Advertisement

- Germany

- /

- Aerospace & Defense

- /

- XTRA:HAG

Hensoldt's Raised Outlook and Growth Strategy Might Change The Case For Investing In Hensoldt (XTRA:HAG)

Simply Wall St

Reviewed by Sasha Jovanovic

- Hensoldt recently outlined a new growth strategy after reporting strong order intake and raising its mid-term EBITDA forecast, with further details discussed at the Annual General Meeting held on May 27, 2025.

- The company's operational momentum and revised outlook have drawn increased market interest, especially given its emphasis on expansion within defense and digitalization sectors.

- We'll examine how Hensoldt's elevated order intake and growth strategy influence its near-term outlook and broader investment narrative.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Hensoldt Investment Narrative Recap

To be a shareholder in Hensoldt, one must be confident in the sustained expansion of European defense spending and the company's ability to turn strong order momentum into profitable revenue growth. While the recent guidance upgrade and growth strategy outline affirm operational momentum, the catalyst of continued robust order intake will likely have more immediate impact on sentiment than longer-term risks such as execution on capacity expansion or changing political priorities. The risks tied to defense budget volatility remain material, but the outlook for near-term revenue growth stands out for now.

Among recent announcements, the confirmation of higher revenue guidance for 2025, targeting EUR 2,500 million to EUR 2,600 million, is most relevant to the current positive momentum. This guidance increase directly follows strong order inflows and underpins the upgraded earnings outlook, reinforcing the view that Hensoldt's near-term results are being shaped by the current defense spending cycle more than any singular operational challenge.

In contrast, investors should be aware that if European defense budgets shift or stall, the revenue growth that underpins consensus expectations could...

Read the full narrative on Hensoldt (it's free!)

Hensoldt's narrative projects €3.8 billion revenue and €353.8 million earnings by 2028. This requires 17.7% yearly revenue growth and a €263.8 million earnings increase from €90.0 million today.

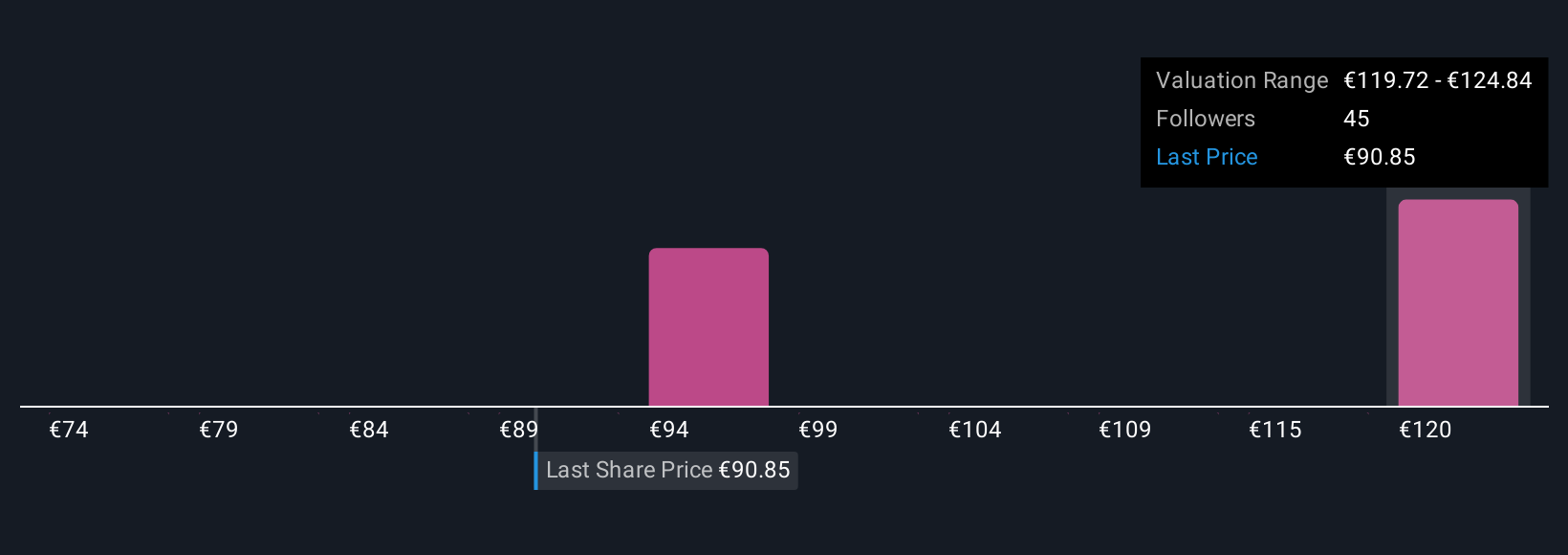

Uncover how Hensoldt's forecasts yield a €96.77 fair value, a 15% downside to its current price.

Exploring Other Perspectives

Fair value estimates from 11 members of the Simply Wall St Community range widely, from €73.60 to €127.68 per share. While growth optimism prevails, many recognize that delays or changes in defense budgets could have far-reaching effects on Hensoldt’s performance, so explore multiple viewpoints before making any decisions.

Explore 11 other fair value estimates on Hensoldt - why the stock might be worth as much as 12% more than the current price!

Build Your Own Hensoldt Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Hensoldt research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Hensoldt research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hensoldt's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hensoldt might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:HAG

Hensoldt

Provides sensor solutions for defense and security applications worldwide.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets