Advertisement

Mid-caps stocks, like Nemetschek SE (ETR:NEM) with a market capitalization of €5.8b, aren’t the focus of most investors who prefer to direct their investments towards either large-cap or small-cap stocks. However, generally ignored mid-caps have historically delivered better risk-adjusted returns than the two other categories of stocks. NEM’s financial liquidity and debt position will be analysed in this article, to get an idea of whether the company can fund opportunities for strategic growth and maintain strength through economic downturns. Remember this is a very top-level look that focuses exclusively on financial health, so I recommend a deeper analysis into NEM here.

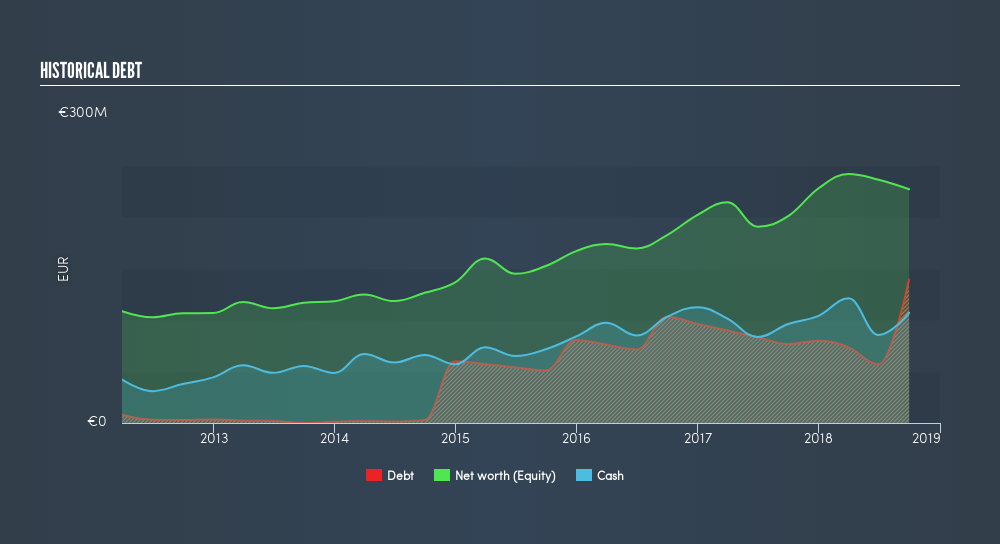

See our latest analysis for Nemetschek

Does NEM Produce Much Cash Relative To Its Debt?

Over the past year, NEM has ramped up its debt from €77m to €139m – this includes long-term debt. With this rise in debt, NEM currently has €107m remaining in cash and short-term investments to keep the business going. On top of this, NEM has produced cash from operations of €101m over the same time period, leading to an operating cash to total debt ratio of 73%, signalling that NEM’s current level of operating cash is high enough to cover debt.

Can NEM meet its short-term obligations with the cash in hand?

At the current liabilities level of €212m, the company arguably has a rather low level of current assets relative its obligations, with the current ratio last standing at 0.86x. The current ratio is calculated by dividing current assets by current liabilities.

Can NEM service its debt comfortably?

With debt reaching 61% of equity, NEM may be thought of as relatively highly levered. This is not unusual for mid-caps as debt tends to be a cheaper and faster source of funding for some businesses. No matter how high the company’s debt, if it can easily cover the interest payments, it’s considered to be efficient with its use of excess leverage. A company generating earnings after interest and tax at least three times its net interest payments is considered financially sound. In NEM's case, the ratio of 188x suggests that interest is comfortably covered, which means that debtors may be willing to loan the company more money, giving NEM ample headroom to grow its debt facilities.

Next Steps:

NEM’s high cash coverage means that, although its debt levels are high, the company is able to utilise its borrowings efficiently in order to generate cash flow. Though its low liquidity raises concerns over whether current asset management practices are properly implemented for the mid-cap. I admit this is a fairly basic analysis for NEM's financial health. Other important fundamentals need to be considered alongside. You should continue to research Nemetschek to get a more holistic view of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for NEM’s future growth? Take a look at our free research report of analyst consensus for NEM’s outlook.

- Valuation: What is NEM worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether NEM is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About XTRA:NEM

Nemetschek

Provides software solutions for architecture, engineering, construction, operation, and media industries in Germany, the rest of Europe, the Americas, the Asia Pacific, and internationally.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor