Advertisement

- China

- /

- Specialty Stores

- /

- SZSE:002758

ZJAMP Group (SZSE:002758) Has More To Do To Multiply In Value Going Forward

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So, when we ran our eye over ZJAMP Group's (SZSE:002758) trend of ROCE, we liked what we saw.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on ZJAMP Group is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.15 = CN¥1.1b ÷ (CN¥20b - CN¥13b) (Based on the trailing twelve months to September 2023).

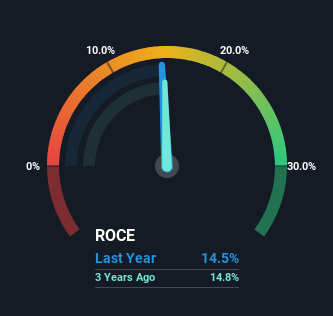

So, ZJAMP Group has an ROCE of 15%. On its own, that's a standard return, however it's much better than the 4.3% generated by the Specialty Retail industry.

View our latest analysis for ZJAMP Group

Historical performance is a great place to start when researching a stock so above you can see the gauge for ZJAMP Group's ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of ZJAMP Group.

So How Is ZJAMP Group's ROCE Trending?

While the returns on capital are good, they haven't moved much. The company has employed 44% more capital in the last three years, and the returns on that capital have remained stable at 15%. 15% is a pretty standard return, and it provides some comfort knowing that ZJAMP Group has consistently earned this amount. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

On a side note, ZJAMP Group's current liabilities are still rather high at 63% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

Our Take On ZJAMP Group's ROCE

In the end, ZJAMP Group has proven its ability to adequately reinvest capital at good rates of return. However, despite the favorable fundamentals, the stock has fallen 14% over the last three years, so there might be an opportunity here for astute investors. That's why we think it'd be worthwhile to look further into this stock given the fundamentals are appealing.

On a final note, we've found 2 warning signs for ZJAMP Group that we think you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if ZJAMP Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002758

ZJAMP Group

Engages in the production and sale of pesticides and fertilizers in China and internationally.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor