Advertisement

- China

- /

- Infrastructure

- /

- SZSE:002023

Sichuan Haite High-tech Co.,Ltd.'s (SZSE:002023) 29% Price Boost Is Out Of Tune With Revenues

Sichuan Haite High-tech Co.,Ltd. (SZSE:002023) shares have continued their recent momentum with a 29% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 26% in the last year.

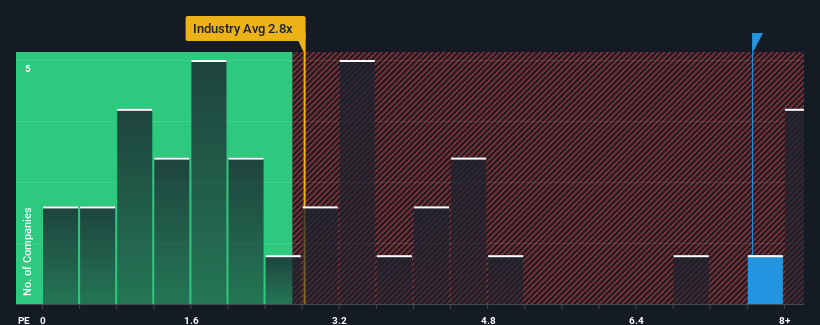

Following the firm bounce in price, when almost half of the companies in China's Infrastructure industry have price-to-sales ratios (or "P/S") below 2.8x, you may consider Sichuan Haite High-techLtd as a stock not worth researching with its 7.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Sichuan Haite High-techLtd

What Does Sichuan Haite High-techLtd's Recent Performance Look Like?

Recent revenue growth for Sichuan Haite High-techLtd has been in line with the industry. It might be that many expect the mediocre revenue performance to strengthen positively, which has kept the P/S ratio from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Sichuan Haite High-techLtd.Is There Enough Revenue Growth Forecasted For Sichuan Haite High-techLtd?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Sichuan Haite High-techLtd's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 19%. The latest three year period has also seen a 11% overall rise in revenue, aided extensively by its short-term performance. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 3.4% as estimated by the lone analyst watching the company. That's shaping up to be materially lower than the 16% growth forecast for the broader industry.

With this information, we find it concerning that Sichuan Haite High-techLtd is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Sichuan Haite High-techLtd's P/S has grown nicely over the last month thanks to a handy boost in the share price. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've concluded that Sichuan Haite High-techLtd currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Sichuan Haite High-techLtd that you should be aware of.

If these risks are making you reconsider your opinion on Sichuan Haite High-techLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002023

Sichuan Haite High-techLtd

Provides aircraft airborne equipment maintenance services in China.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor