Advertisement

- China

- /

- Semiconductors

- /

- SZSE:300751

Suzhou Maxwell Technologies Co., Ltd.'s (SZSE:300751) P/E Still Appears To Be Reasonable

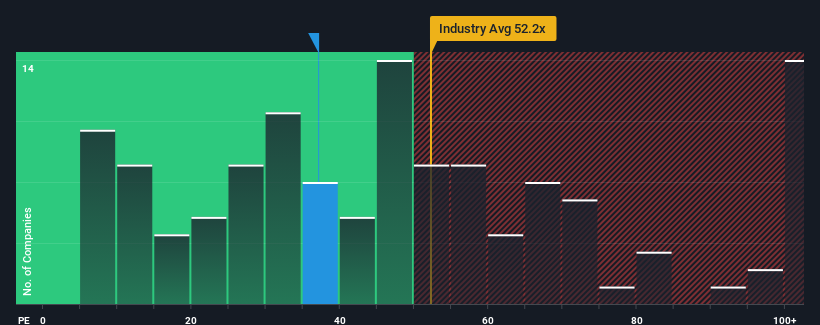

Suzhou Maxwell Technologies Co., Ltd.'s (SZSE:300751) price-to-earnings (or "P/E") ratio of 37.1x might make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 28x and even P/E's below 17x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

There hasn't been much to differentiate Suzhou Maxwell Technologies' and the market's retreating earnings lately. One possibility is that the P/E is high because investors think the company can turn things around and break free from the broader downward trend in earnings. If not, then existing shareholders may be a little nervous about the viability of the share price.

View our latest analysis for Suzhou Maxwell Technologies

Is There Enough Growth For Suzhou Maxwell Technologies?

There's an inherent assumption that a company should outperform the market for P/E ratios like Suzhou Maxwell Technologies' to be considered reasonable.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. However, a few strong years before that means that it was still able to grow EPS by an impressive 126% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 29% per annum as estimated by the analysts watching the company. That's shaping up to be materially higher than the 22% per year growth forecast for the broader market.

With this information, we can see why Suzhou Maxwell Technologies is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Suzhou Maxwell Technologies' P/E

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Suzhou Maxwell Technologies' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you take the next step, you should know about the 3 warning signs for Suzhou Maxwell Technologies (1 is a bit unpleasant!) that we have uncovered.

If you're unsure about the strength of Suzhou Maxwell Technologies' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300751

Suzhou Maxwell Technologies

Engages in the design, research and development, production, and sale of solar cell production equipment in China.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor