Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Will Semiconductor Co., Ltd. (SHSE:603501) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Will Semiconductor's Debt?

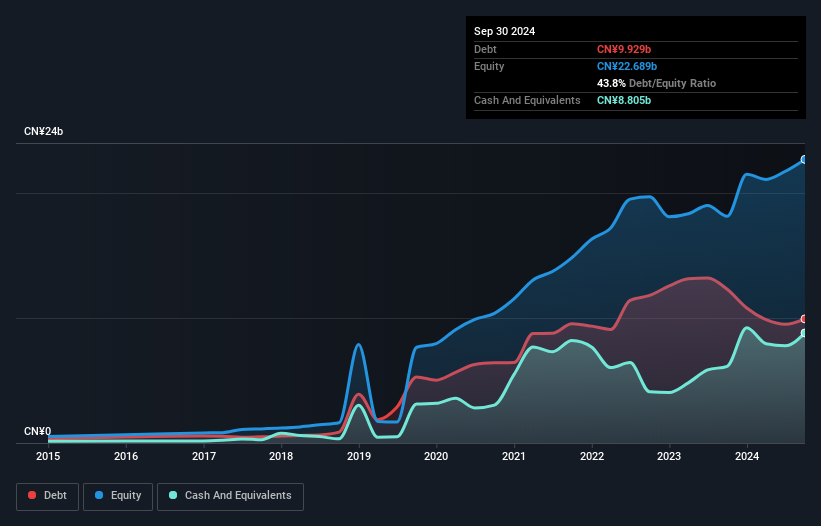

As you can see below, Will Semiconductor had CN¥9.93b of debt at September 2024, down from CN¥12.3b a year prior. However, it does have CN¥8.80b in cash offsetting this, leading to net debt of about CN¥1.12b.

A Look At Will Semiconductor's Liabilities

The latest balance sheet data shows that Will Semiconductor had liabilities of CN¥8.24b due within a year, and liabilities of CN¥7.46b falling due after that. Offsetting these obligations, it had cash of CN¥8.80b as well as receivables valued at CN¥4.53b due within 12 months. So it has liabilities totalling CN¥2.37b more than its cash and near-term receivables, combined.

Having regard to Will Semiconductor's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the CN¥163.0b company is short on cash, but still worth keeping an eye on the balance sheet. But either way, Will Semiconductor has virtually no net debt, so it's fair to say it does not have a heavy debt load!

Check out our latest analysis for Will Semiconductor

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Will Semiconductor has a low net debt to EBITDA ratio of only 0.36. And its EBIT easily covers its interest expense, being 77.6 times the size. So we're pretty relaxed about its super-conservative use of debt. It was also good to see that despite losing money on the EBIT line last year, Will Semiconductor turned things around in the last 12 months, delivering and EBIT of CN¥2.7b. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Will Semiconductor can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Happily for any shareholders, Will Semiconductor actually produced more free cash flow than EBIT over the last year. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

The good news is that Will Semiconductor's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Looking at the bigger picture, we think Will Semiconductor's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. Over time, share prices tend to follow earnings per share, so if you're interested in Will Semiconductor, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603501

OmniVision Integrated Circuits Group

OmniVision Integrated Circuits Group, Inc.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor