Advertisement

- China

- /

- Real Estate

- /

- SHSE:601512

Lacklustre Performance Is Driving China-Singapore Suzhou Industrial Park Development Group Co., Ltd.'s (SHSE:601512) Low P/E

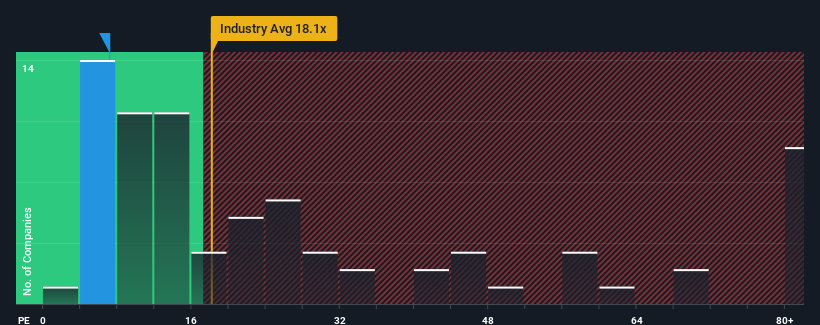

With a price-to-earnings (or "P/E") ratio of 7.1x China-Singapore Suzhou Industrial Park Development Group Co., Ltd. (SHSE:601512) may be sending very bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 30x and even P/E's higher than 55x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Recent times have been pleasing for China-Singapore Suzhou Industrial Park Development Group as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for China-Singapore Suzhou Industrial Park Development Group

Is There Any Growth For China-Singapore Suzhou Industrial Park Development Group?

In order to justify its P/E ratio, China-Singapore Suzhou Industrial Park Development Group would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a decent 11% gain to the company's bottom line. Pleasingly, EPS has also lifted 59% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 16% during the coming year according to the two analysts following the company. With the market predicted to deliver 41% growth , the company is positioned for a weaker earnings result.

In light of this, it's understandable that China-Singapore Suzhou Industrial Park Development Group's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that China-Singapore Suzhou Industrial Park Development Group maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with China-Singapore Suzhou Industrial Park Development Group, and understanding should be part of your investment process.

Of course, you might also be able to find a better stock than China-Singapore Suzhou Industrial Park Development Group. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601512

China-Singapore Suzhou Industrial Park Development Group

China-Singapore Suzhou Industrial Park Development Group Co., Ltd.

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor