What TeamViewer (XTRA:TMV)'s Revenue Growth and Lower Guidance Reveal About Its Margin Pressures

Reviewed by Sasha Jovanovic

- In October 2025, TeamViewer SE reported third quarter results showing revenue growth to €189.48 million, but with a decline in net income to €28.65 million compared to the previous year, and subsequently confirmed 2025 full-year revenue guidance at the lower end of its projected range (€778 million to €797 million).

- This sequence of updates gives fresh insight into TeamViewer's ability to sustain top-line growth despite facing bottom-line pressures.

- We'll explore how TeamViewer's confirmation of revenue guidance shapes the investment narrative amid ongoing margin and demand challenges.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

TeamViewer Investment Narrative Recap

To be a TeamViewer shareholder, you typically need confidence in the company’s ability to convert steady demand for remote access and digital workplace solutions into reliable revenue growth, despite the margin and earnings pressures that have continued into recent results. The confirmation of 2025 guidance at the lower end is important for investor expectations, but the immediate impact on the company’s biggest catalyst, cross-selling and upsell from new IT management products, appears limited, while margin compression remains the top risk.

The most relevant announcement to this outlook is the Q3 2025 report, showing continued growth in revenue but with a year-on-year decline in net income and earnings per share. This earnings trend underlines the key challenge TeamViewer faces: converting higher sales into sustainable profit, especially as new offerings like DEX Essentials and TeamViewer ONE are rolled out and begin to influence both customer mix and average revenue per user.

In contrast, investors should be aware that even with improved top-line results, persistent margin pressure from slowing SMB growth still remains a critical risk...

Read the full narrative on TeamViewer (it's free!)

TeamViewer's outlook anticipates €943.2 million in revenue and €199.5 million in earnings by 2028. This scenario is based on a 9.9% annual revenue growth rate and a €73.1 million increase in earnings from the current level of €126.4 million.

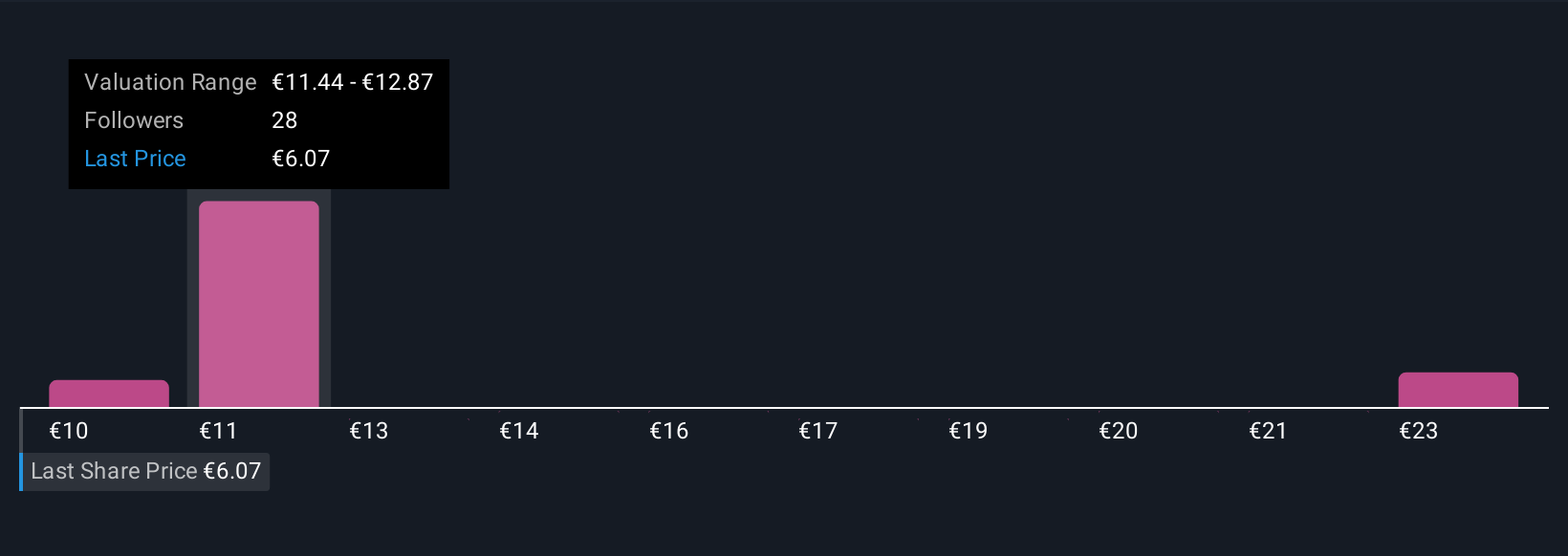

Uncover how TeamViewer's forecasts yield a €12.81 fair value, a 101% upside to its current price.

Exploring Other Perspectives

Nine retail investors from the Simply Wall St Community have fair value estimates for TeamViewer ranging from €10.02 to €23.97 per share. While some focus on long-term opportunities in IT management and remote support, others are cautious about persistent margin and SMB volatility highlighting the value in examining multiple opinions.

Explore 9 other fair value estimates on TeamViewer - why the stock might be worth just €10.02!

Build Your Own TeamViewer Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TeamViewer research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free TeamViewer research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TeamViewer's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TeamViewer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:TMV

Undervalued with limited growth.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion