Advertisement

- Germany

- /

- Basic Materials

- /

- XTRA:HEI

There May Be Some Bright Spots In Heidelberg Materials' (ETR:HEI) Earnings

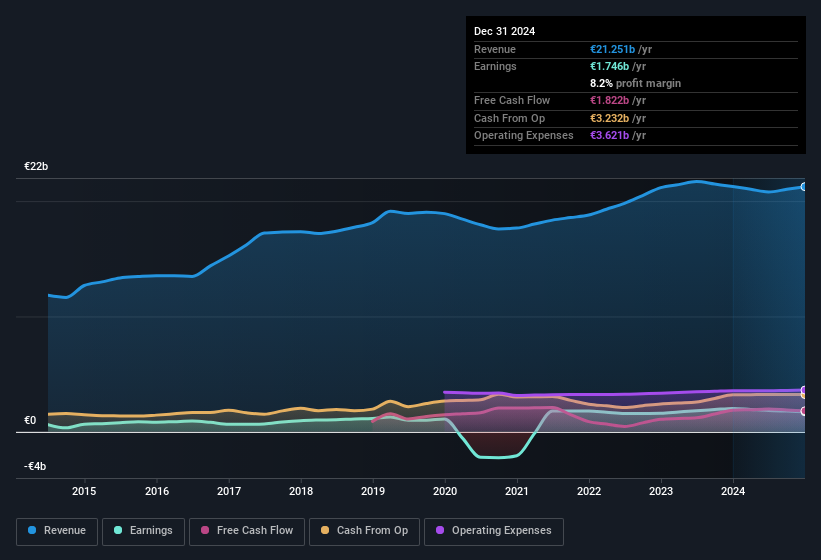

Investors were disappointed with the weak earnings posted by Heidelberg Materials AG (ETR:HEI ). While the headline numbers were soft, we believe that investors might be missing some encouraging factors.

The Impact Of Unusual Items On Profit

To properly understand Heidelberg Materials' profit results, we need to consider the €348m expense attributed to unusual items. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. If Heidelberg Materials doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Heidelberg Materials' Profit Performance

Because unusual items detracted from Heidelberg Materials' earnings over the last year, you could argue that we can expect an improved result in the current quarter. Because of this, we think Heidelberg Materials' earnings potential is at least as good as it seems, and maybe even better! And on top of that, its earnings per share have grown at 5.7% per year over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. So while earnings quality is important, it's equally important to consider the risks facing Heidelberg Materials at this point in time. While conducting our analysis, we found that Heidelberg Materials has 1 warning sign and it would be unwise to ignore this.

Today we've zoomed in on a single data point to better understand the nature of Heidelberg Materials' profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Heidelberg Materials might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:HEI

Heidelberg Materials

Produces and distributes cement, aggregates, ready-mixed concrete, and asphalt worldwide.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor