Advertisement

- Germany

- /

- Aerospace & Defense

- /

- XTRA:HAG

Hensoldt (XTRA:HAG): Valuation Insights Following Index Addition and Undervalued Stock Spotlight

Simply Wall St

Reviewed by Kshitija Bhandaru

Hensoldt (XTRA:HAG) has just been added to the FTSE All-World Index, catching the attention of investors looking for undervalued stocks across the European market. This index inclusion places Hensoldt on more global watchlists.

See our latest analysis for Hensoldt.

Hensoldt’s addition to the FTSE All-World Index has come as its positive outlook attracts investor attention. Over the past year, total shareholder return has crept up by about 2.8%, which hints at improving sentiment and renewed momentum as the broader European market steadies.

Curious to see how other players in aerospace and defense are performing? The best next step is to explore See the full list for free.

With Hensoldt attracting headlines for trading below its estimated fair value and fresh growth forecasts coming in, investors may be considering whether there is a genuine buying opportunity developing or if the market has already priced in future gains.

Most Popular Narrative: 16.8% Overvalued

With Hensoldt’s latest close price sitting well above the most widely followed narrative’s fair value calculation, there is a clear valuation premium in play. This sets the stage for lively debate over how bullish assumptions stack up against near-term risks and execution challenges.

The company reports robust order intake growth driven by increased defense spending, particularly in air defense, across Europe. However, future revenue expectations are based on elevated budget levels, which may not fully materialize, leading to potential overvaluation risk tied to revenue projections.

Want to see what makes this valuation tick? This narrative leans on ambitious growth rates, profit margin expansion and a bold assumption about future market multiples. The real financial backbone behind that price may surprise you. Take a closer look before the market does.

Result: Fair Value of €96.77 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Hensoldt’s robust order intake and strong operational efficiency could defy expectations and support further profitability, even if growth projections seem optimistic.

Find out about the key risks to this Hensoldt narrative.

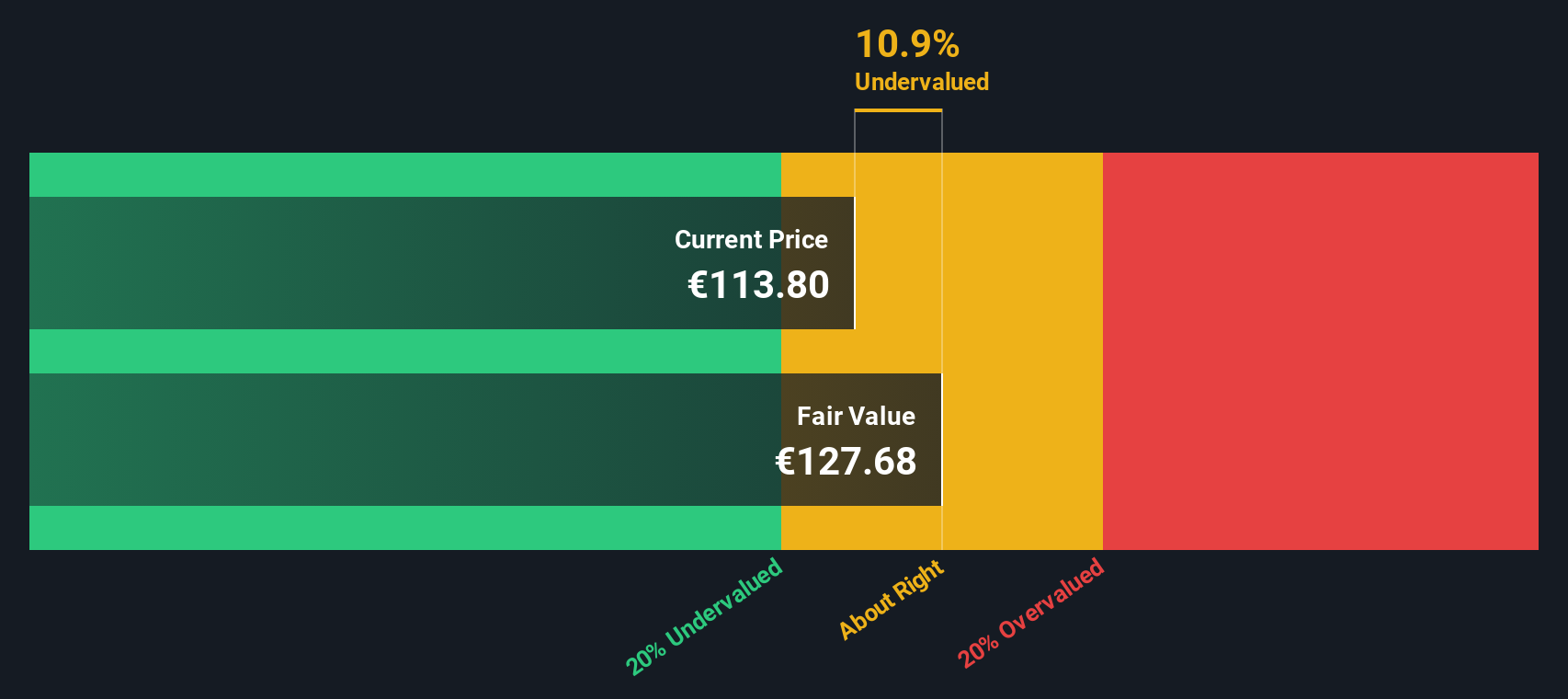

Another View: Discounted Cash Flow Valuation

Taking a different approach, our DCF model suggests that Hensoldt is trading about 11.7% below its fair value estimate of €127.93. Unlike market multiples, this model is based on forecasted future cash flows. As a result, it emphasizes longer-term fundamentals rather than prevailing sentiment. Can a cash-flow-driven perspective influence the ongoing discussion about Hensoldt’s true worth?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hensoldt for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hensoldt Narrative

If your perspective differs or you prefer to dig into the numbers personally, you can piece together your own narrative in under three minutes using Do it your way.

A great starting point for your Hensoldt research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Unlock your next investing win by targeting stocks that match your goals before others catch on. Let the Simply Wall Street Screener put you ahead of the curve.

- Catch profit potential early and size up these 3568 penny stocks with strong financials, chosen for strong financials and solid growth prospects.

- Fuel your portfolio with tech-powered winners by evaluating these 24 AI penny stocks, at the forefront of artificial intelligence and innovation.

- Strengthen your long-term returns and check out these 19 dividend stocks with yields > 3%, delivering reliable yields above 3% from companies with strong dividend track records.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hensoldt might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:HAG

Hensoldt

Provides sensor solutions for defense and security applications worldwide.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor