Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688041

3 Stocks Estimated To Be Trading Below Fair Value In December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a period of economic uncertainty marked by interest rate cuts from the ECB and SNB, and with expectations for a similar move by the Fed, investors are left assessing opportunities amidst mixed performances across major indices. While growth stocks have recently outpaced value stocks, identifying undervalued equities can be particularly appealing in such fluctuating market conditions, offering potential for long-term gains when these stocks eventually align with their intrinsic value.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xiamen Bank (SHSE:601187) | CN¥5.61 | CN¥11.35 | 50.6% |

| Gaming Realms (AIM:GMR) | £0.36 | £0.72 | 49.8% |

| Hanwha Systems (KOSE:A272210) | ₩20650.00 | ₩41978.93 | 50.8% |

| Decisive Dividend (TSXV:DE) | CA$5.92 | CA$11.83 | 50% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP290.00 | CLP579.00 | 49.9% |

| ReadyTech Holdings (ASX:RDY) | A$3.05 | A$6.30 | 51.6% |

| Wetteri Oyj (HLSE:WETTERI) | €0.297 | €0.59 | 49.9% |

| Compagnia dei Caraibi (BIT:TIME) | €0.542 | €1.08 | 50% |

| Fnac Darty (ENXTPA:FNAC) | €29.45 | €58.67 | 49.8% |

| Suzhou Zelgen BiopharmaceuticalsLtd (SHSE:688266) | CN¥62.00 | CN¥126.28 | 50.9% |

Here's a peek at a few of the choices from the screener.

Hygon Information Technology (SHSE:688041)

Overview: Hygon Information Technology Co., Ltd. focuses on the research and development of computing chip products and systems, with a market cap of CN¥281.65 billion.

Operations: Hygon's revenue is primarily derived from its computing chip products and systems.

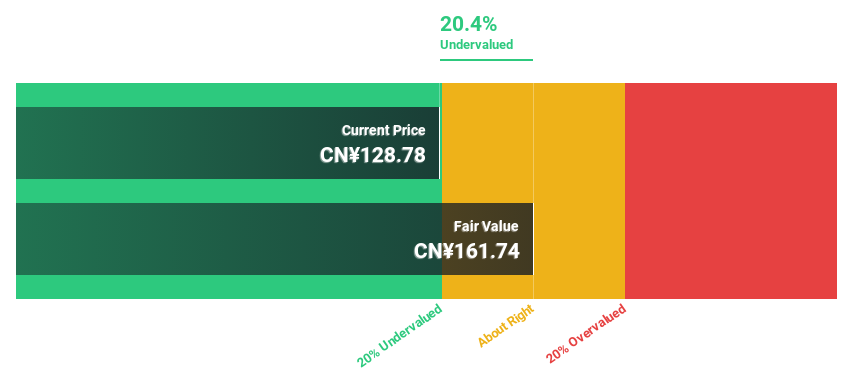

Estimated Discount To Fair Value: 20.4%

Hygon Information Technology is trading at CN¥128.78, below its estimated fair value of CN¥161.74, indicating it may be undervalued based on cash flows. Despite a highly volatile share price recently, the company reported substantial revenue growth to CN¥6.14 billion for the first nine months of 2024 and net income rose to CN¥1.53 billion from last year’s figures. Earnings are expected to grow significantly over the next three years, outpacing market averages in China.

- Our earnings growth report unveils the potential for significant increases in Hygon Information Technology's future results.

- Unlock comprehensive insights into our analysis of Hygon Information Technology stock in this financial health report.

BayCurrent Consulting (TSE:6532)

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market cap of ¥799.37 billion.

Operations: BayCurrent Consulting, Inc. generates revenue through its consulting services in Japan.

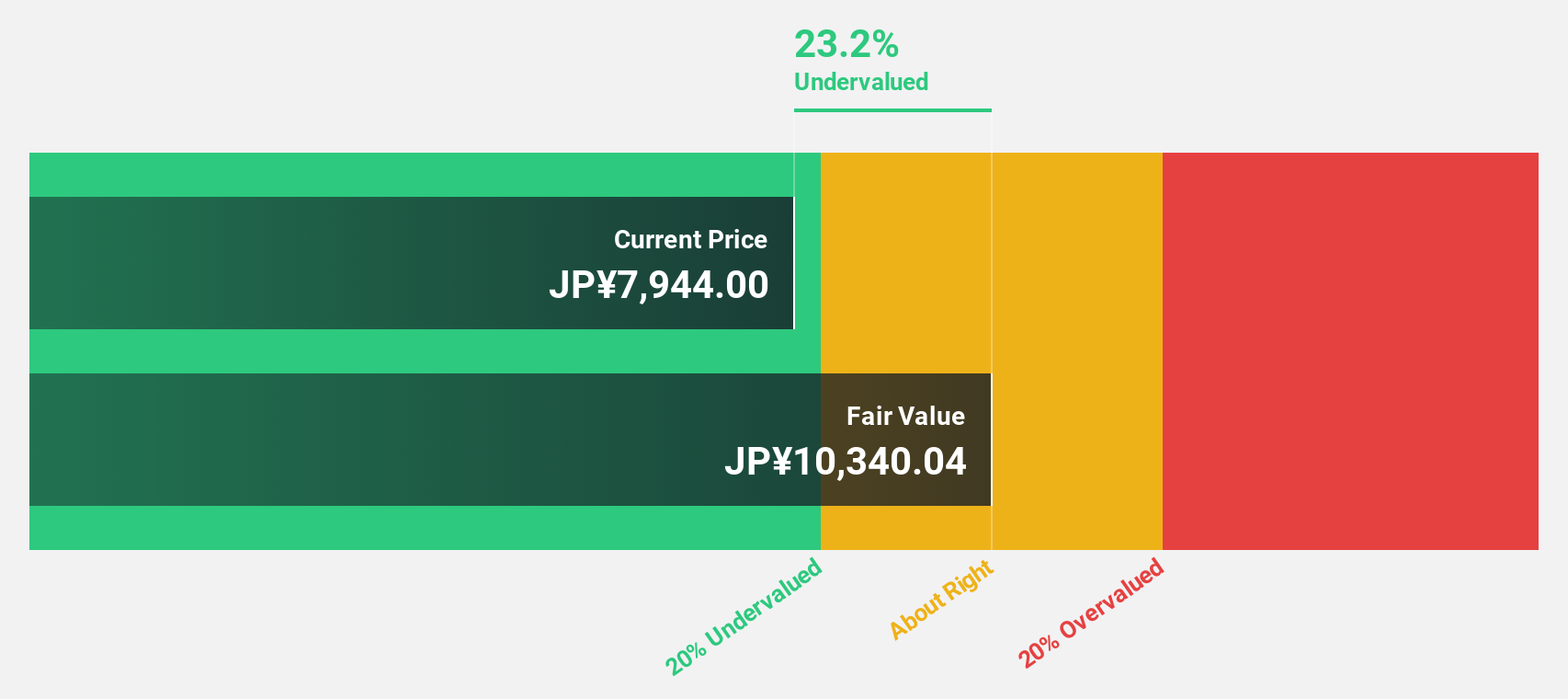

Estimated Discount To Fair Value: 41.9%

BayCurrent Consulting is trading at ¥5,392, considerably below its fair value estimate of ¥9,278.62, highlighting potential undervaluation based on cash flows. Despite earnings growing by 15.7% over the past year and forecasts predicting 19% annual growth—outpacing the Japanese market—revenue growth is expected to be slower than 20% annually. However, its return on equity is anticipated to be robust at 35% in three years, supporting a positive outlook amidst moderate revenue expansion expectations.

- Our comprehensive growth report raises the possibility that BayCurrent Consulting is poised for substantial financial growth.

- Take a closer look at BayCurrent Consulting's balance sheet health here in our report.

Kaori Heat Treatment (TWSE:8996)

Overview: Kaori Heat Treatment Co., Ltd. specializes in the research, development, manufacture, and sale of heat exchanger solutions across Taiwan, Asia, the United States, Europe, and internationally with a market cap of NT$30.14 billion.

Operations: The company's revenue is primarily derived from its Plate Heat Exchanger segment, generating NT$1.77 billion, and its Energy Conservation Product Segment, which includes Metal Products and Processing, contributing NT$2.14 billion.

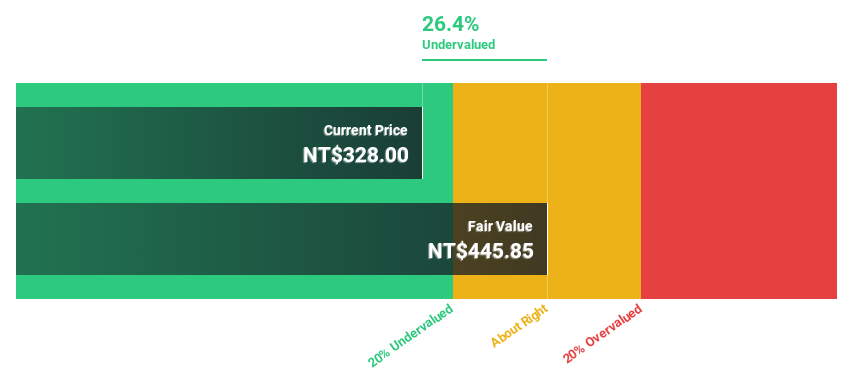

Estimated Discount To Fair Value: 26.4%

Kaori Heat Treatment Co., Ltd. is trading at NT$328, significantly below its fair value estimate of NT$445.85, suggesting undervaluation based on cash flows. Despite recent shareholder dilution and a volatile share price, the company anticipates robust earnings growth of 51.1% annually over the next three years—outpacing Taiwan's market average—and revenue growth of 40.9% per year. Analysts agree on a potential stock price increase by 20.8%, enhancing its investment appeal despite current challenges in sales performance.

- The growth report we've compiled suggests that Kaori Heat Treatment's future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Kaori Heat Treatment.

Seize The Opportunity

- Discover the full array of 885 Undervalued Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hygon Information Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688041

Hygon Information Technology

Engages in the research and development of computing chip products and systems in China.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor