Advertisement

Viscom (ETR:V6C) Has Some Difficulty Using Its Capital Effectively

What underlying fundamental trends can indicate that a company might be in decline? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. Basically the company is earning less on its investments and it is also reducing its total assets. On that note, looking into Viscom (ETR:V6C), we weren't too upbeat about how things were going.

What Is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Viscom:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

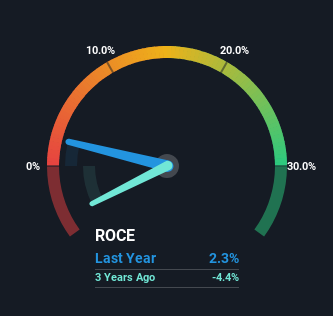

0.023 = €1.6m ÷ (€107m - €40m) (Based on the trailing twelve months to June 2024).

So, Viscom has an ROCE of 2.3%. Ultimately, that's a low return and it under-performs the Electronic industry average of 11%.

Check out our latest analysis for Viscom

Above you can see how the current ROCE for Viscom compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Viscom for free.

So How Is Viscom's ROCE Trending?

In terms of Viscom's historical ROCE movements, the trend doesn't inspire confidence. Unfortunately the returns on capital have diminished from the 11% that they were earning five years ago. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Viscom to turn into a multi-bagger.

On a side note, Viscom's current liabilities have increased over the last five years to 37% of total assets, effectively distorting the ROCE to some degree. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. While the ratio isn't currently too high, it's worth keeping an eye on this because if it gets particularly high, the business could then face some new elements of risk.

The Bottom Line

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. Investors haven't taken kindly to these developments, since the stock has declined 59% from where it was five years ago. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

One more thing, we've spotted 1 warning sign facing Viscom that you might find interesting.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:V6C

Viscom

Develops, manufactures, and sells inspection systems for industrial production applications in Europe, the United States, and Asia.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$467.8% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.1% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.7% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.7% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$0.21.2k% overvalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Delphic on NuScale Power ·

NuScale is Postioned For Long-Term Growth

Fair Value:US$10087.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Argenta Silver ·

Frank Giustra Backed: The High-Grade Silver Project Acquired for Just $3.5M Could Deliver 30x Silver Torque

Fair Value:CA$40.3598.7% undervalued

14 followersusers have followed this narrative

9 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.3% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.1% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22040.4% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative