Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SZSE:300811

Discover 3 High Growth Chinese Stocks With Strong Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

As Chinese stocks face mixed signals from economic indicators and deflationary concerns, investors are seeking opportunities in companies that demonstrate resilience and potential for growth. One key factor to consider is high insider ownership, which often aligns management's interests with those of shareholders, fostering confidence in the company's long-term prospects.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 26.9% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Eoptolink Technology (SZSE:300502) | 26.7% | 39.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| Fujian Wanchen Biotechnology Group (SZSE:300972) | 14.9% | 82.1% |

| UTour Group (SZSE:002707) | 23% | 36.1% |

Let's review some notable picks from our screened stocks.

Shanghai Aohua Photoelectricity Endoscope (SHSE:688212)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai AoHua Photoelectricity Endoscope Co., Ltd. is a medical device company that focuses on the R&D, manufacture, and sale of electronic endoscopic equipment and consumables in China and internationally, with a market cap of CN¥6.02 billion.

Operations: The company generates revenue primarily from diagnostic kits and equipment, amounting to CN¥721.89 million.

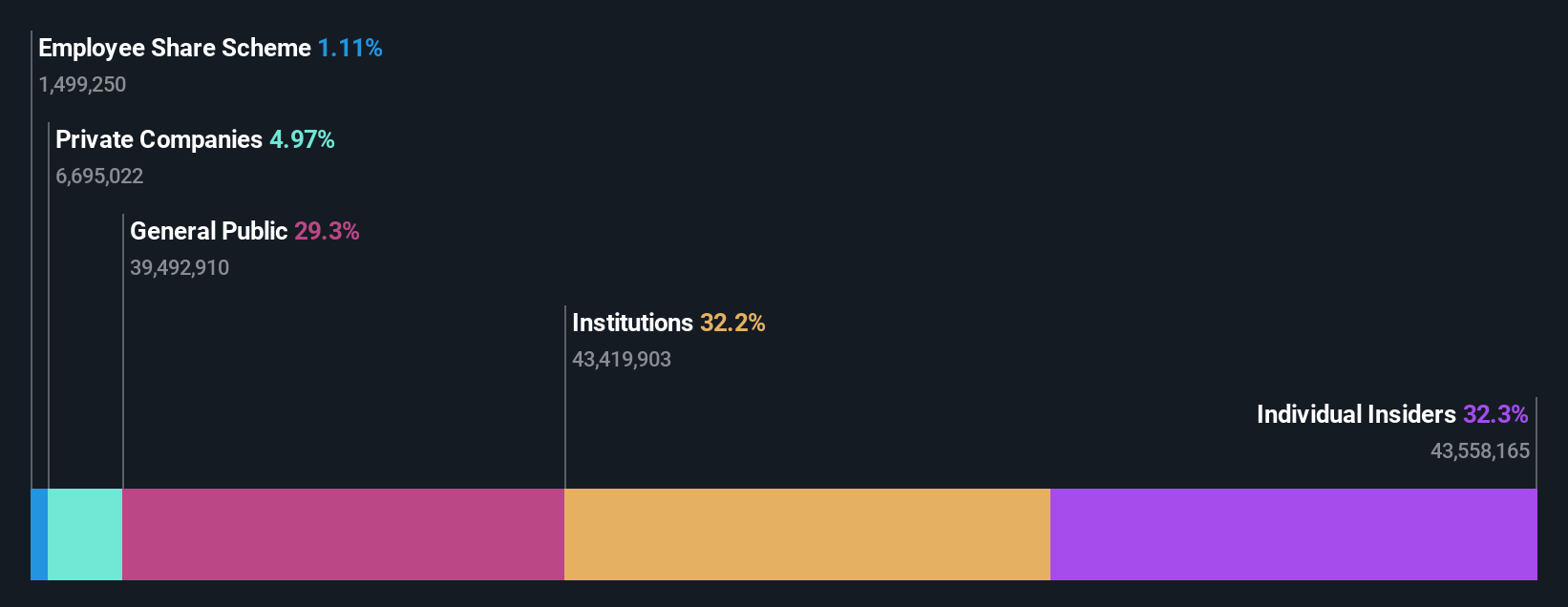

Insider Ownership: 32.3%

Shanghai Aohua Photoelectricity Endoscope is poised for significant growth with forecasted annual revenue and earnings increases of 27.5% and 58.1%, respectively, outpacing the broader Chinese market. Despite a volatile share price recently, analysts expect a substantial stock price rise of 58.8%. However, its Return on Equity is projected to be low at 11.7% in three years. No recent insider trading activity was noted ahead of the upcoming shareholders meeting on July 16, 2024.

- Get an in-depth perspective on Shanghai Aohua Photoelectricity Endoscope's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Shanghai Aohua Photoelectricity Endoscope shares in the market.

Shenzhen Envicool Technology (SZSE:002837)

Simply Wall St Growth Rating: ★★★★★★

Overview: Shenzhen Envicool Technology Co., Ltd. produces and sells temperature control solutions and products in China, with a market cap of CN¥16.06 billion.

Operations: The company's revenue segments include temperature control solutions and products in China.

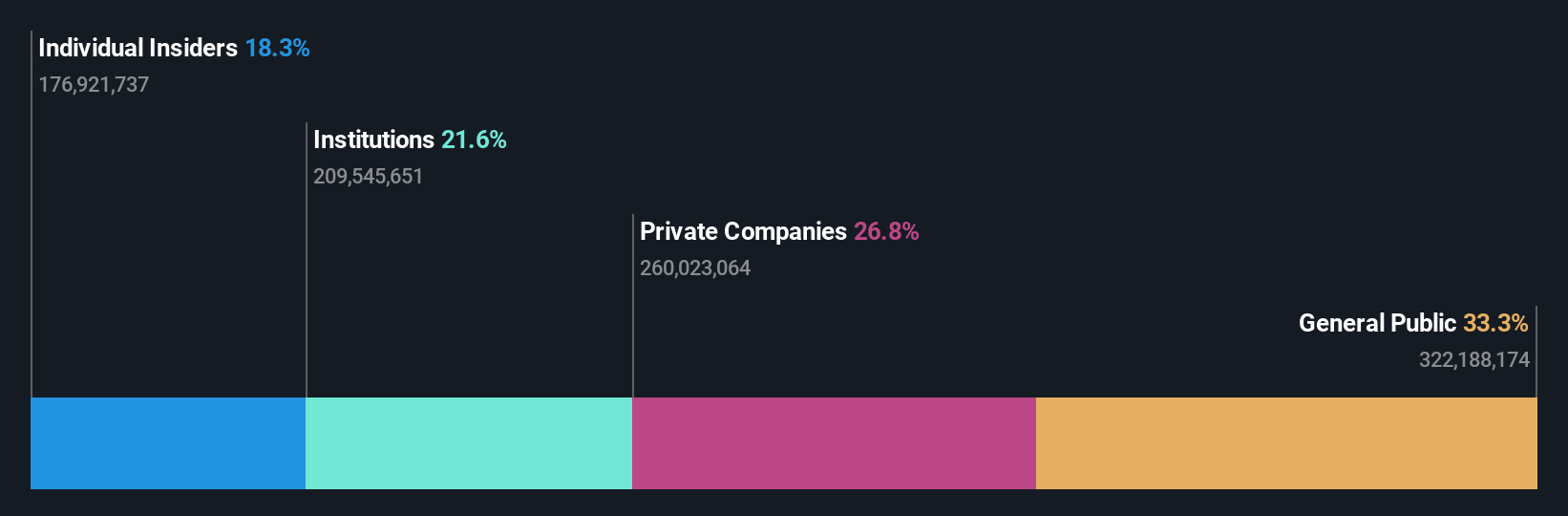

Insider Ownership: 19.7%

Shenzhen Envicool Technology has demonstrated strong growth, with half-year sales rising to CNY 1.71 billion from CNY 1.24 billion a year ago and net income doubling to CNY 183.47 million. Earnings per share also improved significantly. Analysts forecast revenue growth of 21.8% annually, outpacing the broader Chinese market, with earnings expected to grow at 24.23% per year over the next three years, driven by high insider ownership and robust financial performance.

- Click here to discover the nuances of Shenzhen Envicool Technology with our detailed analytical future growth report.

- Our expertly prepared valuation report Shenzhen Envicool Technology implies its share price may be lower than expected.

POCO Holding (SZSE:300811)

Simply Wall St Growth Rating: ★★★★★☆

Overview: POCO Holding Co., Ltd. develops, produces, and sells alloy soft magnetic powder, alloy soft magnetic cores, and related inductance components for users of electronic equipment, with a market cap of CN¥10.56 billion.

Operations: The company generates revenue primarily from electronic components, amounting to CN¥1.20 billion.

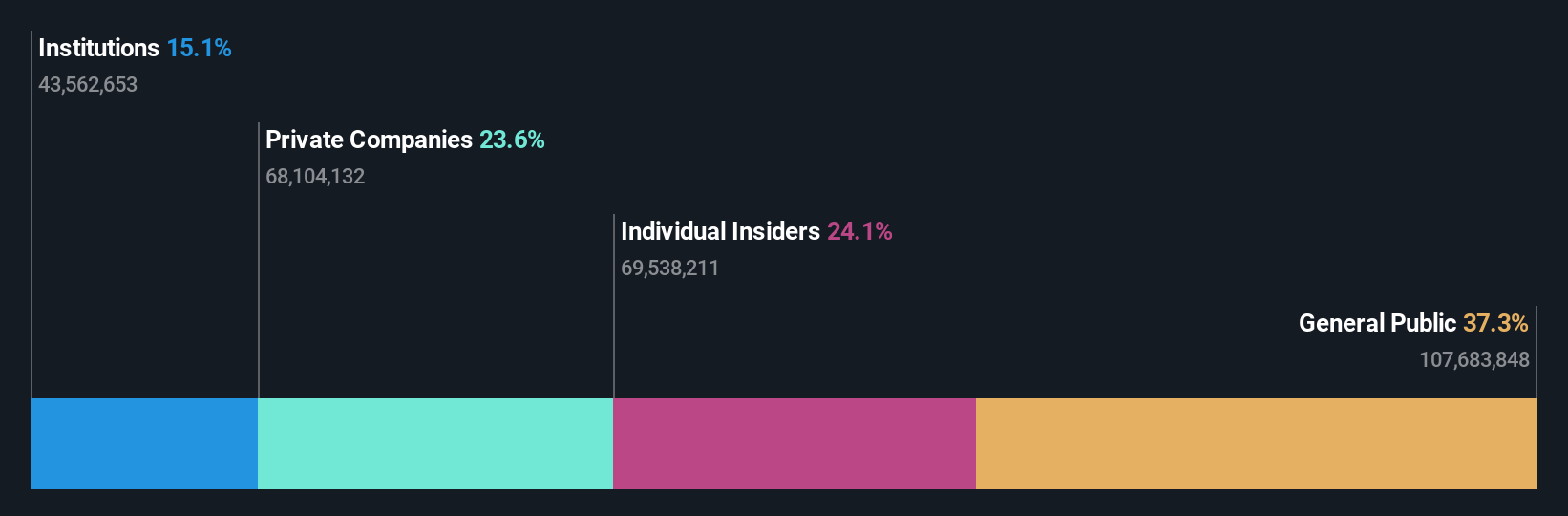

Insider Ownership: 24.8%

POCO Holding's earnings are projected to grow at 28.01% annually, surpassing the Chinese market average of 22%. Revenue is expected to increase by 26.6% per year, also outpacing the market's 13.5%. Despite a volatile share price recently, it trades at a notable discount to its estimated fair value. Recent amendments to company bylaws and dividend affirmations underscore management's commitment to shareholder value but no substantial insider trading activity has been reported in the past three months.

- Click here and access our complete growth analysis report to understand the dynamics of POCO Holding.

- According our valuation report, there's an indication that POCO Holding's share price might be on the cheaper side.

Next Steps

- Click through to start exploring the rest of the 363 Fast Growing Chinese Companies With High Insider Ownership now.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300811

POCO Holding

Develops, produces, and sells alloy soft magnetic powder, and alloy soft magnetic core and related inductance components for the downstream users of electricity electronic equipment.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor