- China

- /

- Semiconductors

- /

- SZSE:300661

3 High-Ownership Growth Companies With Earnings Up To 40%

Reviewed by Simply Wall St

As global markets react to tariff uncertainties and mixed economic signals, investors are closely monitoring earnings reports, with many companies surpassing expectations despite broader market challenges. In this environment, stocks with high insider ownership can be particularly appealing, as they often indicate strong confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 50.8% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 119.4% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 111.4% |

We're going to check out a few of the best picks from our screener tool.

Kuaishou Technology (SEHK:1024)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kuaishou Technology is an investment holding company offering live streaming, online marketing, and other services in the People’s Republic of China, with a market cap of approximately HK$199.93 billion.

Operations: The company generates revenue from its domestic operations amounting to CN¥119.83 billion and overseas activities totaling CN¥4.25 billion.

Insider Ownership: 19.6%

Earnings Growth Forecast: 16.7% p.a.

Kuaishou Technology demonstrates strong growth potential with earnings projected to outpace the Hong Kong market, growing at 16.7% annually. The company trades at a substantial discount to its estimated fair value and offers good relative value compared to peers. Recent innovations, such as Kling AI's multi-image reference feature, enhance its product offerings and expand monetization opportunities. Despite no significant insider trading activity recently, Kuaishou maintains robust insider ownership levels supporting aligned interests with shareholders.

- Click here and access our complete growth analysis report to understand the dynamics of Kuaishou Technology.

- Our valuation report here indicates Kuaishou Technology may be undervalued.

Qi An Xin Technology Group (SHSE:688561)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Qi An Xin Technology Group Inc. is a cybersecurity company that offers products and services to government, enterprises, and other institutions both in China and internationally, with a market cap of approximately CN¥23.14 billion.

Operations: The company generates revenue primarily from its Information Security Industry segment, amounting to CN¥5.47 billion.

Insider Ownership: 22%

Earnings Growth Forecast: 38.5% p.a.

Qi An Xin Technology Group exhibits promising growth prospects, with earnings expected to grow significantly at 38.5% annually, outpacing the Chinese market. The company trades at a substantial discount to its estimated fair value and shows good relative value compared to peers. Despite recent share price volatility and low forecasted return on equity, Qi An Xin's profitability this year marks a positive shift. No significant insider trading activity was noted recently, but insider ownership remains high.

- Delve into the full analysis future growth report here for a deeper understanding of Qi An Xin Technology Group.

- Insights from our recent valuation report point to the potential undervaluation of Qi An Xin Technology Group shares in the market.

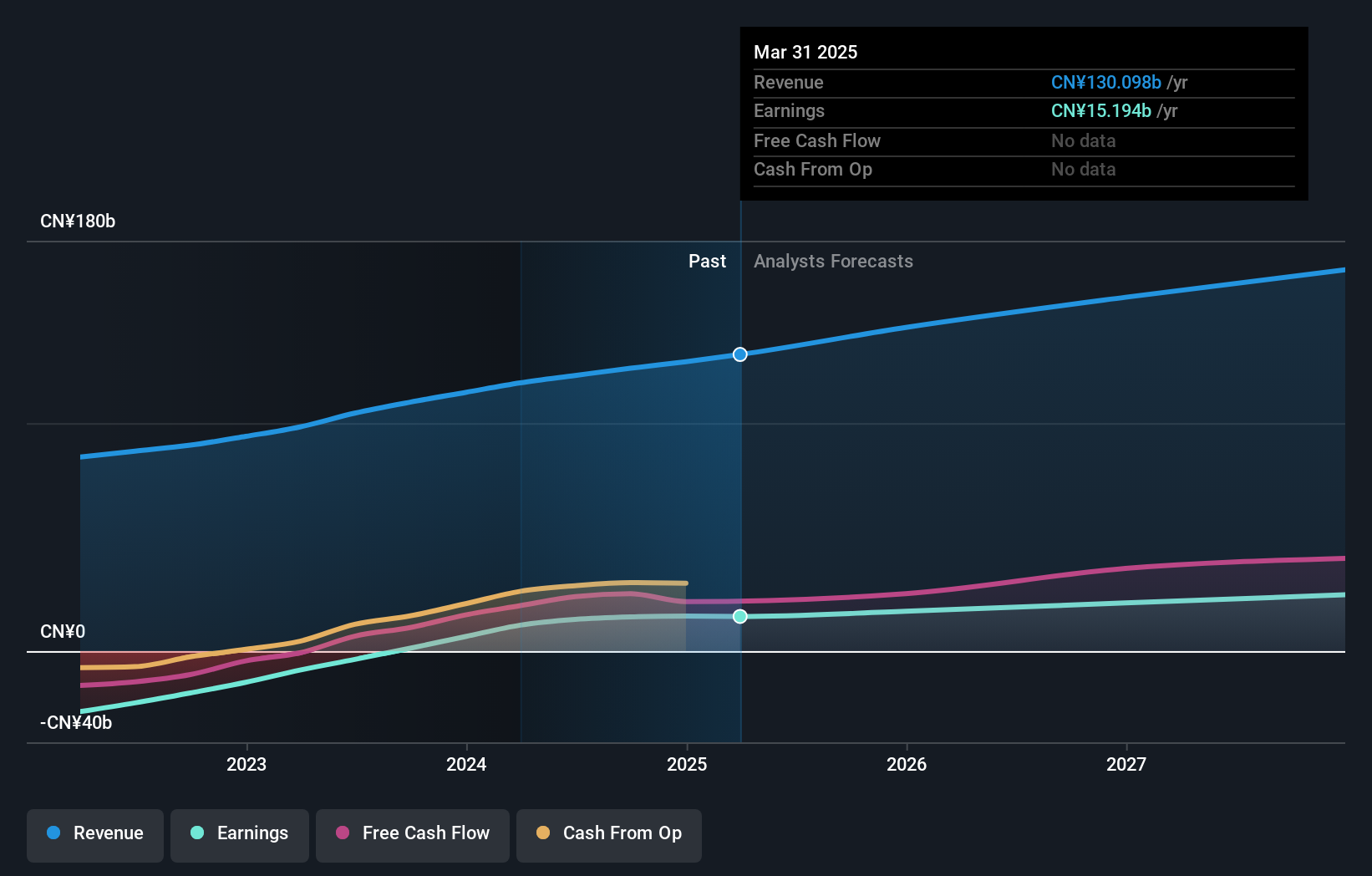

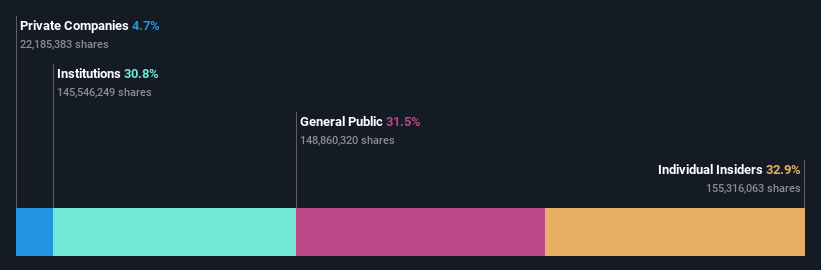

SG Micro (SZSE:300661)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SG Micro Corp designs, markets, and sells analog ICs primarily in China with a market cap of CN¥46.87 billion.

Operations: The company's revenue from the Integrated Circuit Industry segment is CN¥3.18 billion.

Insider Ownership: 32.9%

Earnings Growth Forecast: 40% p.a.

SG Micro's earnings are projected to grow significantly at 40% annually, surpassing the Chinese market. Revenue is also expected to rise by 22% per year, outpacing market averages. Despite a volatile share price and low forecasted return on equity of 16.4%, insider ownership remains substantial with no recent significant trading activity. The company's robust growth outlook positions it well within the competitive landscape, though potential investors should consider volatility risks.

- Dive into the specifics of SG Micro here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential overvaluation of SG Micro shares in the market.

Next Steps

- Click here to access our complete index of 1453 Fast Growing Companies With High Insider Ownership.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300661

High growth potential with solid track record.

Market Insights

Community Narratives