Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688233

Thinkon Semiconductor Jinzhou Corp. (SHSE:688233) Stocks Shoot Up 28% But Its P/S Still Looks Reasonable

Despite an already strong run, Thinkon Semiconductor Jinzhou Corp. (SHSE:688233) shares have been powering on, with a gain of 28% in the last thirty days. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 28% over that time.

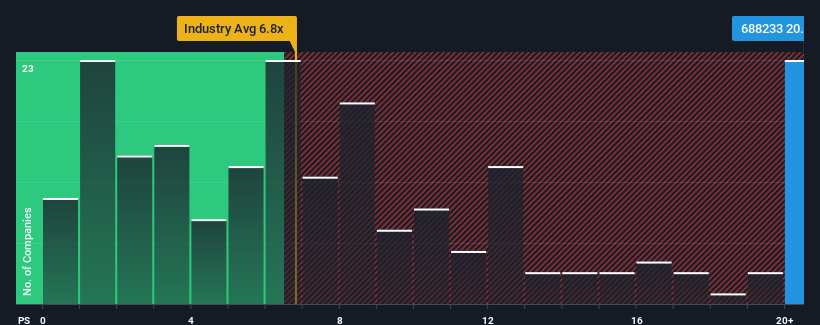

Following the firm bounce in price, Thinkon Semiconductor Jinzhou's price-to-sales (or "P/S") ratio of 20.5x might make it look like a strong sell right now compared to other companies in the Semiconductor industry in China, where around half of the companies have P/S ratios below 6.8x and even P/S below 3x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Thinkon Semiconductor Jinzhou

How Has Thinkon Semiconductor Jinzhou Performed Recently?

Thinkon Semiconductor Jinzhou could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting the poor revenue to reverse, justifying it's current high P/S.. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Thinkon Semiconductor Jinzhou.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Thinkon Semiconductor Jinzhou's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 14% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 46% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 152% as estimated by the lone analyst watching the company. With the industry only predicted to deliver 43%, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Thinkon Semiconductor Jinzhou's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Thinkon Semiconductor Jinzhou's P/S

Shares in Thinkon Semiconductor Jinzhou have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look into Thinkon Semiconductor Jinzhou shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for Thinkon Semiconductor Jinzhou (1 can't be ignored!) that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Thinkon Semiconductor Jinzhou might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688233

Thinkon Semiconductor Jinzhou

Engages in the research, development, production, and sale of monocrystalline silicon products for integrated circuit etching in China and internationally.

Excellent balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor