Advertisement

- China

- /

- Tech Hardware

- /

- SZSE:301308

Shenzhen Longsys Electronics (SZSE:301308) Is Doing The Right Things To Multiply Its Share Price

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, Shenzhen Longsys Electronics (SZSE:301308) looks quite promising in regards to its trends of return on capital.

Return On Capital Employed (ROCE): What Is It?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Shenzhen Longsys Electronics is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

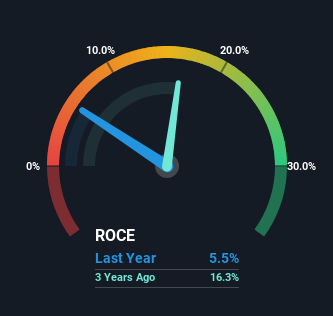

0.055 = CN¥544m ÷ (CN¥18b - CN¥7.8b) (Based on the trailing twelve months to June 2024).

Therefore, Shenzhen Longsys Electronics has an ROCE of 5.5%. Even though it's in line with the industry average of 5.6%, it's still a low return by itself.

View our latest analysis for Shenzhen Longsys Electronics

In the above chart we have measured Shenzhen Longsys Electronics' prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Shenzhen Longsys Electronics .

What Does the ROCE Trend For Shenzhen Longsys Electronics Tell Us?

Even though ROCE is still low in absolute terms, it's good to see it's heading in the right direction. The data shows that returns on capital have increased substantially over the last five years to 5.5%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 274%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Essentially the business now has suppliers or short-term creditors funding about 44% of its operations, which isn't ideal. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

The Bottom Line On Shenzhen Longsys Electronics' ROCE

To sum it up, Shenzhen Longsys Electronics has proven it can reinvest in the business and generate higher returns on that capital employed, which is terrific. And given the stock has remained rather flat over the last year, there might be an opportunity here if other metrics are strong. So researching this company further and determining whether or not these trends will continue seems justified.

On a final note, we found 3 warning signs for Shenzhen Longsys Electronics (2 are concerning) you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301308

Shenzhen Longsys Electronics

Engages in the research, development, design, packaging, testing, manufacturing, and sales of semiconductor storage application products.

Reasonable growth potential with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor