Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688048

3 Global Growth Companies Insiders Own With Up To 93% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate a complex landscape marked by record highs in major U.S. indices and fluctuating economic indicators, investors are keenly observing growth opportunities that align with these evolving conditions. In this environment, companies with high insider ownership often stand out as potentially strong contenders for growth, as insider confidence can be a compelling indicator of future prospects amidst the broader market dynamics.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15.6% | 60.5% |

| Shanghai Huace Navigation Technology (SZSE:300627) | 24.3% | 23.5% |

| Pharma Mar (BME:PHM) | 11.8% | 44.9% |

| Novoray (SHSE:688300) | 23.6% | 27.1% |

| Laopu Gold (SEHK:6181) | 35.5% | 41.8% |

| KebNi (OM:KEBNI B) | 38.3% | 94.5% |

| Fulin Precision (SZSE:300432) | 13.6% | 43.7% |

| Elliptic Laboratories (OB:ELABS) | 24.4% | 79% |

| Circus (XTRA:CA1) | 24.7% | 94.8% |

| Bergen Carbon Solutions (OB:BCS) | 12% | 63.2% |

Here we highlight a subset of our preferred stocks from the screener.

DigiPlus Interactive (PSE:PLUS)

Simply Wall St Growth Rating: ★★★★★☆

Overview: DigiPlus Interactive Corp., with a market cap of ₱178.85 billion, operates as a digital entertainment company in the Philippines through its subsidiaries.

Operations: The company's revenue segments include the Casino Group at ₱503.77 million, Retail Group at ₱83.81 billion, and Network and License Group at ₱414.68 million.

Insider Ownership: 11.7%

Earnings Growth Forecast: 23.2% p.a.

DigiPlus Interactive is expanding into Brazil, targeting a gaming market twice the size of the Philippines, enhancing its growth prospects. The company's earnings are forecast to grow significantly at 23.17% annually, outpacing the Philippine market's 10.9%. Despite recent share price volatility, DigiPlus trades at good value compared to peers and industry standards. Recent announcements include a PHP 6 billion share buyback program and strategic executive appointments to bolster its expansion efforts.

- Click here to discover the nuances of DigiPlus Interactive with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that DigiPlus Interactive is priced lower than what may be justified by its financials.

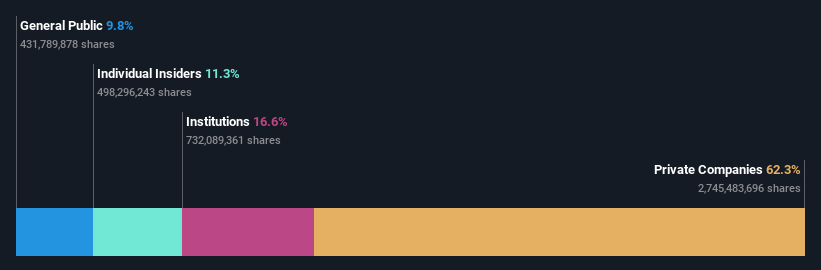

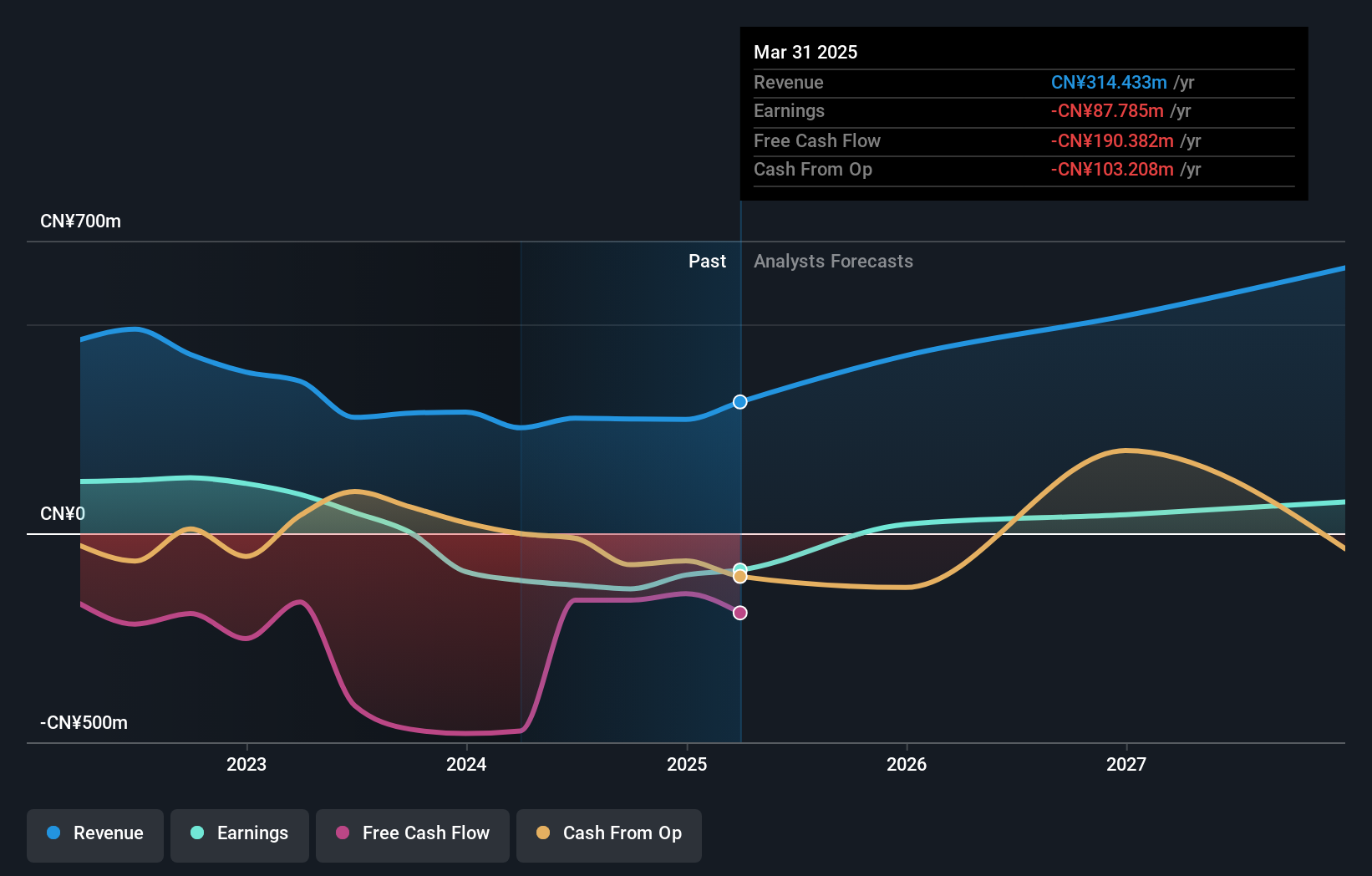

Suzhou Everbright Photonics (SHSE:688048)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Suzhou Everbright Photonics Co., Ltd. engages in the research, development, design, production, and sale of semiconductor laser chips both in China and internationally, with a market cap of CN¥10.58 billion.

Operations: The company generates revenue primarily from the research, development, design, production, and sale of semiconductor laser chips both domestically and internationally.

Insider Ownership: 10.8%

Earnings Growth Forecast: 93.7% p.a.

Suzhou Everbright Photonics is poised for substantial growth, with revenue projected to increase by 24.2% annually, outpacing the Chinese market's 12.4%. Despite a current net loss of CNY 7.5 million in Q1 2025, this marks an improvement from the previous year's loss of CNY 19.45 million. The company is expected to achieve profitability within three years and has not experienced significant insider trading recently, indicating stable insider confidence during its growth phase.

- Click to explore a detailed breakdown of our findings in Suzhou Everbright Photonics' earnings growth report.

- The analysis detailed in our Suzhou Everbright Photonics valuation report hints at an inflated share price compared to its estimated value.

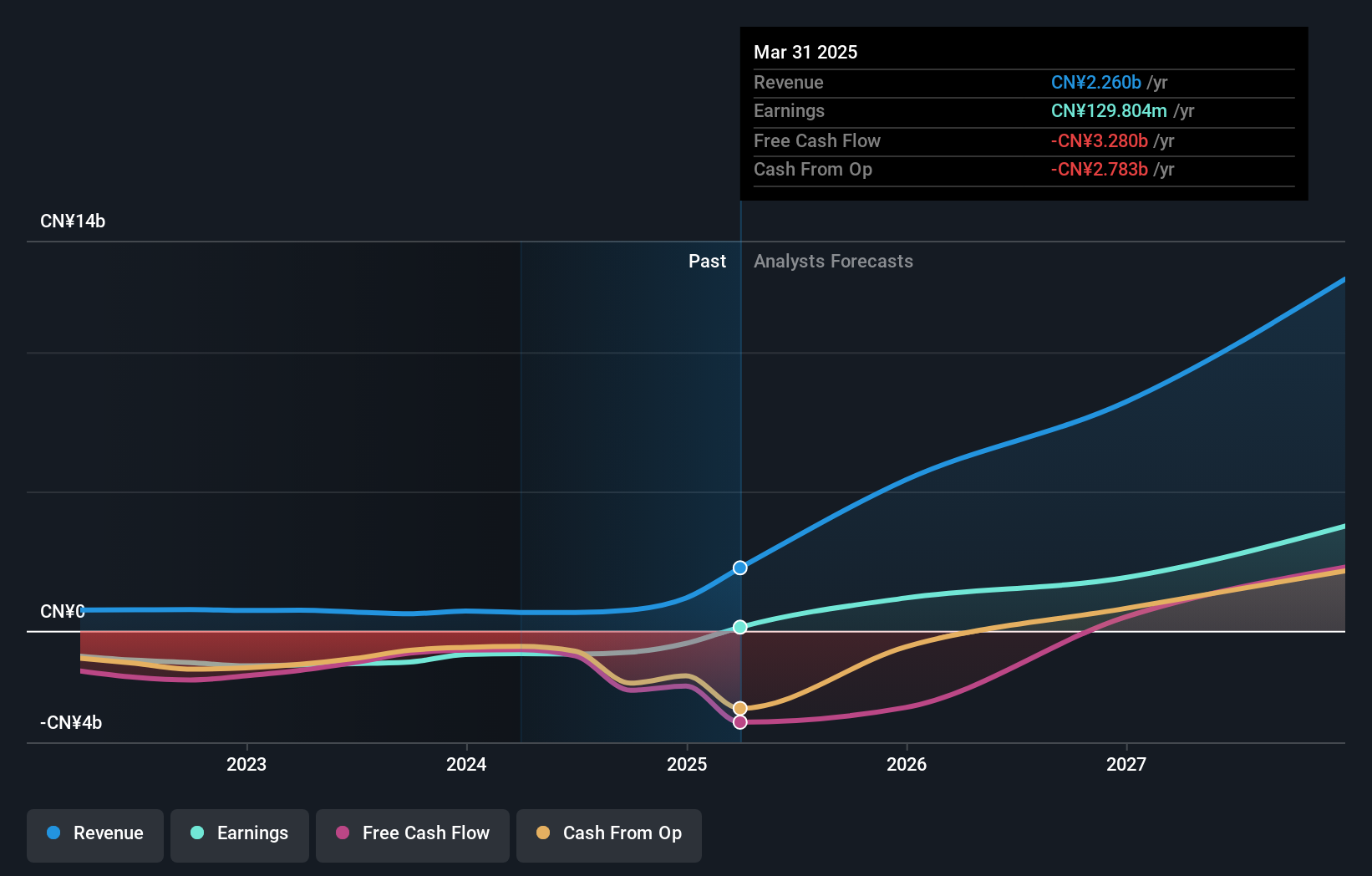

Cambricon Technologies (SHSE:688256)

Simply Wall St Growth Rating: ★★★★★★

Overview: Cambricon Technologies Corporation Limited focuses on researching, developing, designing, and selling core chips for cloud servers, edge computing, and terminal equipment in China with a market cap of CN¥218.88 billion.

Operations: Cambricon Technologies generates revenue from the research, development, design, and sale of core chips utilized in cloud servers, edge computing, and terminal equipment within China.

Insider Ownership: 28.6%

Earnings Growth Forecast: 71.1% p.a.

Cambricon Technologies is experiencing robust growth, with earnings projected to rise significantly at 71.1% annually, surpassing the Chinese market's average. The company recently turned profitable, reporting Q1 2025 net income of CNY 355.47 million, a stark contrast to last year's loss. Despite being removed from the Shanghai Stock Exchange 180 Value Index in June 2025, Cambricon announced a substantial private placement aiming to raise up to CNY 4.98 billion, reflecting strategic expansion efforts amidst high insider ownership stability.

- Unlock comprehensive insights into our analysis of Cambricon Technologies stock in this growth report.

- Our valuation report unveils the possibility Cambricon Technologies' shares may be trading at a premium.

Where To Now?

- Unlock more gems! Our Fast Growing Global Companies With High Insider Ownership screener has unearthed 825 more companies for you to explore.Click here to unveil our expertly curated list of 828 Fast Growing Global Companies With High Insider Ownership.

- Searching for a Fresh Perspective? Outshine the giants: these 23 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688048

Suzhou Everbright Photonics

Researches and develops, designs, produces, and sells semiconductor laser chips in China and internationally.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor