Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Fresenius Medical Care AG (ETR:FME) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Fresenius Medical Care's Net Debt?

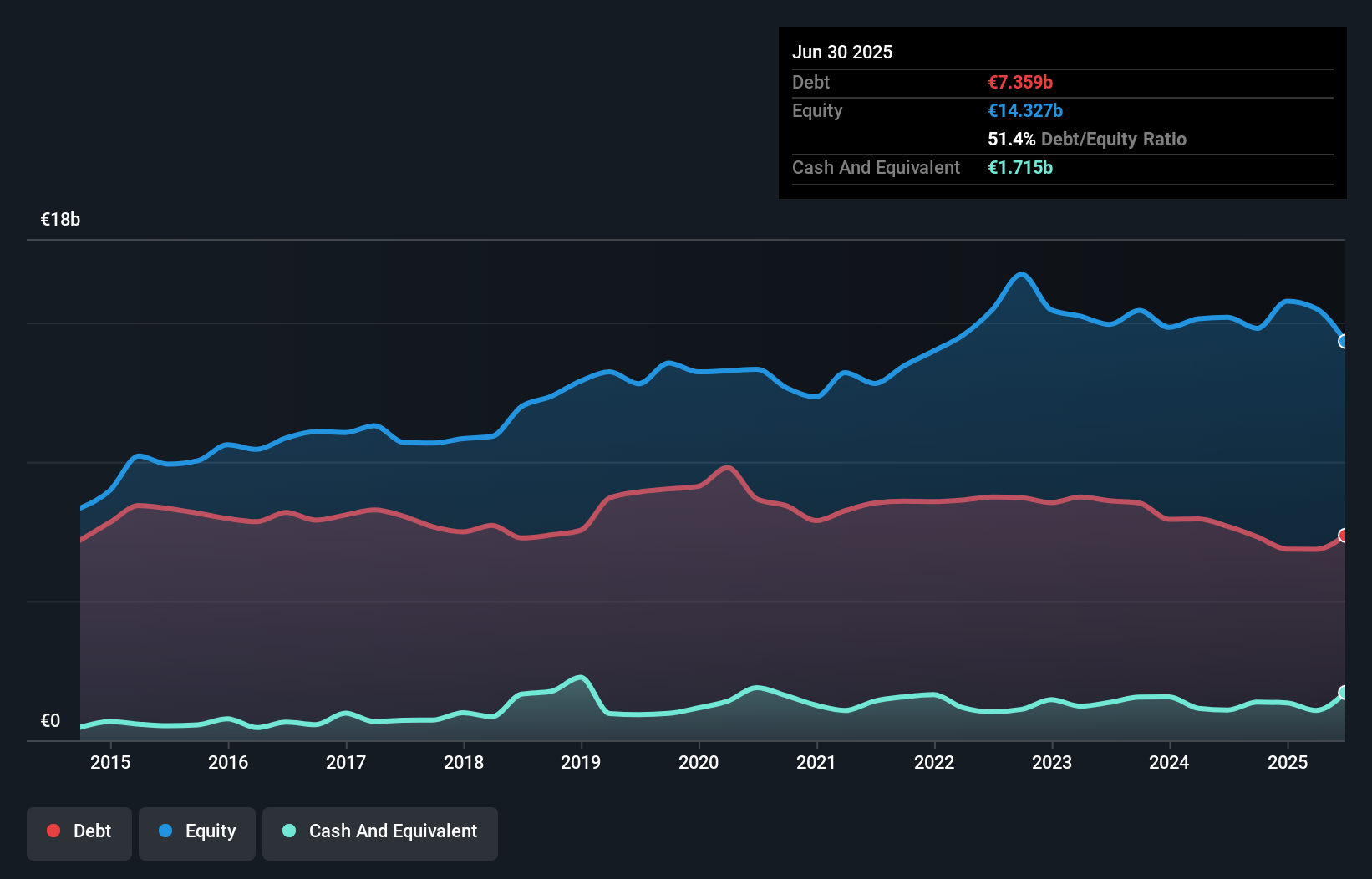

The image below, which you can click on for greater detail, shows that Fresenius Medical Care had debt of €7.36b at the end of June 2025, a reduction from €7.68b over a year. However, it also had €1.72b in cash, and so its net debt is €5.64b.

How Strong Is Fresenius Medical Care's Balance Sheet?

We can see from the most recent balance sheet that Fresenius Medical Care had liabilities of €5.66b falling due within a year, and liabilities of €11.3b due beyond that. Offsetting these obligations, it had cash of €1.72b as well as receivables valued at €3.23b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €12.0b.

This is a mountain of leverage even relative to its gargantuan market capitalization of €12.5b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

View our latest analysis for Fresenius Medical Care

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Fresenius Medical Care's net debt is sitting at a very reasonable 2.4 times its EBITDA, while its EBIT covered its interest expense just 5.0 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Notably Fresenius Medical Care's EBIT was pretty flat over the last year. We would prefer to see some earnings growth, because that always helps diminish debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Fresenius Medical Care can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Fresenius Medical Care actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

When it comes to the balance sheet, the standout positive for Fresenius Medical Care was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. For example, its level of total liabilities makes us a little nervous about its debt. We would also note that Healthcare industry companies like Fresenius Medical Care commonly do use debt without problems. Looking at all this data makes us feel a little cautious about Fresenius Medical Care's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. Given Fresenius Medical Care has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:FME

Fresenius Medical Care

Provides dialysis and related services for individuals with renal diseases in Germany, the United States, and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor