Advertisement

- China

- /

- Capital Markets

- /

- SHSE:603093

Uncovering 3 Undiscovered Gems In Asia For Potential Growth

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate through economic shifts and rate cut expectations, the Asian market presents intriguing opportunities for investors seeking potential growth. In this dynamic landscape, identifying stocks with strong fundamentals and resilience amidst changing economic indicators can be key to uncovering hidden gems that may offer promising prospects.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Natural Food International Holding | NA | 8.04% | 37.71% | ★★★★★★ |

| 104 | NA | 10.13% | 11.50% | ★★★★★★ |

| Soft-World International | NA | -1.48% | 5.58% | ★★★★★★ |

| Bonny Worldwide | 43.84% | 17.85% | 41.97% | ★★★★★★ |

| China Post Technology | NA | -35.78% | 7.84% | ★★★★★★ |

| Minmetals Development | 62.90% | -1.49% | -17.98% | ★★★★★★ |

| Aerospace Hi-Tech Holding Group | NA | 5.18% | 42.12% | ★★★★★★ |

| Unitech Computer | 43.58% | 2.50% | 0.68% | ★★★★★☆ |

| Chinyang Holdings | 31.14% | 7.30% | -20.39% | ★★★★★☆ |

| ASL Marine Holdings | 155.37% | 13.24% | 51.91% | ★★★★☆☆ |

We'll examine a selection from our screener results.

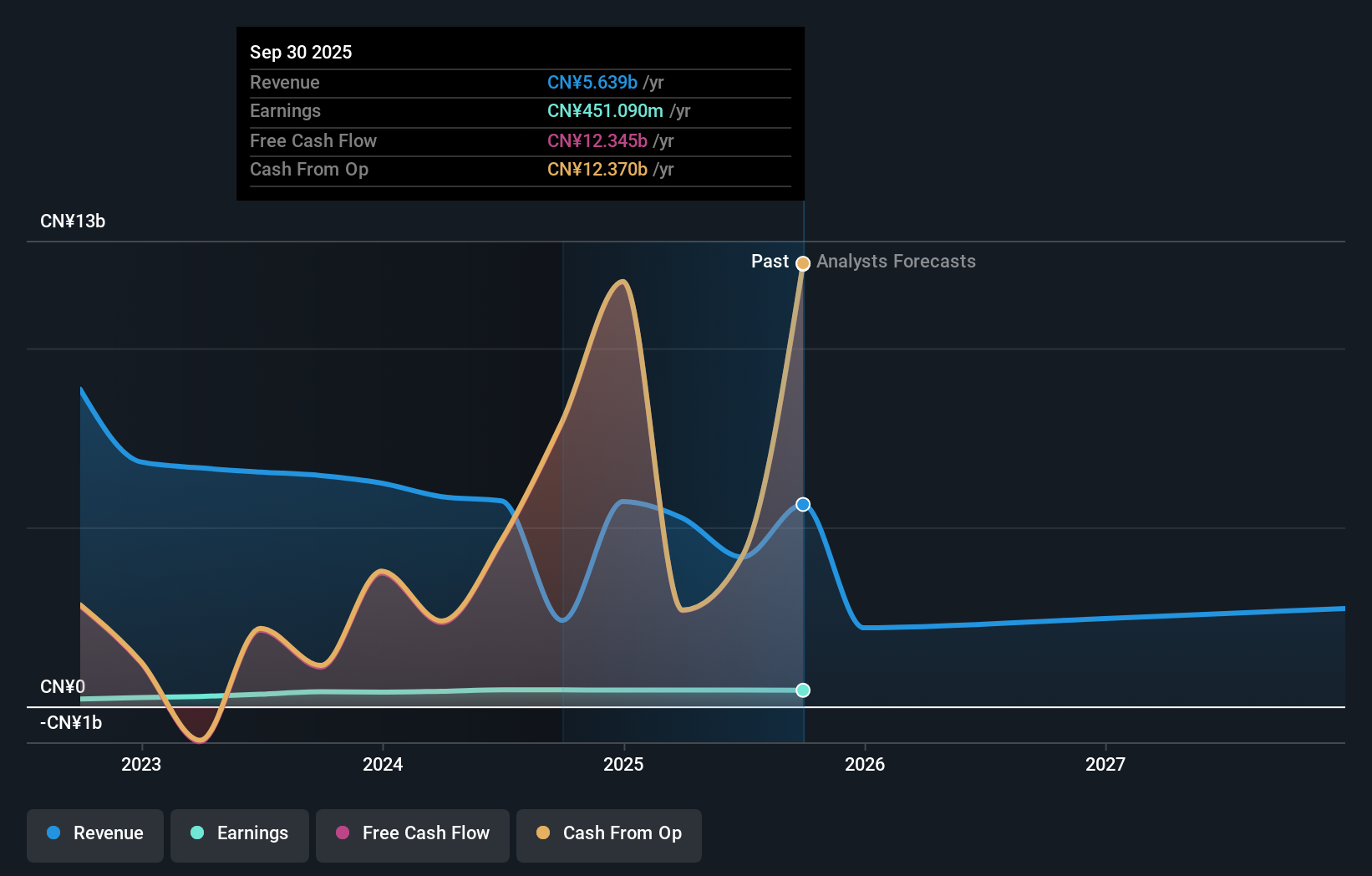

Nanhua Futures (SHSE:603093)

Simply Wall St Value Rating: ★★★★★☆

Overview: Nanhua Futures Co., Ltd. is a financial services company specializing in derivatives, with a market capitalization of CN¥13.88 billion.

Operations: Nanhua Futures Co., Ltd. generates revenue primarily from its derivatives business, with a market capitalization of CN¥13.88 billion. The company's financial performance is influenced by its ability to manage costs effectively, impacting its profitability metrics such as net profit margin.

Nanhua Futures, a smaller player in the financial sector, has demonstrated resilience despite facing challenges. The company's debt to equity ratio has impressively dropped from 60.5% to 26.2% over five years, indicating effective debt management. Its price-to-earnings ratio of 30.2x is attractive compared to the broader CN market's 46x, suggesting potential value for investors. However, earnings growth was negative at -1%, significantly lagging behind the industry average of 57%. Recent earnings calls revealed stable net income year-on-year at CNY 231 million despite revenue falling to CNY 1,100 million from CNY 2,638 million previously.

- Unlock comprehensive insights into our analysis of Nanhua Futures stock in this health report.

Gain insights into Nanhua Futures' past trends and performance with our Past report.

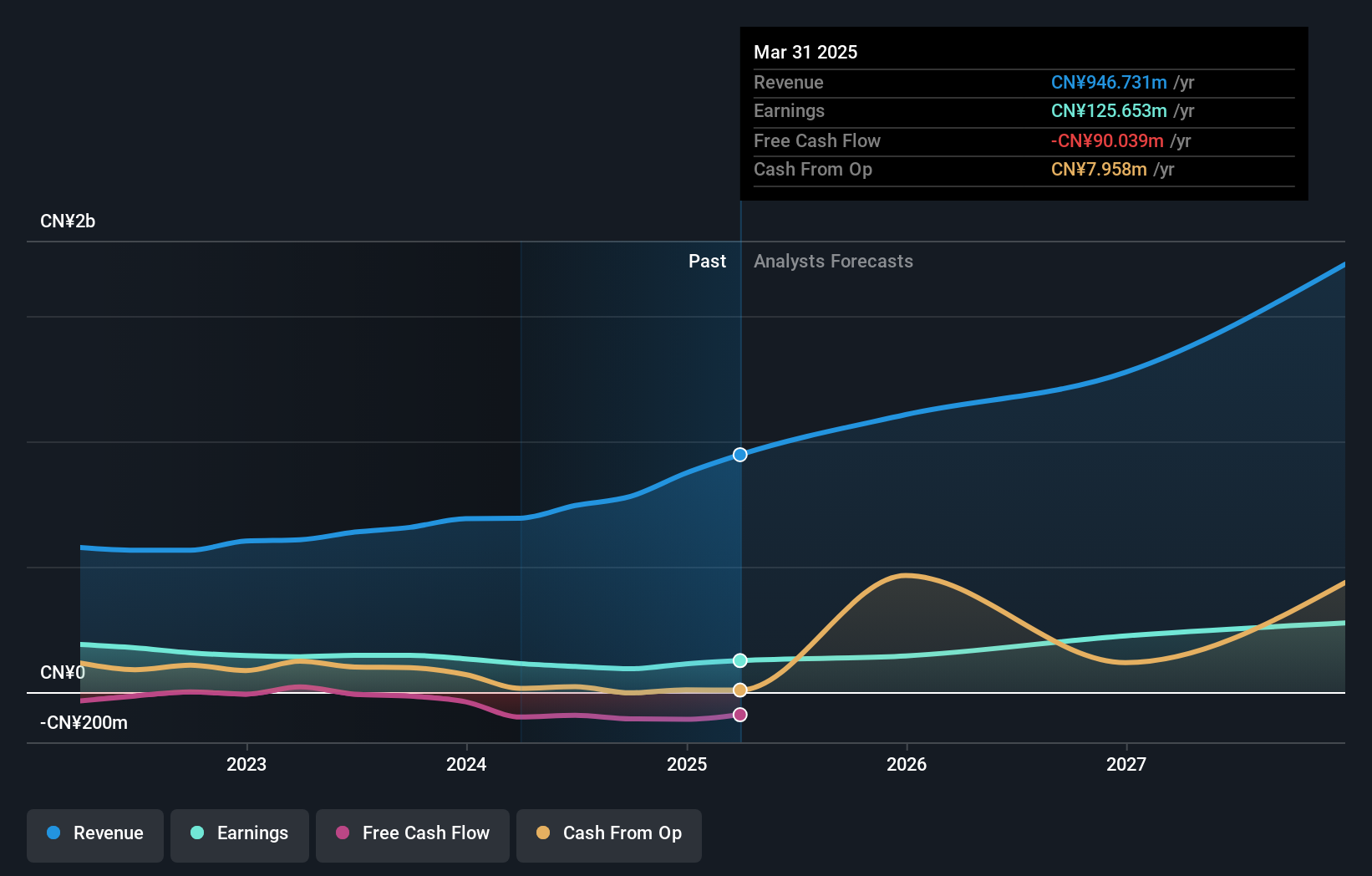

Cubic Sensor and InstrumentLtd (SHSE:688665)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Cubic Sensor and Instrument Co., Ltd. focuses on developing, producing, and selling gas sensors and sensor solutions in China with a market capitalization of CN¥6.77 billion.

Operations: Cubic Sensor and Instrument Ltd generates revenue primarily from the sale of gas sensors and sensor solutions in China. The company has a market capitalization of CN¥6.77 billion.

Cubic Sensor and Instrument Ltd. has shown notable growth, with earnings increasing by 52% over the past year, outpacing the electronic industry average of 3.8%. The company's net income for the first half of 2025 was CNY 84.12 million, a significant rise from CNY 41.36 million in the previous year, reflecting strong operational performance. Despite a volatile share price recently, Cubic's debt management appears satisfactory with a net debt to equity ratio at 4.4%, and interest payments are well-covered by EBIT at an impressive 94x coverage. Looking ahead, earnings are forecasted to grow annually by approximately 21%.

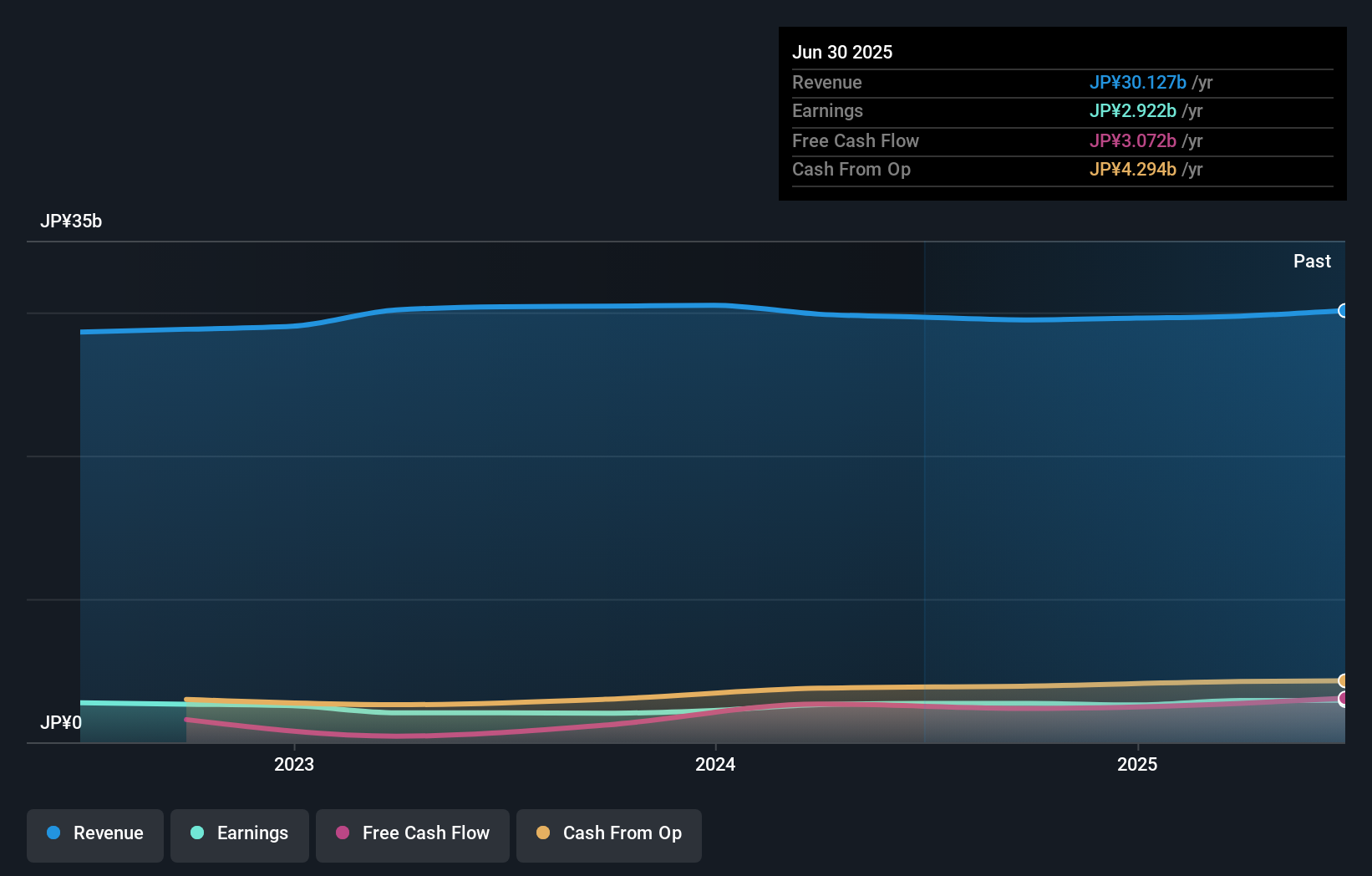

SOFT99corporation (TSE:4464)

Simply Wall St Value Rating: ★★★★★★

Overview: SOFT99corporation specializes in the manufacture and sale of chemical products for auto and home care both in Japan and internationally, with a market cap of ¥74.38 billion.

Operations: Revenue for SOFT99corporation is derived primarily from the sale of chemical products related to auto and home care, both domestically and internationally. The company has a market capitalization of ¥74.38 billion.

SOFT99, a nimble player in the auto components sector, has seen its earnings grow by 8% over the past year, outpacing an industry decline of 10.7%. The company's debt to equity ratio has improved from 0.2 to 0.1 over five years, indicating prudent financial management. With more cash than total debt and positive free cash flow, financial stability seems assured. However, recent share price volatility could be concerning for some investors. A significant development is Hideaki Tanaka's proposal to acquire a majority stake for ¥36.4 billion (¥2465 per share), which may lead to delisting if successful by September end.

- Click here to discover the nuances of SOFT99corporation with our detailed analytical health report.

Explore historical data to track SOFT99corporation's performance over time in our Past section.

Where To Now?

- Access the full spectrum of 2390 Asian Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nanhua Futures might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603093

Nanhua Futures

Provides financial services focused on derivatives business.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets