Analyst Estimates: Here's What Brokers Think Of TeamViewer SE (ETR:TMV) After Its First-Quarter Report

It's been a sad week for TeamViewer SE (ETR:TMV), who've watched their investment drop 19% to €10.90 in the week since the company reported its first-quarter result. Revenues came in 3.6% below expectations, at €179m. Statutory earnings per share were relatively better off, with a per-share profit of €0.76 being roughly in line with analyst estimates. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

We've discovered 1 warning sign about TeamViewer. View them for free.

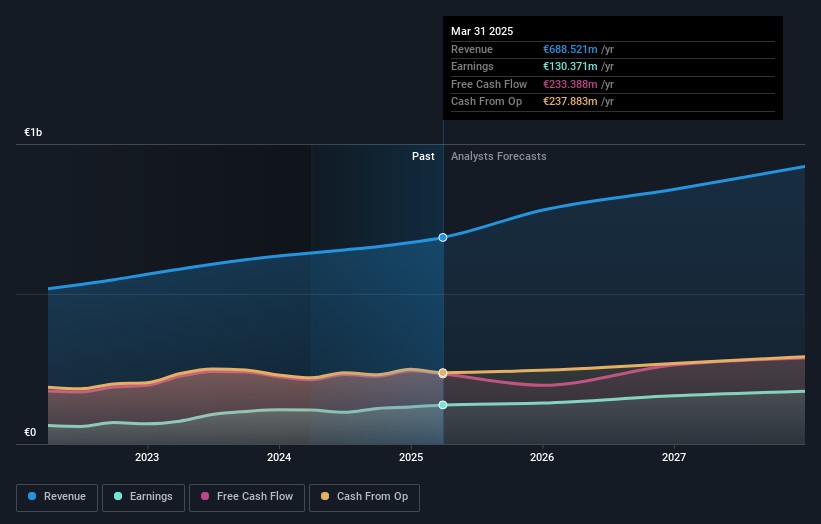

Taking into account the latest results, the most recent consensus for TeamViewer from twelve analysts is for revenues of €779.1m in 2025. If met, it would imply a decent 13% increase on its revenue over the past 12 months. Per-share earnings are expected to accumulate 6.2% to €0.86. Yet prior to the latest earnings, the analysts had been anticipated revenues of €783.2m and earnings per share (EPS) of €0.90 in 2025. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

See our latest analysis for TeamViewer

It might be a surprise to learn that the consensus price target was broadly unchanged at €15.45, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic TeamViewer analyst has a price target of €20.00 per share, while the most pessimistic values it at €12.00. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The analysts are definitely expecting TeamViewer's growth to accelerate, with the forecast 18% annualised growth to the end of 2025 ranking favourably alongside historical growth of 10% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 11% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that TeamViewer is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for TeamViewer going out to 2027, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 1 warning sign for TeamViewer you should know about.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if TeamViewer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:TMV

Undervalued with limited growth.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion