Advertisement

- Philippines

- /

- Banks

- /

- PSE:PNB

Undiscovered Gems in Global Markets for November 2025

Simply Wall St

Reviewed by Simply Wall St

In the current global market landscape, investor sentiment is heavily influenced by concerns over AI-related valuations and the potential for further interest rate cuts. Despite these challenges, small-cap indices like the S&P MidCap 400 and Russell 2000 have shown resilience, suggesting opportunities for discerning investors to uncover promising stocks that may be overlooked by broader market trends. In such an environment, a good stock often possesses strong fundamentals and growth potential that might not yet be fully recognized by the market.

Top 10 Undiscovered Gems With Strong Fundamentals Globally

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| YagiLtd | 27.83% | -6.06% | 32.03% | ★★★★★★ |

| Nantong Guosheng Intelligence Technology Group | NA | 5.01% | -3.27% | ★★★★★★ |

| Kanda HoldingsLtd | 23.54% | 3.84% | 10.38% | ★★★★★★ |

| MOBI Industry | 18.09% | 6.66% | 22.02% | ★★★★★★ |

| Nofoth Food Products | NA | 15.49% | 26.47% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 3.26% | 17.17% | 23.30% | ★★★★★★ |

| Orient Pharma | 0.12% | 26.97% | 72.60% | ★★★★★★ |

| Najran Cement | 14.49% | -4.20% | -30.16% | ★★★★★★ |

| Otec | 8.45% | 6.58% | 18.86% | ★★★★★☆ |

| Etihad Atheeb Telecommunication | 0.97% | 38.36% | 57.78% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

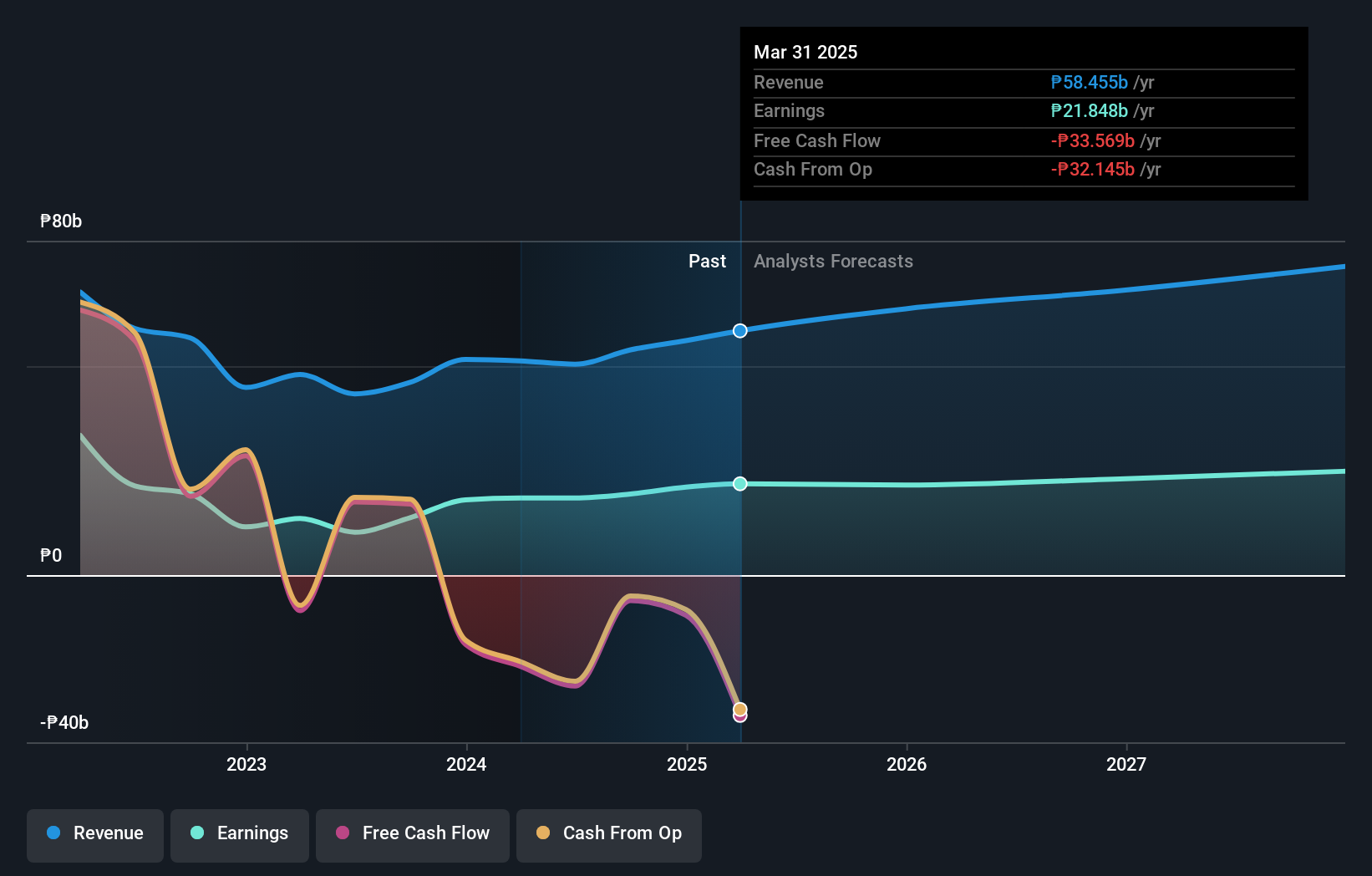

Philippine National Bank (PSE:PNB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Philippine National Bank offers a range of banking and financial products and services with a market capitalization of approximately ₱79.87 billion.

Operations: Philippine National Bank generates revenue primarily through its Retail Banking and Corporate Banking segments, contributing approximately ₱35.10 billion and ₱14.49 billion, respectively. The Treasury segment adds another significant portion with around ₱12.50 billion in revenue.

Philippine National Bank, with total assets of ₱1,249.1 billion and equity of ₱234 billion, is a notable player in the banking sector. Total deposits stand at ₱949.5 billion against loans of ₱652.5 billion, supported by a net interest margin of 4.5%. The bank's earnings surged 26.3% over the past year, outpacing the industry growth rate of 7.6%, although it contends with high non-performing loans at 6.5%. Despite trading at a good value and having primarily low-risk funding sources (94% from customer deposits), its allowance for bad loans remains insufficient at 82%.

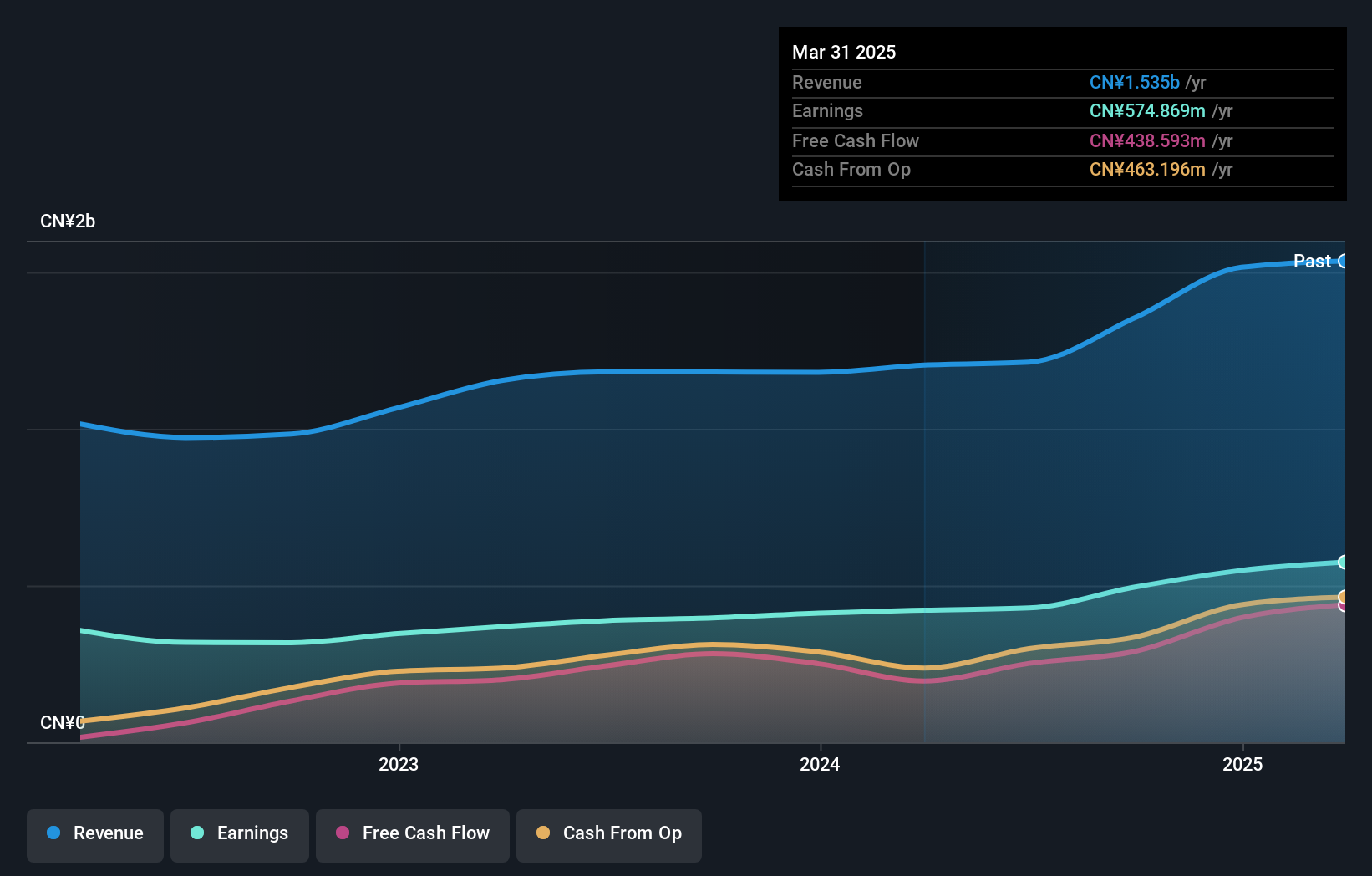

Henan Thinker Automatic EquipmentLtd (SHSE:603508)

Simply Wall St Value Rating: ★★★★★☆

Overview: Henan Thinker Automatic Equipment Co., Ltd. specializes in the development and manufacturing of automation equipment, with a market capitalization of CN¥10.12 billion.

Operations: Henan Thinker generates revenue primarily from its Software and Information Technology Services segment, amounting to CN¥1.56 billion.

Henan Thinker Automatic Equipment, a small cap player in the machinery sector, has shown robust earnings growth of 24.6% over the past year, outpacing the industry's 6.3%. The firm's debt to equity ratio is minimal at 0.8%, and it holds more cash than its total debt, suggesting a strong financial position. In recent results for the nine months ending September 2025, sales reached CNY 953 million from CNY 906 million last year, with net income climbing to CNY 396 million from CNY 328 million. Basic earnings per share increased to CNY 1.04 from CNY 0.86 previously reported.

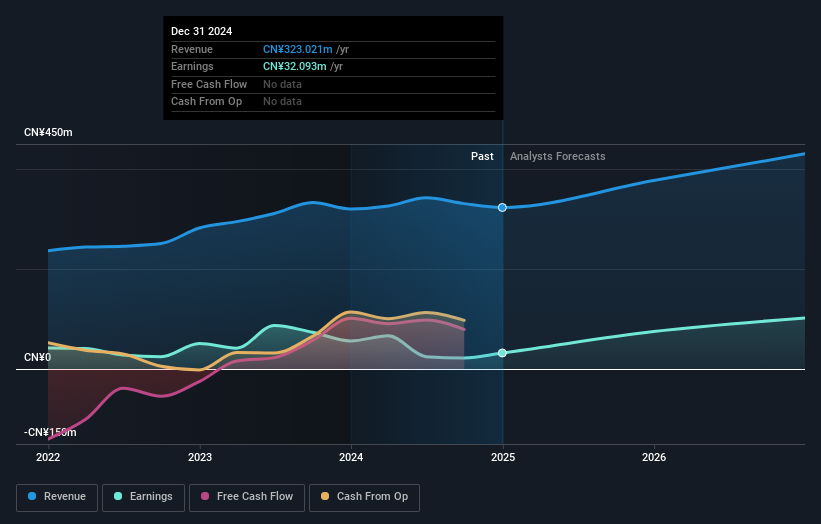

Jiangsu Eazytec (SHSE:688258)

Simply Wall St Value Rating: ★★★★★☆

Overview: Jiangsu Eazytec Co., Ltd. specializes in providing core firmware products for cloud computing equipment both in China and internationally, with a market capitalization of CN¥7.38 billion.

Operations: Eazytec generates revenue primarily from its core firmware products for cloud computing equipment. The company's financial performance is highlighted by a net profit margin of 15.2%, reflecting its profitability in the competitive tech industry.

Jiangsu Eazytec's recent financial performance highlights its potential as a promising player in the IT sector. Over the past year, earnings surged by 158.5%, significantly outpacing the industry average of -12.9%. The company reported net income of CN¥44.6 million for the nine months ending September 2025, a noticeable increase from CN¥20.09 million a year earlier, with basic earnings per share climbing to CN¥0.37 from CN¥0.17. Despite its volatile share price recently, Jiangsu Eazytec's strategic moves and strong EBIT coverage of interest payments (7.2x) suggest robust operational efficiency and financial health amidst market fluctuations.

- Get an in-depth perspective on Jiangsu Eazytec's performance by reading our health report here.

Review our historical performance report to gain insights into Jiangsu Eazytec's's past performance.

Next Steps

- Reveal the 3011 hidden gems among our Global Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About PSE:PNB

Philippine National Bank

Provides various banking and financial products and services.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative