- China

- /

- Semiconductors

- /

- SHSE:688223

Market Still Lacking Some Conviction On Jinko Solar Co., Ltd. (SHSE:688223)

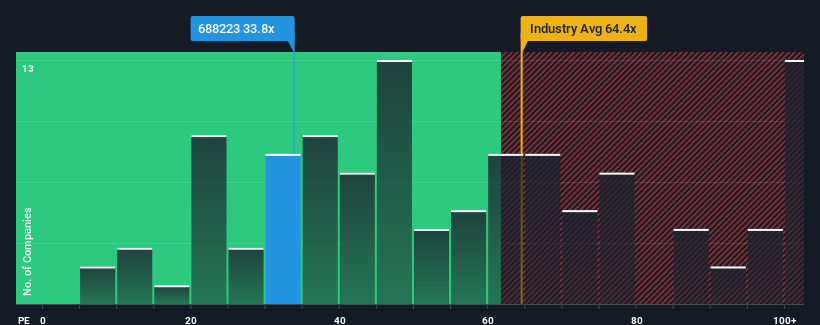

With a median price-to-earnings (or "P/E") ratio of close to 35x in China, you could be forgiven for feeling indifferent about Jinko Solar Co., Ltd.'s (SHSE:688223) P/E ratio of 33.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Jinko Solar has been struggling lately as its earnings have declined faster than most other companies. One possibility is that the P/E is moderate because investors think the company's earnings trend will eventually fall in line with most others in the market. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Jinko Solar

How Is Jinko Solar's Growth Trending?

The only time you'd be comfortable seeing a P/E like Jinko Solar's is when the company's growth is tracking the market closely.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 71%. Still, the latest three year period has seen an excellent 64% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 49% each year over the next three years. Meanwhile, the rest of the market is forecast to only expand by 21% per annum, which is noticeably less attractive.

In light of this, it's curious that Jinko Solar's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Jinko Solar's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

You should always think about risks. Case in point, we've spotted 2 warning signs for Jinko Solar you should be aware of, and 1 of them shouldn't be ignored.

You might be able to find a better investment than Jinko Solar. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688223

Jinko Solar

Engages in the design, development, production, and marketing of photovoltaic products and integrated clean energy solutions worldwide.

Flawless balance sheet and undervalued.

Market Insights

Community Narratives