Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688259

Triductor Technology (Suzhou) Inc.'s (SHSE:688259) Stock Retreats 26% But Earnings Haven't Escaped The Attention Of Investors

The Triductor Technology (Suzhou) Inc. (SHSE:688259) share price has fared very poorly over the last month, falling by a substantial 26%. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 48% share price drop.

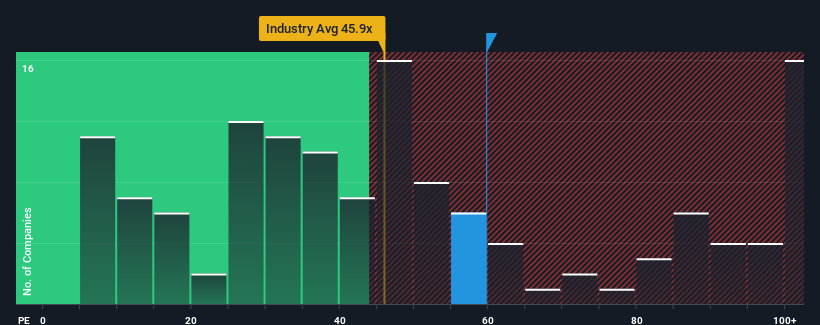

Although its price has dipped substantially, Triductor Technology (Suzhou) may still be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 59.7x, since almost half of all companies in China have P/E ratios under 27x and even P/E's lower than 17x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Triductor Technology (Suzhou) could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

See our latest analysis for Triductor Technology (Suzhou)

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Triductor Technology (Suzhou)'s is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 35%. As a result, earnings from three years ago have also fallen 34% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the one analyst covering the company suggest earnings should grow by 69% over the next year. With the market only predicted to deliver 36%, the company is positioned for a stronger earnings result.

With this information, we can see why Triductor Technology (Suzhou) is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Triductor Technology (Suzhou)'s P/E?

A significant share price dive has done very little to deflate Triductor Technology (Suzhou)'s very lofty P/E. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Triductor Technology (Suzhou)'s analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Triductor Technology (Suzhou) has 2 warning signs we think you should be aware of.

If these risks are making you reconsider your opinion on Triductor Technology (Suzhou), explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Triductor Technology (Suzhou) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688259

Triductor Technology (Suzhou)

A semiconductor company, designs and provides mixed-signal integrated circuits, and related hardware and software applications.

Excellent balance sheet low.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor