Advertisement

- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:2317

Exploring High Growth Tech Stocks for December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets experience fluctuations, with U.S. stocks facing declines due to cautious Federal Reserve commentary and political uncertainty, the focus on high growth tech stocks becomes particularly relevant for investors seeking potential opportunities amidst broader market volatility. In such an environment, identifying a promising stock often involves looking at companies with innovative technologies and strong growth prospects that can navigate economic challenges and capitalize on market trends.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Material Group | 20.45% | 24.01% | ★★★★★★ |

| Seojin SystemLtd | 35.41% | 39.86% | ★★★★★★ |

| Yggdrazil Group | 30.20% | 87.10% | ★★★★★★ |

| eWeLLLtd | 27.24% | 28.74% | ★★★★★★ |

| Ascelia Pharma | 76.15% | 47.16% | ★★★★★★ |

| Medley | 25.57% | 31.67% | ★★★★★★ |

| Waystream Holding | 22.09% | 113.25% | ★★★★★★ |

| CD Projekt | 24.92% | 27.00% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 131.08% | ★★★★★★ |

| JNTC | 29.48% | 104.37% | ★★★★★★ |

Click here to see the full list of 1276 stocks from our High Growth Tech and AI Stocks screener.

Here's a peek at a few of the choices from the screener.

Valneva (ENXTPA:VLA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Valneva SE is a specialty vaccine company focused on developing, manufacturing, and commercializing prophylactic vaccines for infectious diseases with unmet needs, and it has a market cap of €310.78 million.

Operations: Valneva SE focuses on the development, production, and sale of vaccines targeting infectious diseases that lack adequate prevention options. The company's revenue is primarily generated from its vaccine portfolio, although specific segment data is not detailed.

Valneva SE, amid a challenging backdrop of being unprofitable with a volatile share price, is navigating its path towards profitability with an expected revenue growth rate of 24.6% per year, outpacing the French market's 5.5%. This growth is underpinned by strategic moves like the recent licensing agreement with Serum Institute of India for its chikungunya vaccine during one of India's worst outbreaks, coupled with a $41.3 million funding boost from CEPI and the EU. Despite shareholder dilution over the past year and less than a year's cash runway posing financial constraints, Valneva's innovative strides in infectious diseases—evidenced by its robust R&D spending which remains crucial for future approvals and market expansions—are setting it apart in high-stakes markets.

- Get an in-depth perspective on Valneva's performance by reading our health report here.

Gain insights into Valneva's historical performance by reviewing our past performance report.

Empyrean Technology (SZSE:301269)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Empyrean Technology Co., Ltd. focuses on the development, sale, and servicing of electronic design automation (EDA) software, with a market cap of CN¥69.74 billion.

Operations: Empyrean Technology specializes in electronic design automation (EDA) software, generating revenue primarily through the development, sale, and servicing of these products. The company's operations are supported by a significant market presence with a market cap of CN¥69.74 billion.

Empyrean Technology has demonstrated a robust growth trajectory, with revenue surging by 27% annually, outpacing the broader CN market's 13.8%. This growth is bolstered by significant R&D investments, which are crucial for maintaining its competitive edge in the tech sector. Despite a challenging year with net income dropping to CNY 58.55 million from CNY 171.4 million, the company's commitment to innovation is evident in its recent presentation at the Tower Semiconductor Technical Global Symposium and its ongoing product development initiatives. These efforts underscore Empyrean's potential to navigate market fluctuations and capitalize on emerging tech trends.

- Click to explore a detailed breakdown of our findings in Empyrean Technology's health report.

Gain insights into Empyrean Technology's past trends and performance with our Past report.

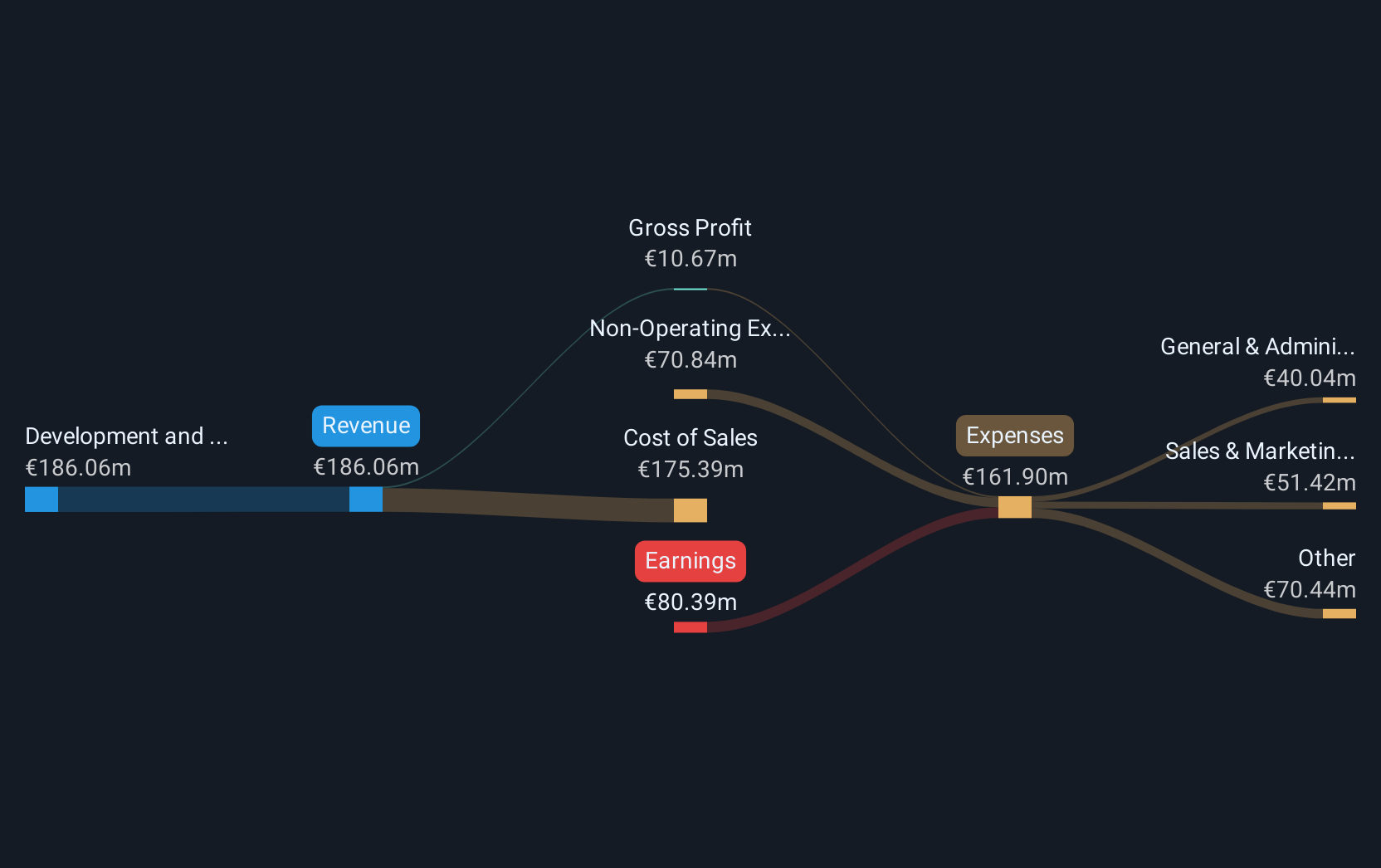

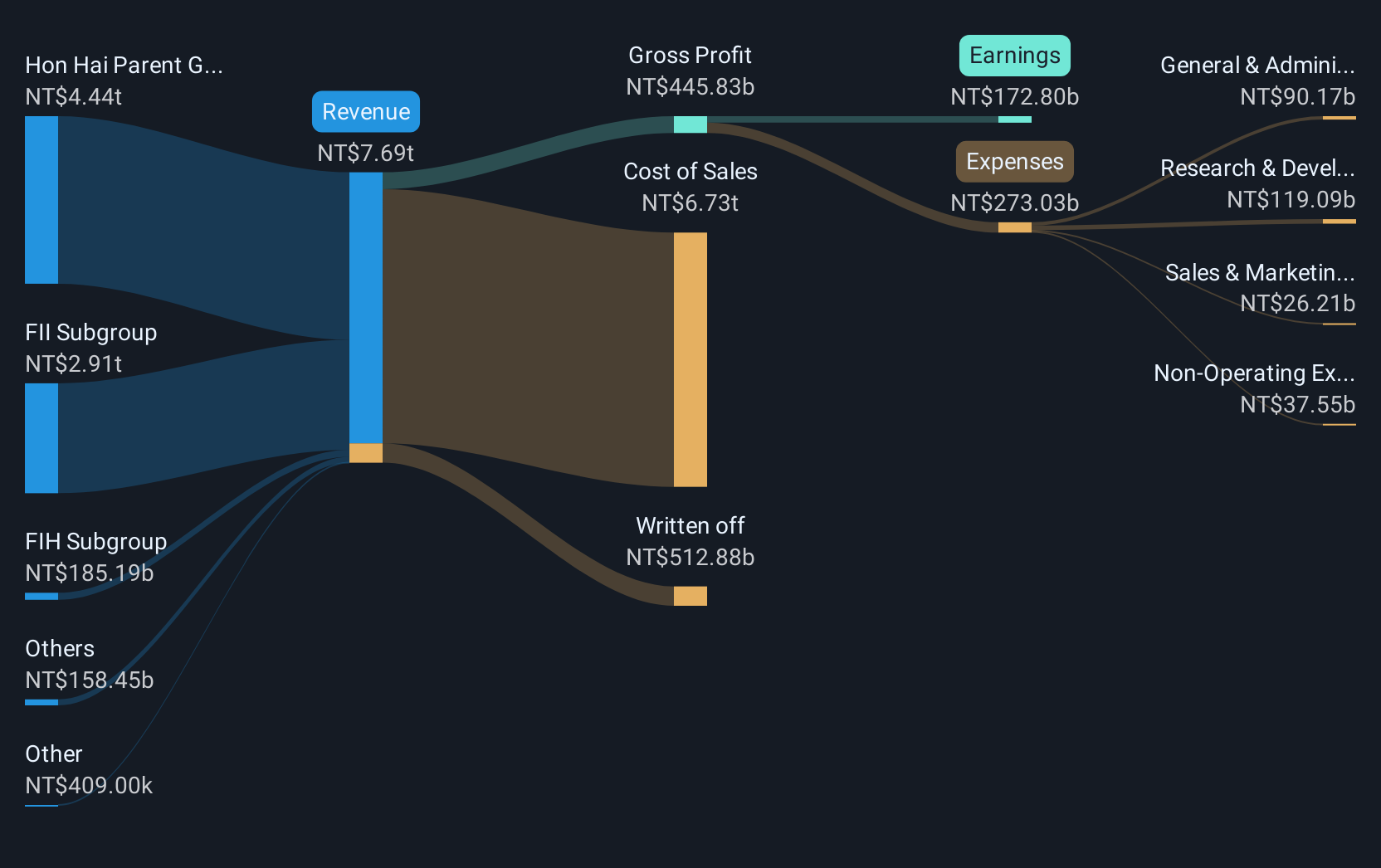

Hon Hai Precision Industry (TWSE:2317)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hon Hai Precision Industry Co., Ltd. offers electronic OEM services and has a market capitalization of NT$2.58 trillion.

Operations: Hon Hai Precision Industry Co., Ltd. generates significant revenue through its FII Subgroup and Foxconn Population, with the latter contributing NT$4.23 billion. The company's cost structure includes a notable amount written off, totaling NT$569.14 million.

Hon Hai Precision Industry, often recognized for its role in electronics manufacturing, is navigating an ambitious expansion into electric vehicles and tech integration. With a notable 18.2% annual revenue growth and an earnings increase of 20.05%, the company outperforms the broader Taiwanese market's growth rates. Recent strategic moves include pausing potential acquisitions amid industry consolidations, reflecting a cautious yet opportunistic approach to expansion. The firm's substantial R&D expenditure, integral to its innovation strategy, positions it well amidst evolving industry dynamics and customer demands in high-tech sectors.

Seize The Opportunity

- Gain an insight into the universe of 1276 High Growth Tech and AI Stocks by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hon Hai Precision Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2317

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor