Advertisement

Guobang Pharma Ltd. (SHSE:605507) Analysts Just Cut Their EPS Forecasts Substantially

The analysts covering Guobang Pharma Ltd. (SHSE:605507) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously. At CN¥18.61, shares are up 4.6% in the past 7 days. Investors could be forgiven for changing their mind on the business following the downgrade; but it's not clear if the revised forecasts will lead to selling activity.

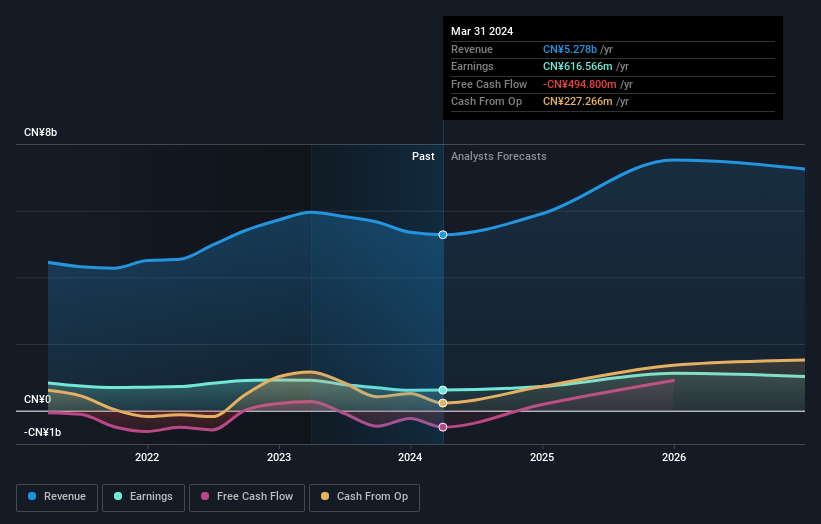

Following the downgrade, the current consensus from Guobang Pharma's twin analysts is for revenues of CN¥5.9b in 2024 which - if met - would reflect a decent 12% increase on its sales over the past 12 months. Per-share earnings are expected to grow 16% to CN¥1.29. Previously, the analysts had been modelling revenues of CN¥7.1b and earnings per share (EPS) of CN¥1.77 in 2024. Indeed, we can see that the analysts are a lot more bearish about Guobang Pharma's prospects, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Guobang Pharma

Analysts made no major changes to their price target of CN¥23.00, suggesting the downgrades are not expected to have a long-term impact on Guobang Pharma's valuation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We can infer from the latest estimates that forecasts expect a continuation of Guobang Pharma'shistorical trends, as the 12% annualised revenue growth to the end of 2024 is roughly in line with the 10% annual revenue growth over the past three years. Juxtapose this against our data, which suggests that other companies (with analyst coverage) in the industry are forecast to see their revenues grow 13% per year. So although Guobang Pharma is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on Guobang Pharma after the downgrade.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Guobang Pharma going out as far as 2026, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:605507

Guobang Pharma

Engages in the research, development, production, and sale of products in the pharmaceutical and veterinary industries.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor