Amidst a backdrop of political uncertainty and fluctuating markets across Europe, Germany's DAX index has not been immune to the pressures, experiencing a notable decline. In such an environment, identifying undervalued stocks becomes particularly compelling as investors look for potential resilience and growth opportunities in less favorable economic conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Germany

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Novem Group (XTRA:NVM) | €5.66 | €10.86 | 47.9% |

| Verbio (XTRA:VBK) | €17.25 | €28.24 | 38.9% |

| elumeo (XTRA:ELB) | €2.44 | €4.77 | 48.8% |

| MTU Aero Engines (XTRA:MTX) | €227.90 | €397.14 | 42.6% |

| Stratec (XTRA:SBS) | €47.35 | €80.11 | 40.9% |

| CHAPTERS Group (XTRA:CHG) | €23.80 | €44.54 | 46.6% |

| SBF (DB:CY1K) | €2.96 | €5.22 | 43.3% |

| Redcare Pharmacy (XTRA:RDC) | €116.30 | €197.69 | 41.2% |

| Your Family Entertainment (DB:RTV) | €2.42 | €4.08 | 40.6% |

| Dr. Hönle (XTRA:HNL) | €19.85 | €33.15 | 40.1% |

We're going to check out a few of the best picks from our screener tool

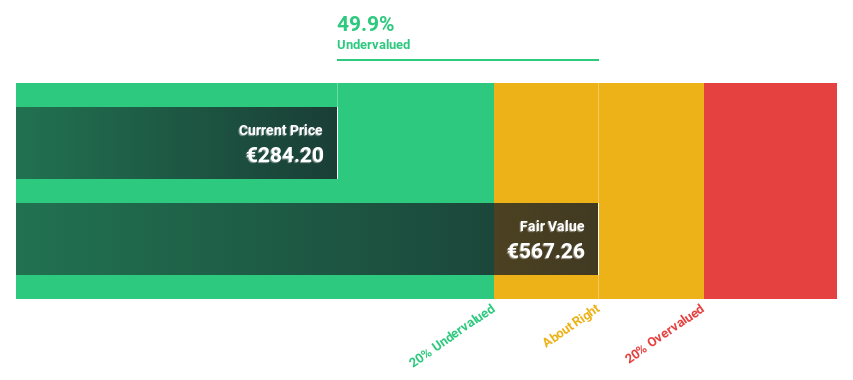

MTU Aero Engines (XTRA:MTX)

Overview: MTU Aero Engines AG operates in the development, manufacture, marketing, and support of commercial and military aircraft engines as well as industrial gas turbines globally, with a market capitalization of approximately €12.27 billion.

Operations: MTU Aero Engines generates revenue through two primary segments: the Commercial Maintenance Business (MRO), which brought in €4.35 billion, and the Commercial and Military Engine Business (OEM), which accounted for €1.27 billion.

Estimated Discount To Fair Value: 42.6%

MTU Aero Engines, trading at €227.9, is significantly undervalued based on a DCF valuation of €397.14, indicating a potential investment opportunity. The company's revenue growth at 12.2% per year outpaces the German market's 5.1%, with earnings expected to grow by 35.5% annually. Despite a slight dip in Q1 2024 profits with net income at €126 million down from €134 million year-over-year, MTU is forecasted to achieve high return on equity of 20.3% in three years, supporting its growth trajectory above the market average.

- Our comprehensive growth report raises the possibility that MTU Aero Engines is poised for substantial financial growth.

- Click to explore a detailed breakdown of our findings in MTU Aero Engines' balance sheet health report.

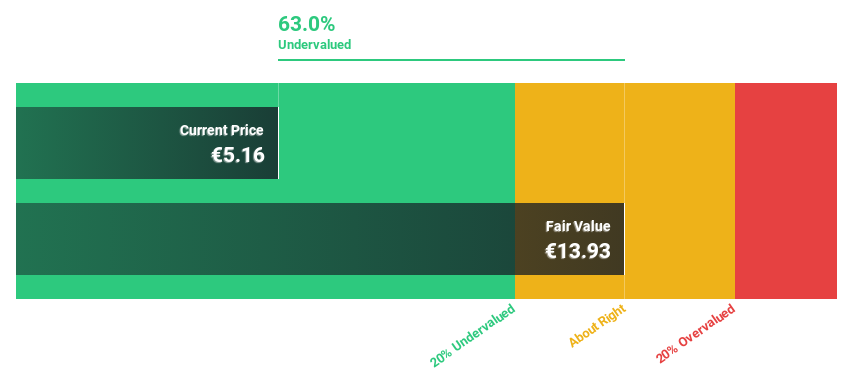

Novem Group (XTRA:NVM)

Overview: Novem Group S.A., based in Luxembourg, specializes in developing and supplying trim elements and decorative function elements for car interiors globally, with a market capitalization of €243.55 million.

Operations: The company generates €635.50 million from its auto parts and accessories segment.

Estimated Discount To Fair Value: 47.9%

Novem Group S.A., priced at €5.66, is considered highly undervalued with an estimated fair value of €10.86, reflecting a 47.9% potential undervaluation. Despite recent earnings declines—full-year net income dropped to €34.8 million from €50 million—the company is expected to see substantial earnings growth at 28.1% annually over the next three years, outpacing the German market forecast of 18.5%. However, it carries a high level of debt and has an unstable dividend track record, posing risks to its financial stability.

- Our expertly prepared growth report on Novem Group implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of Novem Group.

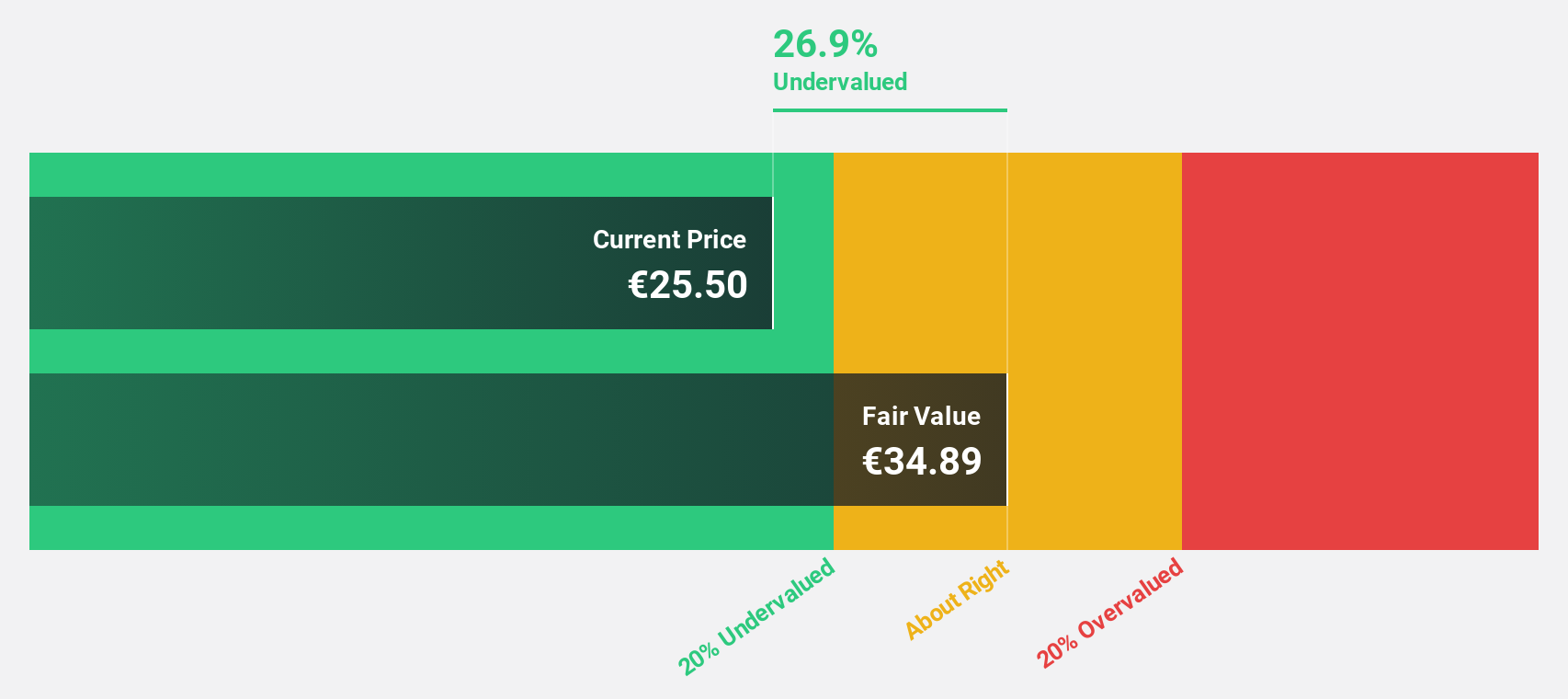

Kontron (XTRA:SANT)

Overview: Kontron AG is a company based in Austria that specializes in providing Internet of Things (IoT) solutions globally, with a market capitalization of approximately €1.25 billion.

Operations: The company generates revenue primarily from three segments: Europe (€971.03 million), Global (€269.17 million), and Software + Solutions (€306.81 million).

Estimated Discount To Fair Value: 35.8%

Kontron AG, with a current trading price of €20.3, appears undervalued based on DCF analysis, suggesting a fair value of €31.64. Recent product launches like the VX6096 and XMC-ETH6 highlight its commitment to enhancing high-performance computing capabilities, potentially boosting future cash flows. However, despite significant expected earnings growth over the next three years and trading 35.8% below estimated fair value, concerns remain due to an unstable dividend track record and only moderate revenue growth forecasts compared to the market.

- Our earnings growth report unveils the potential for significant increases in Kontron's future results.

- Unlock comprehensive insights into our analysis of Kontron stock in this financial health report.

Seize The Opportunity

- Gain an insight into the universe of 30 Undervalued German Stocks Based On Cash Flows by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kontron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:SANT

Kontron

Engages in the provision of internet of things (IoT) solutions in Austria and internationally.

Very undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives