- China

- /

- Commercial Services

- /

- SZSE:001267

Insiders Favor These 3 Growth Companies

Reviewed by Simply Wall St

As global markets show resilience with U.S. indexes nearing record highs and broad-based gains across sectors, investors are increasingly focused on the implications of geopolitical tensions and economic policies. In this environment, companies with high insider ownership can be particularly appealing as they often signal confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| SKS Technologies Group (ASX:SKS) | 32.4% | 24.8% |

| On Holding (NYSE:ONON) | 19.1% | 29.6% |

| Pharma Mar (BME:PHM) | 11.8% | 56.9% |

| Medley (TSE:4480) | 34% | 31.7% |

| Findi (ASX:FND) | 34.8% | 71.5% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 103.6% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

| Alkami Technology (NasdaqGS:ALKT) | 11% | 98.6% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

We'll examine a selection from our screener results.

SK oceanplantLtd (KOSE:A100090)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SK oceanplant Co., Ltd. operates in South Korea, focusing on the manufacturing of steel and stainless steel pipes, hull blocks, and shipbuilding equipment, with a market cap of ₩709.16 billion.

Operations: The company's revenue segments include the production of steel and stainless steel pipes, hull blocks, and shipbuilding equipment.

Insider Ownership: 20.7%

Revenue Growth Forecast: 21.3% p.a.

SK oceanplant Ltd. is poised for significant growth, with earnings expected to rise over 36% annually, outpacing the Korean market's 29.5%. Revenue growth is also forecasted at 21.3%, surpassing the market average of 9.3%. Despite this positive outlook, return on equity remains low at a projected 10% in three years and profit margins have declined from last year. Recent earnings reports show increased sales but a decrease in net income over nine months compared to the previous year.

- Dive into the specifics of SK oceanplantLtd here with our thorough growth forecast report.

- According our valuation report, there's an indication that SK oceanplantLtd's share price might be on the expensive side.

Piesat Information Technology (SHSE:688066)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Piesat Information Technology Co., Ltd. offers satellite internet services in China and has a market cap of CN¥6.07 billion.

Operations: The company's revenue primarily comes from its Satellite Application segment, amounting to CN¥1.58 billion.

Insider Ownership: 21.6%

Revenue Growth Forecast: 28.5% p.a.

Piesat Information Technology is set for rapid expansion, with revenue projected to grow 28.5% annually, exceeding the Chinese market's 13.8%. Despite this growth potential, the company faces challenges with a net loss of CNY 221.8 million reported for the nine months ending September 2024 and a volatile share price recently. The company's financial position shows that debt is not well covered by operating cash flow, and return on equity is forecasted to be low at 9.3% in three years.

- Take a closer look at Piesat Information Technology's potential here in our earnings growth report.

- The valuation report we've compiled suggests that Piesat Information Technology's current price could be quite moderate.

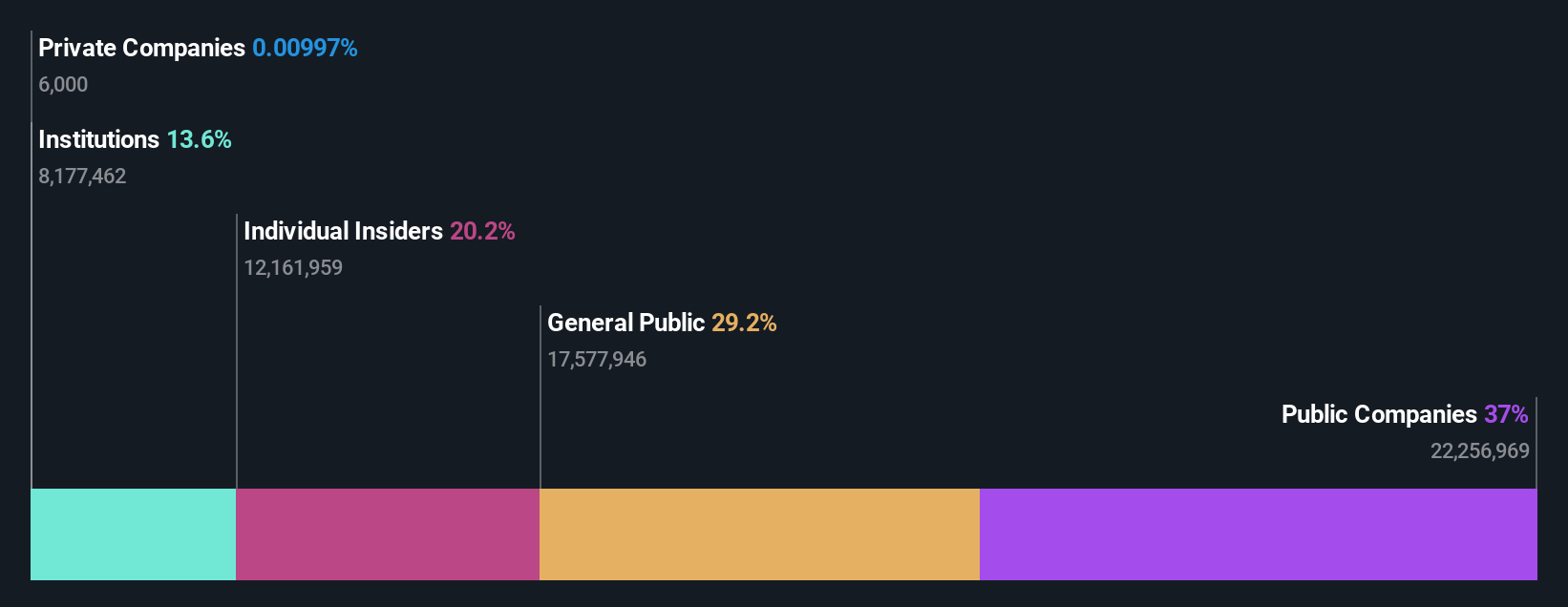

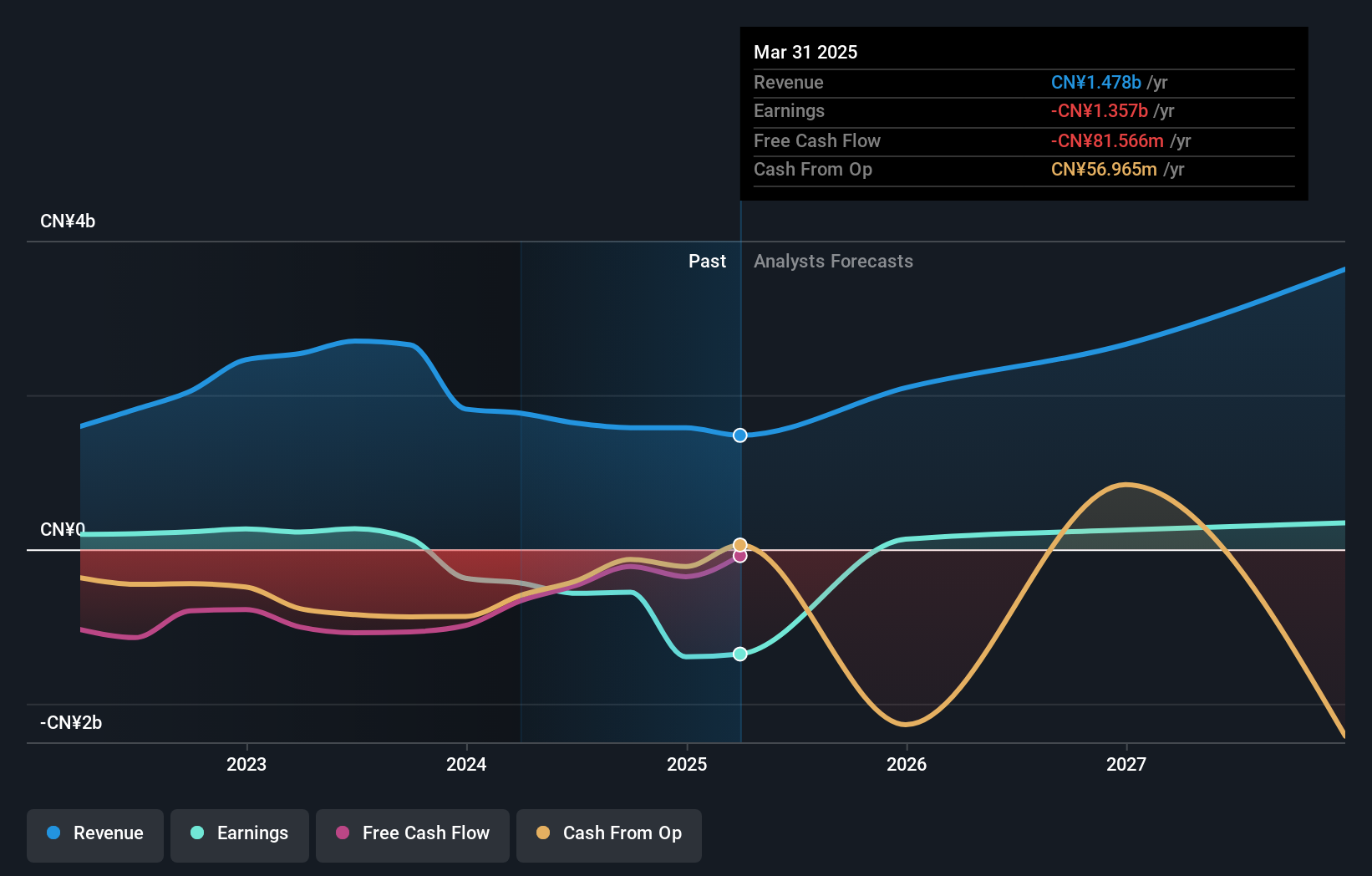

Hui Lyu Ecological Technology GroupsLtd (SZSE:001267)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hui Lyu Ecological Technology Groups Co., Ltd. operates in the ecological technology sector and has a market cap of approximately CN¥5.64 billion.

Operations: Unfortunately, the provided text does not include specific revenue segment information for Hui Lyu Ecological Technology Groups Co., Ltd. If you can provide the details of their revenue segments, I would be able to summarize them for you.

Insider Ownership: 34.7%

Revenue Growth Forecast: 17.4% p.a.

Hui Lyu Ecological Technology Groups Ltd. is poised for significant earnings growth, forecasted at 41.5% annually, outpacing the broader Chinese market's 26.1%. Despite a decline in sales to CNY 353.19 million for the first nine months of 2024, net income increased slightly to CNY 26.26 million. The stock trades at a discount to its estimated fair value and recent board changes could influence strategic direction, though dividend stability remains uncertain due to an unstable track record.

- Navigate through the intricacies of Hui Lyu Ecological Technology GroupsLtd with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that Hui Lyu Ecological Technology GroupsLtd is trading beyond its estimated value.

Seize The Opportunity

- Investigate our full lineup of 1519 Fast Growing Companies With High Insider Ownership right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hui Lyu Ecological Technology GroupsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:001267

Hui Lyu Ecological Technology GroupsLtd

Hui Lyu Ecological Technology Groups Co.,Ltd.

Reasonable growth potential with mediocre balance sheet.