Advertisement

As global markets navigate a choppy start to the year, marked by inflation concerns and political uncertainties, investors are closely watching growth stocks, which have recently underperformed compared to value counterparts. In such an environment, companies with high insider ownership can be appealing as they often indicate strong management confidence and alignment with shareholder interests.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.8% | 38.9% |

| CD Projekt (WSE:CDR) | 29.7% | 32.2% |

| Pharma Mar (BME:PHM) | 11.9% | 56.2% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 111.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.2% | 66.3% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 110.9% |

Let's take a closer look at a couple of our picks from the screened companies.

UTour Group (SZSE:002707)

Simply Wall St Growth Rating: ★★★★★★

Overview: UTour Group Co., Ltd. operates in the outbound tourism wholesale and retail sector both within China and internationally, with a market cap of CN¥7.03 billion.

Operations: UTour Group Co., Ltd. generates revenue from its outbound tourism wholesale and retail operations, serving both domestic and international markets.

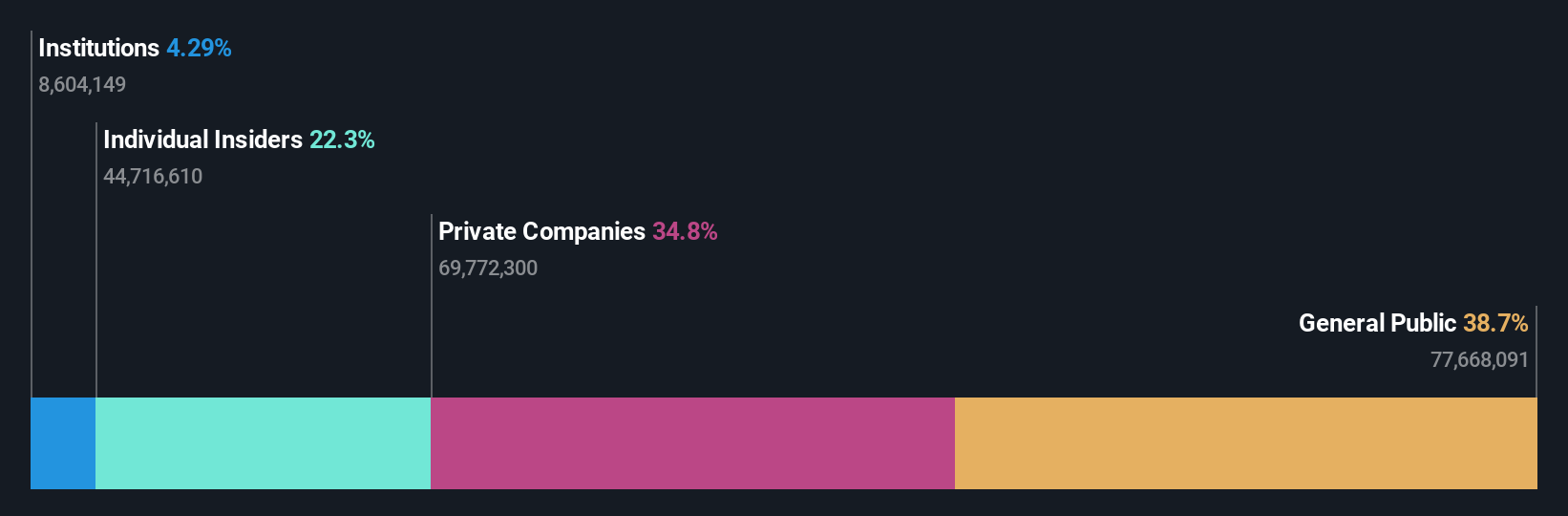

Insider Ownership: 24.1%

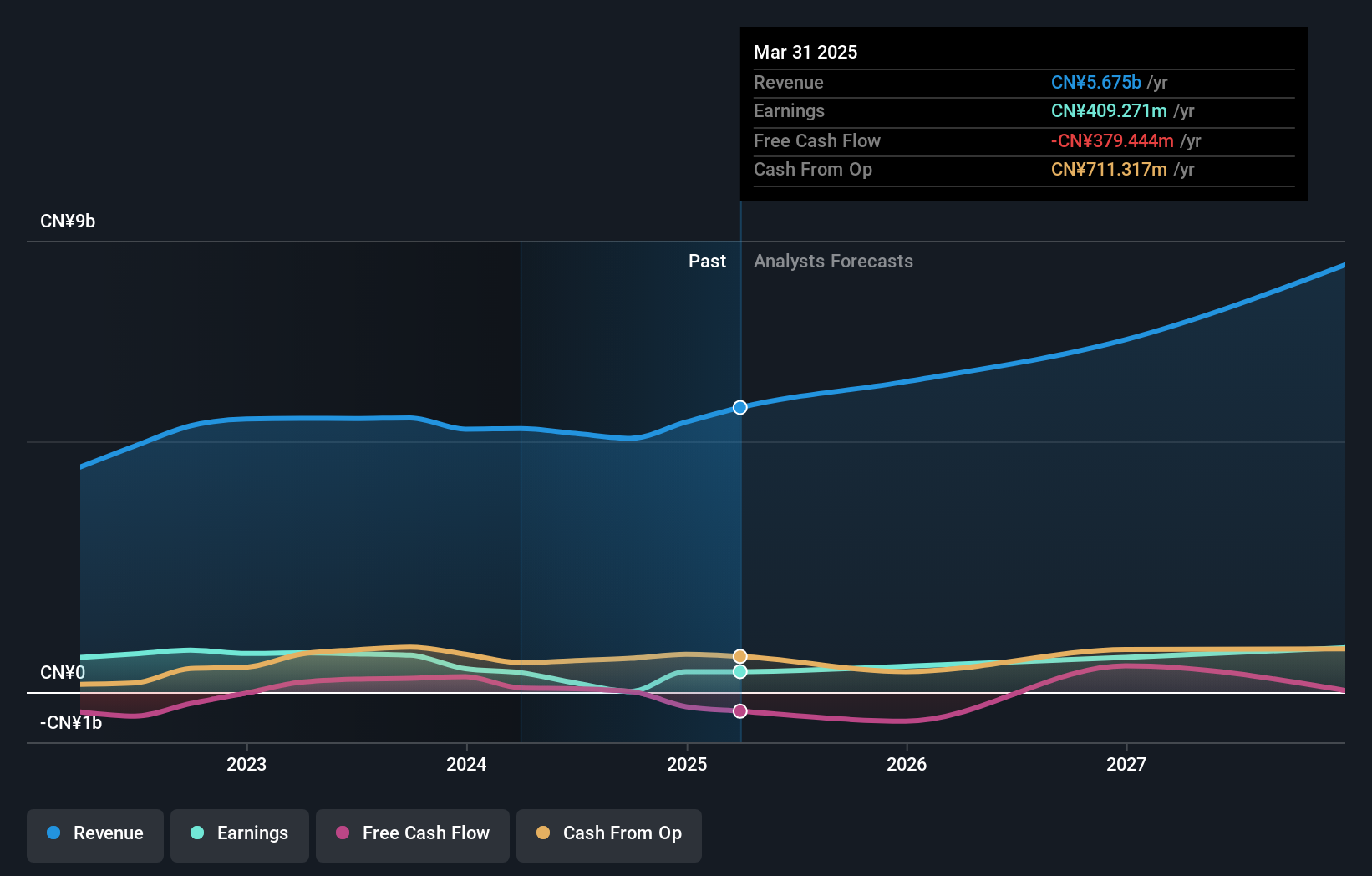

UTour Group has shown substantial growth, with recent earnings reports indicating a significant increase in revenue to CNY 4.72 billion and net income rising to CNY 123.5 million for the first nine months of 2024. The company is expected to maintain strong annual earnings growth of over 27%, outpacing the broader Chinese market. Additionally, UTour is trading significantly below its estimated fair value, suggesting potential upside as it continues its growth trajectory without notable insider selling activity recently.

- Unlock comprehensive insights into our analysis of UTour Group stock in this growth report.

- According our valuation report, there's an indication that UTour Group's share price might be on the expensive side.

Thunder Software TechnologyLtd (SZSE:300496)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Thunder Software Technology Co., Ltd. offers operating-system products across China, Europe, the United States, Japan, and other international markets with a market cap of CN¥24.71 billion.

Operations: Thunder Software Technology Co., Ltd. generates revenue from its operating-system products across various regions, including China, Europe, the United States, Japan, and other international markets.

Insider Ownership: 27.6%

Thunder Software Technology Ltd. is experiencing significant earnings growth, forecasted at 73.7% annually, surpassing the broader Chinese market's growth rate. Despite recent declines in revenue and net income, strategic partnerships like the one with HERE Technologies aim to enhance its intelligent navigation offerings and drive future expansion. The stock trades below estimated fair value, indicating potential investment appeal amid low profit margins and a forecasted low return on equity of 6.7%.

- Get an in-depth perspective on Thunder Software TechnologyLtd's performance by reading our analyst estimates report here.

- Our valuation report here indicates Thunder Software TechnologyLtd may be undervalued.

Hunan Sundy Science and Technology (SZSE:300515)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hunan Sundy Science and Technology Co., Ltd provides coal analysis solutions both within the People’s Republic of China and internationally, with a market cap of CN¥2.47 billion.

Operations: The company's revenue from the instrumentation industry is CN¥483.69 million.

Insider Ownership: 23.3%

Hunan Sundy Science and Technology is poised for robust growth, with earnings forecasted to rise 34.19% annually, outpacing the broader Chinese market. Recent amendments to its articles of association and board changes signal strategic alignment for future expansion. The company's revenue is expected to grow at 28% per year, exceeding market averages. Despite an unstable dividend history and a low forecasted return on equity of 19.7%, its price-to-earnings ratio suggests relative value within the industry.

- Dive into the specifics of Hunan Sundy Science and Technology here with our thorough growth forecast report.

- Our valuation report here indicates Hunan Sundy Science and Technology may be overvalued.

Turning Ideas Into Actions

- Unlock our comprehensive list of 1465 Fast Growing Companies With High Insider Ownership by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Thunder Software TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300496

Thunder Software TechnologyLtd

Provides operating-system products in China, Europe, the United States, Japan, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor