Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SHSE:603386

Guangdong Champion Asia ElectronicsLtd (SHSE:603386) May Have Issues Allocating Its Capital

To find a multi-bagger stock, what are the underlying trends we should look for in a business? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at Guangdong Champion Asia ElectronicsLtd (SHSE:603386), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Guangdong Champion Asia ElectronicsLtd is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.071 = CN¥136m ÷ (CN¥3.6b - CN¥1.7b) (Based on the trailing twelve months to September 2023).

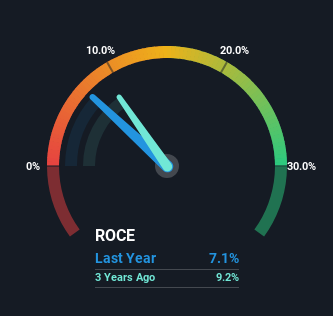

Thus, Guangdong Champion Asia ElectronicsLtd has an ROCE of 7.1%. On its own that's a low return, but compared to the average of 5.3% generated by the Electronic industry, it's much better.

Check out our latest analysis for Guangdong Champion Asia ElectronicsLtd

Historical performance is a great place to start when researching a stock so above you can see the gauge for Guangdong Champion Asia ElectronicsLtd's ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Guangdong Champion Asia ElectronicsLtd.

So How Is Guangdong Champion Asia ElectronicsLtd's ROCE Trending?

On the surface, the trend of ROCE at Guangdong Champion Asia ElectronicsLtd doesn't inspire confidence. Around five years ago the returns on capital were 13%, but since then they've fallen to 7.1%. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It may take some time before the company starts to see any change in earnings from these investments.

On a separate but related note, it's important to know that Guangdong Champion Asia ElectronicsLtd has a current liabilities to total assets ratio of 47%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In Conclusion...

In summary, Guangdong Champion Asia ElectronicsLtd is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. Additionally, the stock's total return to shareholders over the last five years has been flat, which isn't too surprising. All in all, the inherent trends aren't typical of multi-baggers, so if that's what you're after, we think you might have more luck elsewhere.

On a separate note, we've found 3 warning signs for Guangdong Champion Asia ElectronicsLtd you'll probably want to know about.

While Guangdong Champion Asia ElectronicsLtd may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603386

Guangdong Champion Asia ElectronicsLtd

Guangdong Champion Asia Electronics Co.,Ltd.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|43.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|51.3% undervalued

TO

Community Contributor