Advertisement

- China

- /

- Life Sciences

- /

- SHSE:688131

After Leaping 27% Shanghai Haoyuan Chemexpress Co., Ltd. (SHSE:688131) Shares Are Not Flying Under The Radar

Those holding Shanghai Haoyuan Chemexpress Co., Ltd. (SHSE:688131) shares would be relieved that the share price has rebounded 27% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. But the last month did very little to improve the 50% share price decline over the last year.

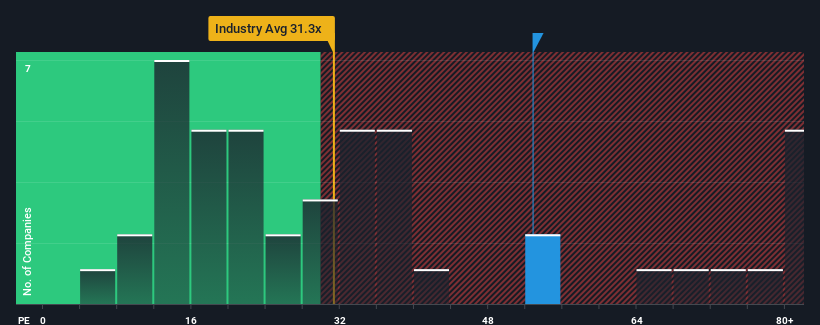

After such a large jump in price, Shanghai Haoyuan Chemexpress may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 52.8x, since almost half of all companies in China have P/E ratios under 31x and even P/E's lower than 19x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Shanghai Haoyuan Chemexpress hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Shanghai Haoyuan Chemexpress

Does Growth Match The High P/E?

In order to justify its P/E ratio, Shanghai Haoyuan Chemexpress would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 39% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 31% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 62% as estimated by the four analysts watching the company. With the market only predicted to deliver 40%, the company is positioned for a stronger earnings result.

With this information, we can see why Shanghai Haoyuan Chemexpress is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

The strong share price surge has got Shanghai Haoyuan Chemexpress' P/E rushing to great heights as well. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Shanghai Haoyuan Chemexpress maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Shanghai Haoyuan Chemexpress you should know about.

If you're unsure about the strength of Shanghai Haoyuan Chemexpress' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688131

Shanghai Haoyuan Chemexpress

Researches, develops, and manufactures pharmaceutical intermediates and small molecule drugs.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor