Advertisement

- Hong Kong

- /

- Electrical

- /

- SEHK:1729

Undiscovered Gems With Potential For February 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by fluctuating corporate earnings, AI competition fears, and steady interest rates from the Federal Reserve, small-cap stocks have faced their share of volatility. Despite these challenges, the Dow Jones Industrial Average has shown resilience with its continued gains, while other indices like the S&P 500 and Nasdaq Composite reflect a more cautious sentiment among investors. In this environment, identifying promising stocks involves looking for those with strong fundamentals that can withstand economic uncertainties and leverage emerging opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Central Forest Group | NA | 6.85% | 15.11% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Chilanga Cement | NA | 13.46% | 35.92% | ★★★★★★ |

| La Forestière Equatoriale | NA | -58.49% | 45.78% | ★★★★★★ |

| First National Bank of Botswana | 24.77% | 10.64% | 15.30% | ★★★★★☆ |

| Societe de Limonaderies et de Boissons Rafraichissantes d'Afrique | 39.37% | 4.38% | -14.46% | ★★★★★☆ |

| Procimmo Group | 157.49% | 0.65% | 4.94% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

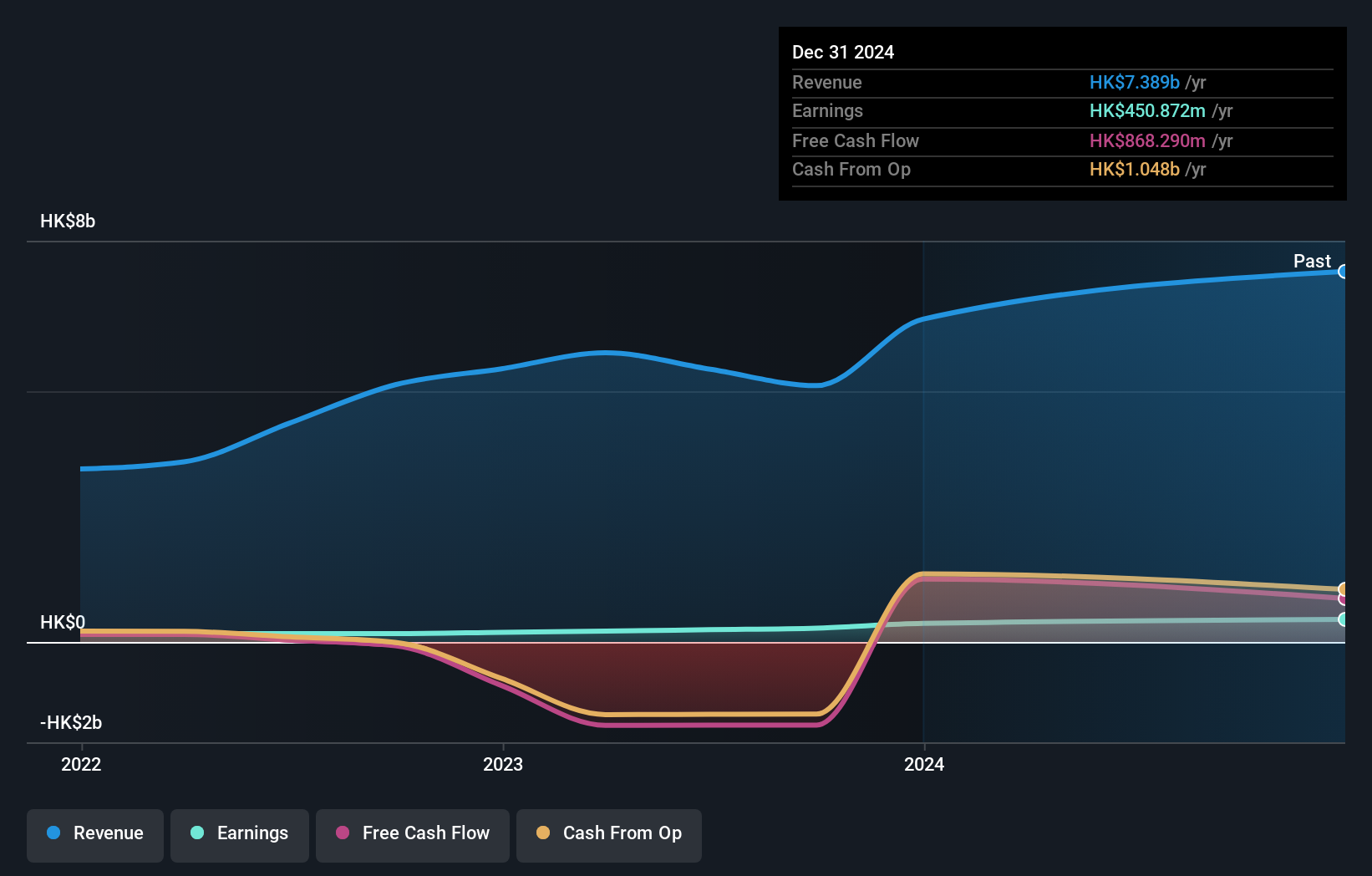

Time Interconnect Technology (SEHK:1729)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Time Interconnect Technology Limited is an investment holding company that manufactures and sells cable assembly and networking cable products across various international markets, with a market cap of HK$8.81 billion.

Operations: Time Interconnect derives its revenue primarily from three segments: Server (HK$2.98 billion), Digital Cable (HK$1.18 billion), and Cable Assembly (HK$2.31 billion).

Time Interconnect Technology, a relatively small player in the industry, has shown impressive earnings growth of 93.1% over the past year, outpacing the Electrical industry's 7.7%. Despite its high net debt to equity ratio of 184.9%, interest payments are well covered with EBIT covering debt interest nine times over. Recent developments include an increased annual cap under their agreement with Luxshare Precision from HK$130 million to HK$170 million for product supply until March 2025, reflecting growing demand in medical equipment cables. Trading at a significant discount to estimated fair value suggests potential upside if financial health improves.

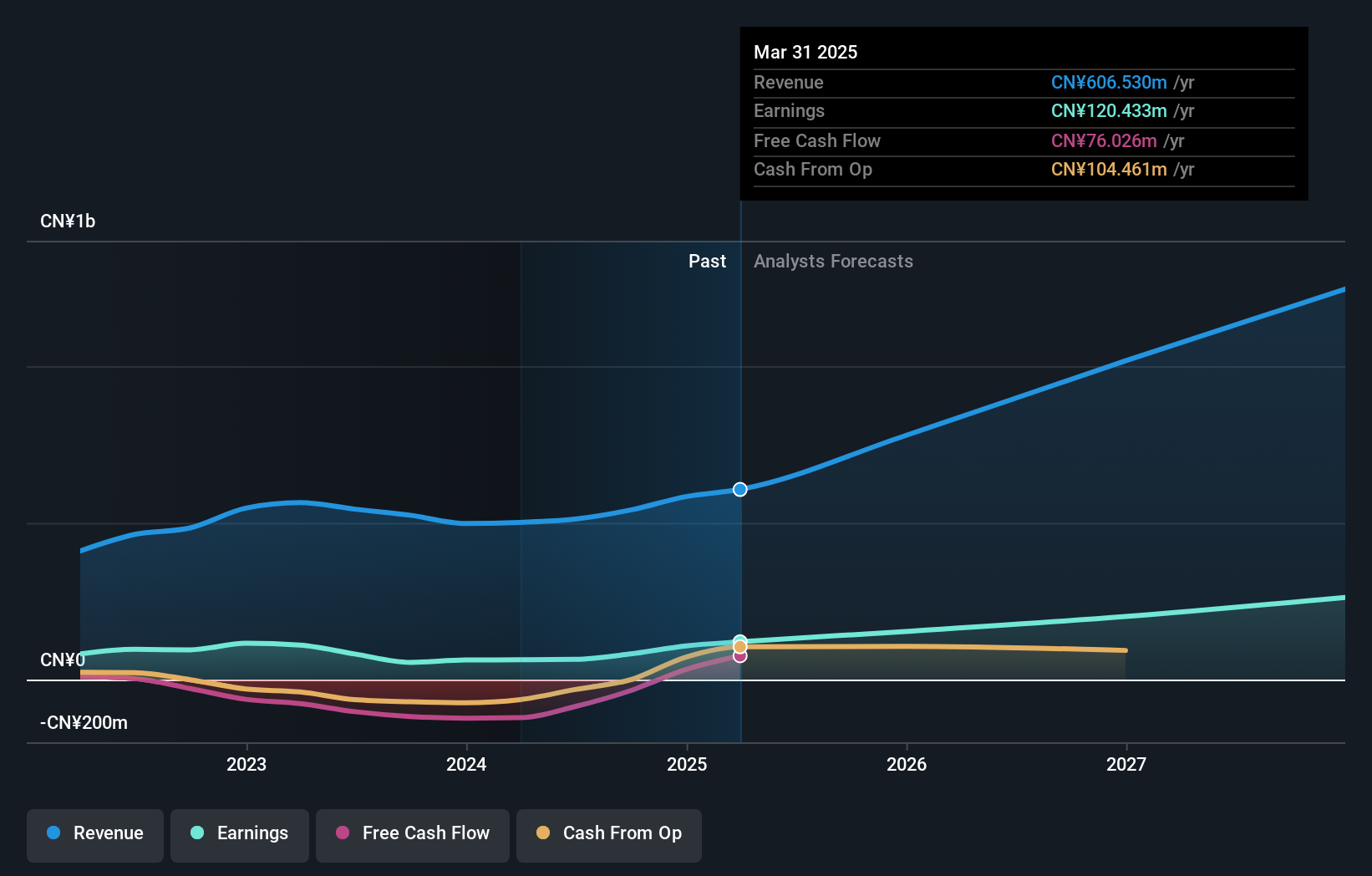

Anhui Ronds Science & Technology (SHSE:688768)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Anhui Ronds Science & Technology Incorporated Company offers machinery condition monitoring solutions for predictive maintenance in China, with a market cap of CN¥3.85 billion.

Operations: Ronds generates revenue primarily from its machinery condition monitoring solutions. The company's cost structure includes expenses related to product development and operational activities. Gross profit margin trends provide insights into the company's pricing strategy and cost management effectiveness, reflecting a key area of financial performance.

Anhui Ronds Science & Technology, a dynamic player in the electronics sector, has shown remarkable earnings growth of 48.7% over the past year, outpacing its industry peers who grew at just 2.3%. With a price-to-earnings ratio of 47x that sits below the industry average of 47.6x, it presents an attractive valuation for potential investors. Despite its debt to equity ratio increasing from 4% to 5% over five years, it maintains more cash than total debt and covers interest payments comfortably. A special shareholders meeting is slated for December in Hefei, potentially signaling strategic developments ahead.

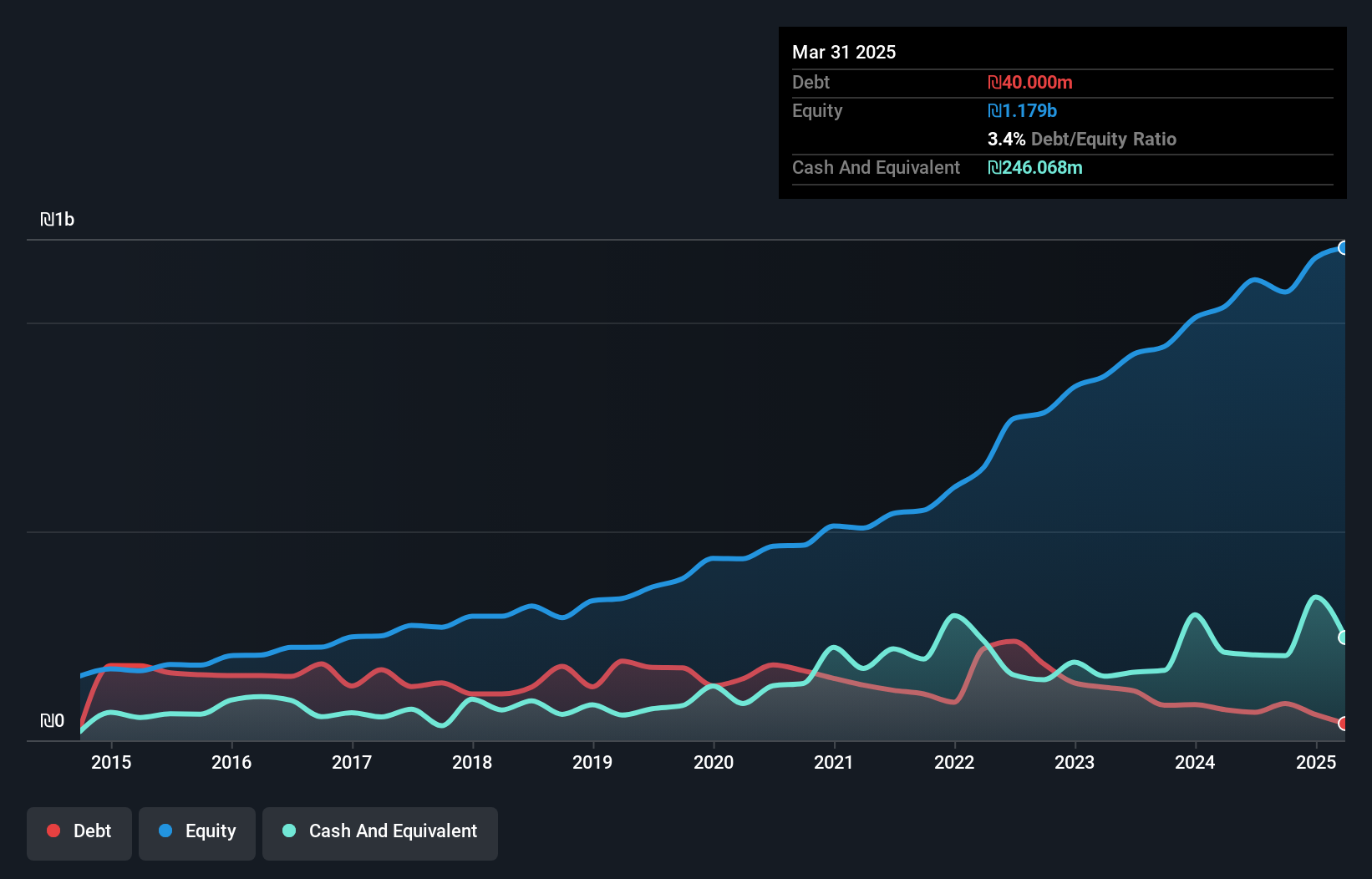

Hilan (TASE:HLAN)

Simply Wall St Value Rating: ★★★★★★

Overview: Hilan Ltd. is a software as a service (SaaS) provider that develops solutions for managing enterprise human capital in Israel, with a market capitalization of ₪6.52 billion.

Operations: Hilan generates revenue primarily from Business Information Services (₪1.62 billion) and Payroll Services, Human Resources and Organizational Systems (₪511.86 million). The company also earns from Computer Infrastructure and Marketing of Software Products, contributing to its total revenue streams.

Hilan, a promising player in the professional services sector, is trading at 26.9% below its estimated fair value, suggesting potential upside for investors. Over the past year, earnings have grown by 17.8%, outpacing the industry's 10.2% growth rate and highlighting its competitive edge. The company's debt situation has improved significantly with a reduction in the debt-to-equity ratio from 44.8% to 8.2% over five years, indicating sound financial management. Recent results show sales of ILS 694 million and net income of ILS 49 million for Q3, reflecting steady performance improvement compared to last year’s figures.

- Click to explore a detailed breakdown of our findings in Hilan's health report.

Review our historical performance report to gain insights into Hilan's's past performance.

Taking Advantage

- Click this link to deep-dive into the 4710 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Time Interconnect Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1729

Time Interconnect Technology

An investment holding company, manufactures and sells cable assembly, digital cable, and server products in the People's Republic of China, the United States, Singapore, the Netherlands, Hong Kong, Mexico, the United Kingdom, and internationally.

Exceptional growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative