Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688515

Motorcomm Electronic Technology Co., Ltd. (SHSE:688515) Stock Rockets 25% As Investors Are Less Pessimistic Than Expected

Motorcomm Electronic Technology Co., Ltd. (SHSE:688515) shareholders would be excited to see that the share price has had a great month, posting a 25% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 90% in the last year.

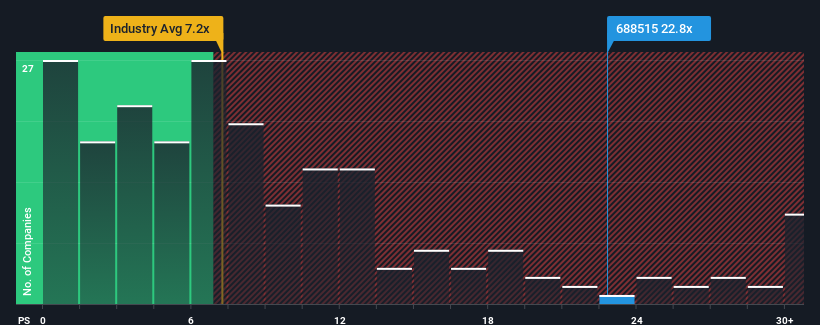

Following the firm bounce in price, Motorcomm Electronic Technology may be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 22.8x, since almost half of all companies in the Semiconductor industry in China have P/S ratios under 7.2x and even P/S lower than 3x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for Motorcomm Electronic Technology

What Does Motorcomm Electronic Technology's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, Motorcomm Electronic Technology has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. If not, then existing shareholders might be a little nervous about the viability of the share price.

Keen to find out how analysts think Motorcomm Electronic Technology's future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For Motorcomm Electronic Technology?

The only time you'd be truly comfortable seeing a P/S as steep as Motorcomm Electronic Technology's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that the company grew revenue by an impressive 40% last year. Pleasingly, revenue has also lifted 48% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 52% over the next year. Meanwhile, the rest of the industry is forecast to expand by 50%, which is not materially different.

In light of this, it's curious that Motorcomm Electronic Technology's P/S sits above the majority of other companies. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

The Final Word

The strong share price surge has lead to Motorcomm Electronic Technology's P/S soaring as well. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Given Motorcomm Electronic Technology's future revenue forecasts are in line with the wider industry, the fact that it trades at an elevated P/S is somewhat surprising. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

You always need to take note of risks, for example - Motorcomm Electronic Technology has 2 warning signs we think you should be aware of.

If you're unsure about the strength of Motorcomm Electronic Technology's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688515

Motorcomm Electronic Technology

Motorcomm Electronic Technology Co., Ltd.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|6.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|25.8% undervalued

KA

Community Contributor