- China

- /

- Communications

- /

- SZSE:300548

Quectel Wireless Solutions And Two Other Leading Growth Stocks With Strong Insider Ownership

Reviewed by Simply Wall St

As global markets navigate a period of volatility, characterized by inflation concerns and fluctuating interest rates, investors are closely watching economic indicators and policy shifts. In this environment, growth companies with strong insider ownership can offer unique insights into potential resilience and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 23.8% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 35.8% |

| Medley (TSE:4480) | 34% | 27.2% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's dive into some prime choices out of the screener.

Quectel Wireless Solutions (SHSE:603236)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Quectel Wireless Solutions Co., Ltd. focuses on the research, design, production, and sales of wireless communication modules and solutions globally, with a market cap of approximately CN¥18.19 billion.

Operations: The company generates revenue from the research, development, design, production, and sales of wireless communication modules and solutions on a global scale.

Insider Ownership: 23.3%

Revenue Growth Forecast: 19% p.a.

Quectel Wireless Solutions, with significant insider ownership, is positioned for growth as its earnings are forecast to grow substantially faster than the Chinese market. Despite a lower projected return on equity of 17%, Quectel trades well below estimated fair value. Recent product innovations, including GNSS modules and antennas, highlight its commitment to IoT solutions. Strategic alliances like the one with Swift Navigation enhance its high-precision positioning capabilities across diverse industries.

- Dive into the specifics of Quectel Wireless Solutions here with our thorough growth forecast report.

- According our valuation report, there's an indication that Quectel Wireless Solutions' share price might be on the cheaper side.

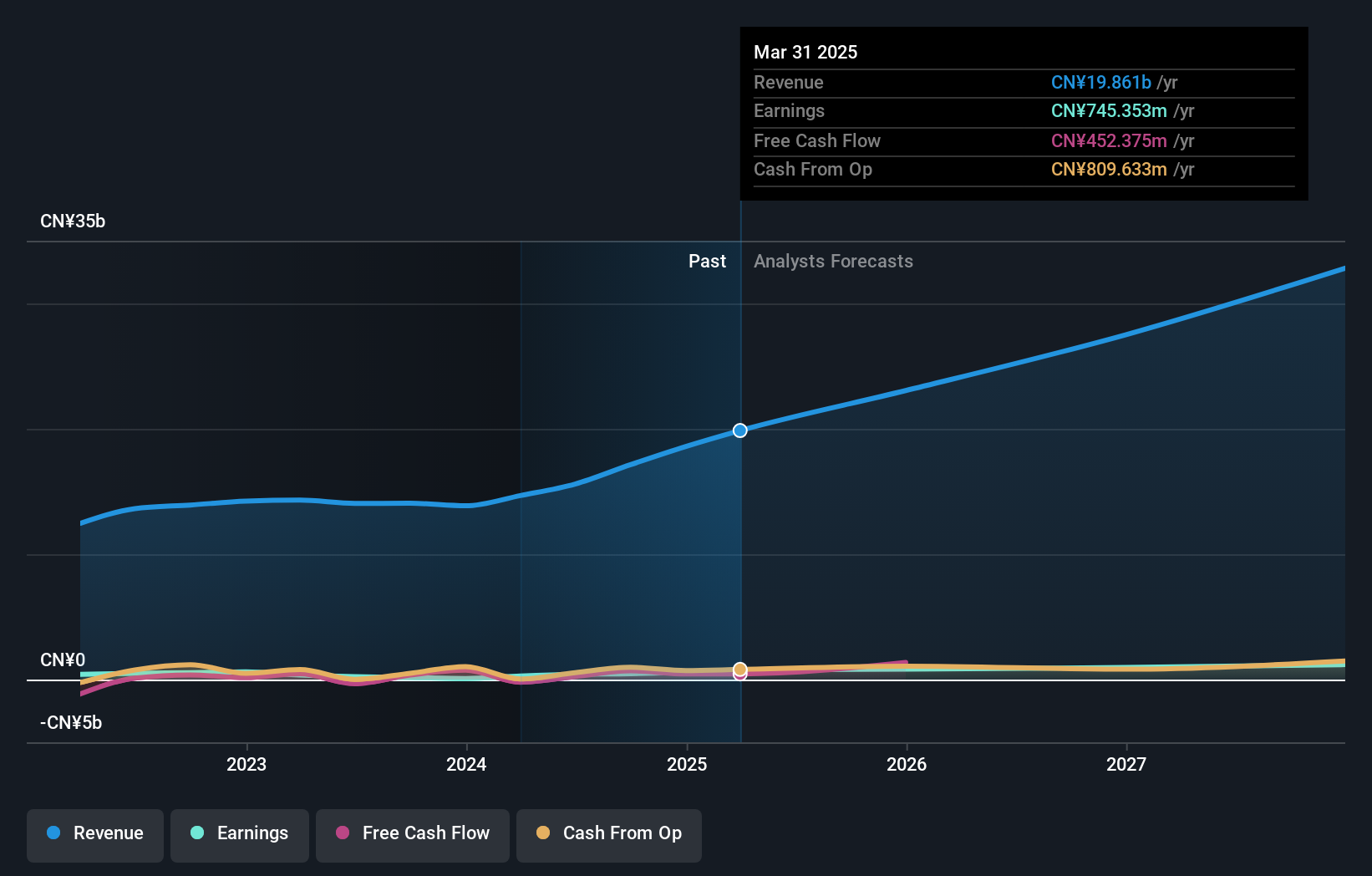

Broadex Technologies (SZSE:300548)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Broadex Technologies Co., Ltd. engages in the research, development, production, and sale of integrated optoelectronic devices for optical communications both in China and internationally, with a market cap of approximately CN¥12.65 billion.

Operations: Broadex Technologies generates revenue through the research, development, production, and sale of integrated optoelectronic devices for optical communications across domestic and international markets.

Insider Ownership: 11.5%

Revenue Growth Forecast: 24.3% p.a.

Broadex Technologies is anticipated to see revenue growth of 24.3% annually, outpacing the broader Chinese market. Despite recent earnings declines, with net income at CNY 37.5 million for the first nine months of 2024 compared to CNY 140.81 million a year prior, future profitability is expected within three years. Recent shareholder meetings focused on acquisitions and fund allocation changes, while insider ownership remains significant without recent substantial trading activity.

- Navigate through the intricacies of Broadex Technologies with our comprehensive analyst estimates report here.

- The analysis detailed in our Broadex Technologies valuation report hints at an inflated share price compared to its estimated value.

Flaircomm Microelectronics (SZSE:301600)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Flaircomm Microelectronics, Inc. develops and sells wireless communication modules, embedded software, and turnkey system solutions for automotive and M2M applications in China with a market cap of CN¥16.49 billion.

Operations: The company's revenue is primarily derived from its Wireless Communications Equipment segment, which generated CN¥995.17 million.

Insider Ownership: 35.5%

Revenue Growth Forecast: 26.7% p.a.

Flaircomm Microelectronics is experiencing robust growth, with earnings up 44.7% year-over-year and sales reaching CNY 734.85 million for the first nine months of 2024. Forecasts suggest annual profit growth of 30.8%, surpassing the Chinese market average. Despite high volatility in its share price, insider ownership remains stable without recent significant trading activity. However, future return on equity is expected to be modest at 17.2%, potentially impacting long-term investment appeal.

- Click here and access our complete growth analysis report to understand the dynamics of Flaircomm Microelectronics.

- Our comprehensive valuation report raises the possibility that Flaircomm Microelectronics is priced higher than what may be justified by its financials.

Make It Happen

- Navigate through the entire inventory of 1438 Fast Growing Companies With High Insider Ownership here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Broadex Technologies, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Broadex Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300548

Broadex Technologies

Researches and develops, produces, and sells integrated optoelectronic devices in the field of optical communications in China and internationally.

Solid track record with excellent balance sheet.

Market Insights

Community Narratives