Advertisement

- China

- /

- Semiconductors

- /

- SZSE:300393

Jolywood (Suzhou) Sunwatt Co., Ltd. (SZSE:300393) Could Be Riskier Than It Looks

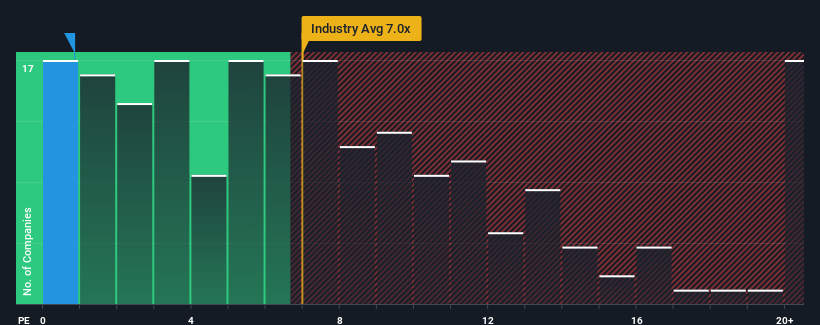

You may think that with a price-to-sales (or "P/S") ratio of 0.8x Jolywood (Suzhou) Sunwatt Co., Ltd. (SZSE:300393) is definitely a stock worth checking out, seeing as almost half of all the Semiconductor companies in China have P/S ratios greater than 7x and even P/S above 12x aren't out of the ordinary. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Jolywood (Suzhou) Sunwatt

How Has Jolywood (Suzhou) Sunwatt Performed Recently?

Jolywood (Suzhou) Sunwatt certainly has been doing a good job lately as it's been growing revenue more than most other companies. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Jolywood (Suzhou) Sunwatt will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Jolywood (Suzhou) Sunwatt would need to produce anemic growth that's substantially trailing the industry.

Retrospectively, the last year delivered an exceptional 26% gain to the company's top line. Pleasingly, revenue has also lifted 154% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 59% as estimated by the one analyst watching the company. With the industry only predicted to deliver 34%, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that Jolywood (Suzhou) Sunwatt's P/S sits behind most of its industry peers. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

To us, it seems Jolywood (Suzhou) Sunwatt currently trades on a significantly depressed P/S given its forecasted revenue growth is higher than the rest of its industry. There could be some major risk factors that are placing downward pressure on the P/S ratio. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Jolywood (Suzhou) Sunwatt you should know about.

If these risks are making you reconsider your opinion on Jolywood (Suzhou) Sunwatt, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300393

Jolywood (Suzhou) SunwattLtd

Manufactures and sells integrated photovoltaic (PV) products worldwide.

Second-rate dividend payer low.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor