Shenyang Xingqi Pharmaceutical Co.,Ltd. (SZSE:300573) Looks Just Right With A 26% Price Jump

Shenyang Xingqi Pharmaceutical Co.,Ltd. (SZSE:300573) shareholders would be excited to see that the share price has had a great month, posting a 26% gain and recovering from prior weakness. The last month tops off a massive increase of 113% in the last year.

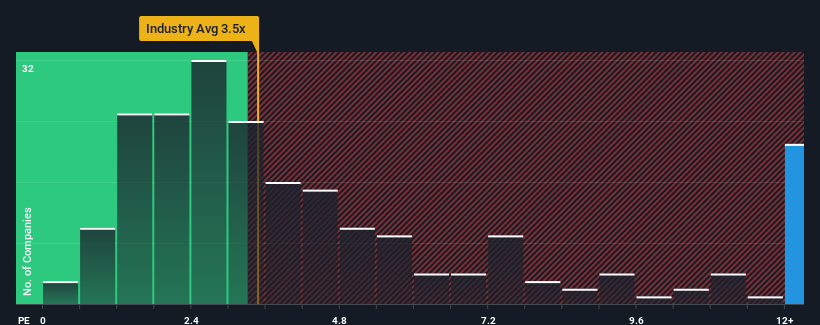

After such a large jump in price, when almost half of the companies in China's Pharmaceuticals industry have price-to-sales ratios (or "P/S") below 3.5x, you may consider Shenyang Xingqi PharmaceuticalLtd as a stock not worth researching with its 18.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for Shenyang Xingqi PharmaceuticalLtd

How Shenyang Xingqi PharmaceuticalLtd Has Been Performing

Recent times haven't been great for Shenyang Xingqi PharmaceuticalLtd as its revenue has been rising slower than most other companies. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Shenyang Xingqi PharmaceuticalLtd's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Shenyang Xingqi PharmaceuticalLtd's to be considered reasonable.

Retrospectively, the last year delivered a decent 7.0% gain to the company's revenues. The latest three year period has also seen an excellent 124% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 39% over the next year. With the industry only predicted to deliver 18%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Shenyang Xingqi PharmaceuticalLtd's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Shenyang Xingqi PharmaceuticalLtd's P/S

The strong share price surge has lead to Shenyang Xingqi PharmaceuticalLtd's P/S soaring as well. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Shenyang Xingqi PharmaceuticalLtd's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Before you settle on your opinion, we've discovered 1 warning sign for Shenyang Xingqi PharmaceuticalLtd that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300573

Shenyang Xingqi PharmaceuticalLtd

Engages in the research and development, production, and sale of ophthalmic medications in the People’s Republic of China.

Outstanding track record with flawless balance sheet.

Market Insights

Community Narratives