even after the forecast slowdown in growth, it seems obvious that KATEK is also expected to grow faster than the wider industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2024, which can be seen for free on our platform here.

It is also worth noting that we have found 2 warning signs for KATEK (1 doesn't sit too well with us!) that you need to take into consideration.

Valuation is complex, but we're here to simplify it.

Discover if KATEK might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DB:KTEK

KATEK

Provides electronics value chain services in Germany, Europe, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor