Advertisement

- China

- /

- Wireless Telecom

- /

- SZSE:002148

After Leaping 26% Beijing Bewinner Communications Co., Ltd. (SZSE:002148) Shares Are Not Flying Under The Radar

Beijing Bewinner Communications Co., Ltd. (SZSE:002148) shareholders have had their patience rewarded with a 26% share price jump in the last month. The annual gain comes to 109% following the latest surge, making investors sit up and take notice.

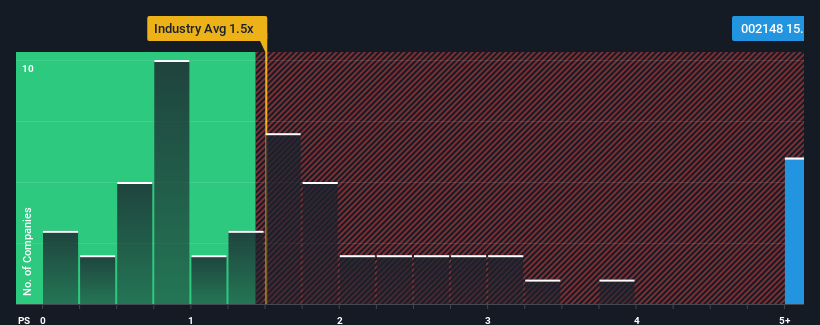

After such a large jump in price, you could be forgiven for thinking Beijing Bewinner Communications is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 15.1x, considering almost half the companies in China's Wireless Telecom industry have P/S ratios below 1.5x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Beijing Bewinner Communications

What Does Beijing Bewinner Communications' P/S Mean For Shareholders?

The revenue growth achieved at Beijing Bewinner Communications over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders may be a little nervous about the viability of the share price.

Although there are no analyst estimates available for Beijing Bewinner Communications, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Beijing Bewinner Communications?

The only time you'd be truly comfortable seeing a P/S as steep as Beijing Bewinner Communications' is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that the company managed to grow revenues by a handy 12% last year. This was backed up an excellent period prior to see revenue up by 33% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

This is in contrast to the rest of the industry, which is expected to grow by 6.9% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this information, we can see why Beijing Bewinner Communications is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What Does Beijing Bewinner Communications' P/S Mean For Investors?

The strong share price surge has lead to Beijing Bewinner Communications' P/S soaring as well. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It's no surprise that Beijing Bewinner Communications can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Beijing Bewinner Communications that you need to be mindful of.

If these risks are making you reconsider your opinion on Beijing Bewinner Communications, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Bewinner Communications might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002148

Beijing Bewinner Communications

Beijing Bewinner Communications Co., Ltd.

Flawless balance sheet very low.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor