Advertisement

- China

- /

- Semiconductors

- /

- SHSE:603421

Qingdao Topscomm Communication INC.'s (SHSE:603421) Price Is Right But Growth Is Lacking After Shares Rocket 25%

Qingdao Topscomm Communication INC. (SHSE:603421) shares have had a really impressive month, gaining 25% after a shaky period beforehand. But the last month did very little to improve the 53% share price decline over the last year.

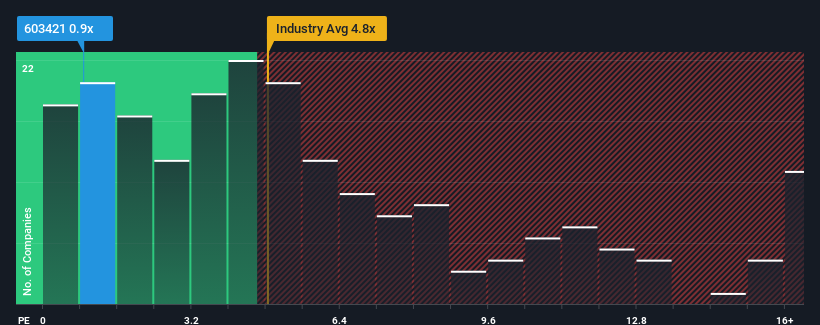

In spite of the firm bounce in price, Qingdao Topscomm Communication's price-to-sales (or "P/S") ratio of 0.9x might still make it look like a strong buy right now compared to the wider Semiconductor industry in China, where around half of the companies have P/S ratios above 4.8x and even P/S above 9x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Qingdao Topscomm Communication

How Qingdao Topscomm Communication Has Been Performing

Qingdao Topscomm Communication has been doing a good job lately as it's been growing revenue at a solid pace. It might be that many expect the respectable revenue performance to degrade substantially, which has repressed the P/S. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Qingdao Topscomm Communication will help you shine a light on its historical performance.Is There Any Revenue Growth Forecasted For Qingdao Topscomm Communication?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Qingdao Topscomm Communication's to be considered reasonable.

Retrospectively, the last year delivered a decent 8.6% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 72% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

This is in contrast to the rest of the industry, which is expected to grow by 36% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in consideration, it's easy to understand why Qingdao Topscomm Communication's P/S falls short of the mark set by its industry peers. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

The Bottom Line On Qingdao Topscomm Communication's P/S

Even after such a strong price move, Qingdao Topscomm Communication's P/S still trails the rest of the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Qingdao Topscomm Communication revealed its three-year revenue trends are contributing to its low P/S, given they look worse than current industry expectations. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

It is also worth noting that we have found 5 warning signs for Qingdao Topscomm Communication (1 is a bit unpleasant!) that you need to take into consideration.

If you're unsure about the strength of Qingdao Topscomm Communication's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao Topscomm Communication might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603421

Qingdao Topscomm Communication

Engages in the research and development, production, sale, and service of products in the field of power electronics and signal processing.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor