Advertisement

What Does Destiny Media Technologies Inc.’s (FRA:DME) 26% ROCE Say About The Business?

Today we'll look at Destiny Media Technologies Inc. (FRA:DME) and reflect on its potential as an investment. Specifically, we're going to calculate its Return On Capital Employed (ROCE), in the hopes of getting some insight into the business.

First of all, we'll work out how to calculate ROCE. Next, we'll compare it to others in its industry. Last but not least, we'll look at what impact its current liabilities have on its ROCE.

What is Return On Capital Employed (ROCE)?

ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. In general, businesses with a higher ROCE are usually better quality. Overall, it is a valuable metric that has its flaws. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.'

How Do You Calculate Return On Capital Employed?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Destiny Media Technologies:

0.26 = US$711k ÷ (US$3.1m - US$390k) (Based on the trailing twelve months to November 2018.)

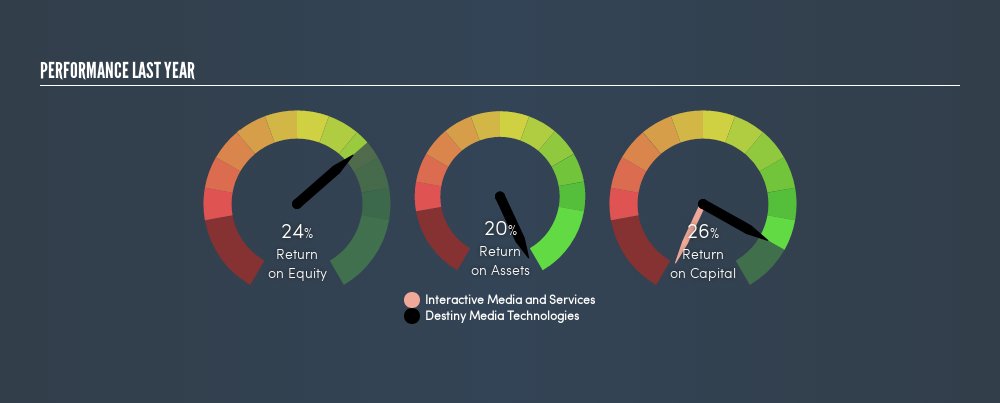

So, Destiny Media Technologies has an ROCE of 26%.

View our latest analysis for Destiny Media Technologies

Is Destiny Media Technologies's ROCE Good?

One way to assess ROCE is to compare similar companies. We can see Destiny Media Technologies's ROCE is around the 26% average reported by the Interactive Media and Services industry. Setting aside the comparison to its industry for a moment, Destiny Media Technologies's ROCE in absolute terms currently looks quite high.

Destiny Media Technologies delivered an ROCE of 26%, which is better than 3 years ago, as was making losses back then. This makes us wonder if the company is improving.

It is important to remember that ROCE shows past performance, and is not necessarily predictive. Companies in cyclical industries can be difficult to understand using ROCE, as returns typically look high during boom times, and low during busts. This is because ROCE only looks at one year, instead of considering returns across a whole cycle. How cyclical is Destiny Media Technologies? You can see for yourself by looking at this freegraph of past earnings, revenue and cash flow.

How Destiny Media Technologies's Current Liabilities Impact Its ROCE

Current liabilities include invoices, such as supplier payments, short-term debt, or a tax bill, that need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To check the impact of this, we calculate if a company has high current liabilities relative to its total assets.

Destiny Media Technologies has total liabilities of US$390k and total assets of US$3.1m. Therefore its current liabilities are equivalent to approximately 13% of its total assets. A minimal amount of current liabilities limits the impact on ROCE.

Our Take On Destiny Media Technologies's ROCE

Low current liabilities and high ROCE is a good combination, making Destiny Media Technologies look quite interesting. Destiny Media Technologies looks strong on this analysis, but there are plenty of other companies that could be a good opportunity . Here is a free list of companies growing earnings rapidly.

For those who like to find winning investments this freelist of growing companies with recent insider purchasing, could be just the ticket.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About DB:DME1

Destiny Media Technologies

Develops technologies that enable the distribution of digital media files in a streaming or digital download format over the Internet.

Flawless balance sheet slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor