Advertisement

What Hangzhou Raycloud Technology Co.,Ltd's (SHSE:688365) 31% Share Price Gain Is Not Telling You

Hangzhou Raycloud Technology Co.,Ltd (SHSE:688365) shares have continued their recent momentum with a 31% gain in the last month alone. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 6.4% over the last year.

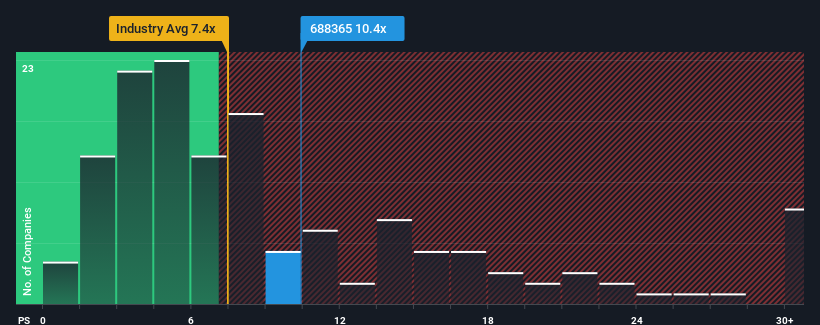

Following the firm bounce in price, you could be forgiven for thinking Hangzhou Raycloud TechnologyLtd is a stock not worth researching with a price-to-sales ratios (or "P/S") of 10.4x, considering almost half the companies in China's Software industry have P/S ratios below 7.4x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Hangzhou Raycloud TechnologyLtd

What Does Hangzhou Raycloud TechnologyLtd's P/S Mean For Shareholders?

There hasn't been much to differentiate Hangzhou Raycloud TechnologyLtd's and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to improve, justifying the currently elevated P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Hangzhou Raycloud TechnologyLtd's future stacks up against the industry? In that case, our free report is a great place to start.How Is Hangzhou Raycloud TechnologyLtd's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Hangzhou Raycloud TechnologyLtd's to be considered reasonable.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. The lack of growth did nothing to help the company's aggregate three-year performance, which is an unsavory 12% drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 20% over the next year. Meanwhile, the rest of the industry is forecast to expand by 31%, which is noticeably more attractive.

In light of this, it's alarming that Hangzhou Raycloud TechnologyLtd's P/S sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

What We Can Learn From Hangzhou Raycloud TechnologyLtd's P/S?

The large bounce in Hangzhou Raycloud TechnologyLtd's shares has lifted the company's P/S handsomely. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've concluded that Hangzhou Raycloud TechnologyLtd currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for Hangzhou Raycloud TechnologyLtd that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Raycloud TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688365

Hangzhou Raycloud TechnologyLtd

Operates as an e-commerce software and service technology company in China and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.5% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor