- Germany

- /

- Auto Components

- /

- XTRA:SFQ

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For SAF-Holland SE's (ETR:SFQ) CEO For Now

Key Insights

- SAF-Holland's Annual General Meeting to take place on 20th of May

- Total pay for CEO Alexander Geis includes €868.0k salary

- Total compensation is 1,355% above industry average

- SAF-Holland's total shareholder return over the past three years was 156% while its EPS grew by 18% over the past three years

Under the guidance of CEO Alexander Geis, SAF-Holland SE (ETR:SFQ) has performed reasonably well recently. As shareholders go into the upcoming AGM on 20th of May, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for SAF-Holland

Comparing SAF-Holland SE's CEO Compensation With The Industry

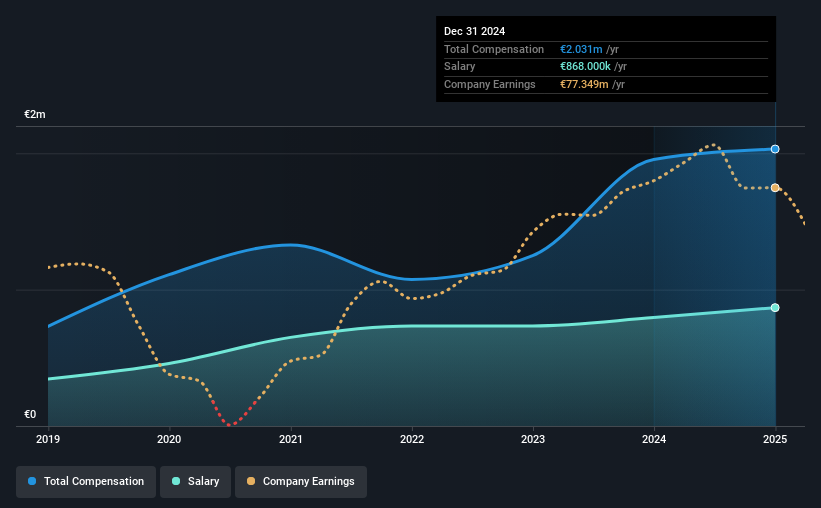

Our data indicates that SAF-Holland SE has a market capitalization of €787m, and total annual CEO compensation was reported as €2.0m for the year to December 2024. That's a modest increase of 3.9% on the prior year. We think total compensation is more important but our data shows that the CEO salary is lower, at €868k.

For comparison, other companies in the German Auto Components industry with market capitalizations ranging between €357m and €1.4b had a median total CEO compensation of €140k. Hence, we can conclude that Alexander Geis is remunerated higher than the industry median.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | €868k | €795k | 43% |

| Other | €1.2m | €1.2m | 57% |

| Total Compensation | €2.0m | €2.0m | 100% |

On an industry level, roughly 36% of total compensation represents salary and 64% is other remuneration. SAF-Holland pays out 43% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

SAF-Holland SE's Growth

Over the past three years, SAF-Holland SE has seen its earnings per share (EPS) grow by 18% per year. Its revenue is down 15% over the previous year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. While it would be good to see revenue growth, profits matter more in the end. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has SAF-Holland SE Been A Good Investment?

Boasting a total shareholder return of 156% over three years, SAF-Holland SE has done well by shareholders. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 2 warning signs for SAF-Holland that you should be aware of before investing.

Important note: SAF-Holland is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:SFQ

SAF-Holland

Manufactures and sells chassis-related assemblies and components for trailers, trucks, semi-trailers, and buses.

Established dividend payer and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion