Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688233

Revenues Tell The Story For Thinkon Semiconductor Jinzhou Corp. (SHSE:688233) As Its Stock Soars 35%

Thinkon Semiconductor Jinzhou Corp. (SHSE:688233) shares have had a really impressive month, gaining 35% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 34% over that time.

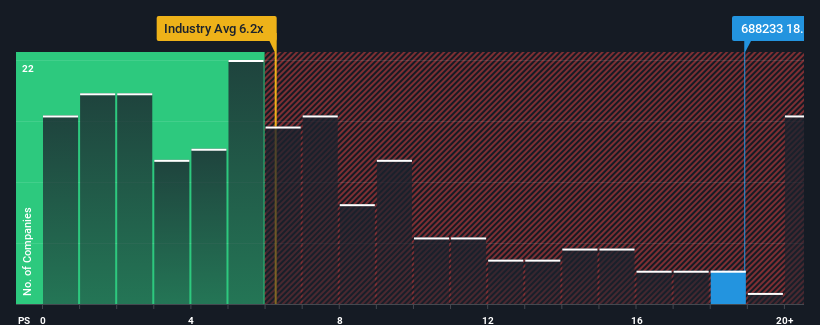

Following the firm bounce in price, Thinkon Semiconductor Jinzhou may be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 18.9x, when you consider almost half of the companies in the Semiconductor industry in China have P/S ratios under 6.2x and even P/S lower than 3x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Thinkon Semiconductor Jinzhou

What Does Thinkon Semiconductor Jinzhou's Recent Performance Look Like?

While the industry has experienced revenue growth lately, Thinkon Semiconductor Jinzhou's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to recover substantially, which has kept the P/S from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Thinkon Semiconductor Jinzhou will help you uncover what's on the horizon.Is There Enough Revenue Growth Forecasted For Thinkon Semiconductor Jinzhou?

The only time you'd be truly comfortable seeing a P/S as steep as Thinkon Semiconductor Jinzhou's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 49%. As a result, revenue from three years ago have also fallen 48% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 173% during the coming year according to the lone analyst following the company. Meanwhile, the rest of the industry is forecast to only expand by 36%, which is noticeably less attractive.

With this information, we can see why Thinkon Semiconductor Jinzhou is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Thinkon Semiconductor Jinzhou's P/S?

Shares in Thinkon Semiconductor Jinzhou have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look into Thinkon Semiconductor Jinzhou shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Thinkon Semiconductor Jinzhou (1 is concerning) you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Thinkon Semiconductor Jinzhou might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688233

Thinkon Semiconductor Jinzhou

Engages in the research, development, production, and sale of monocrystalline silicon products for integrated circuit etching in China and internationally.

Excellent balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor