Advertisement

- China

- /

- General Merchandise and Department Stores

- /

- SZSE:301110

Qingmu Tec Co., Ltd.'s (SZSE:301110) P/E Is Still On The Mark Following 30% Share Price Bounce

Despite an already strong run, Qingmu Tec Co., Ltd. (SZSE:301110) shares have been powering on, with a gain of 30% in the last thirty days. The last month tops off a massive increase of 127% in the last year.

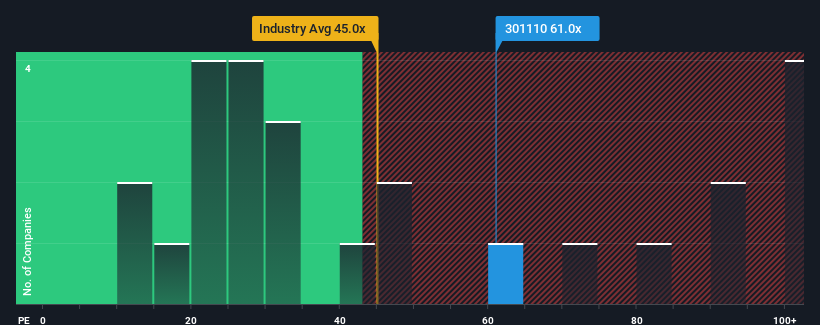

After such a large jump in price, Qingmu Tec may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 61x, since almost half of all companies in China have P/E ratios under 31x and even P/E's lower than 18x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Qingmu Tec has been doing quite well of late. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Qingmu Tec

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Qingmu Tec would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered an exceptional 79% gain to the company's bottom line. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 41% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the only analyst covering the company suggest earnings should grow by 118% over the next year. Meanwhile, the rest of the market is forecast to only expand by 38%, which is noticeably less attractive.

With this information, we can see why Qingmu Tec is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Qingmu Tec's P/E?

The strong share price surge has got Qingmu Tec's P/E rushing to great heights as well. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Qingmu Tec maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You need to take note of risks, for example - Qingmu Tec has 3 warning signs (and 2 which make us uncomfortable) we think you should know about.

Of course, you might also be able to find a better stock than Qingmu Tec. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Qingmu Tec might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301110

Excellent balance sheet slight.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor