Advertisement

Why Investors Shouldn't Be Surprised By Hubei Jumpcan Pharmaceutical Co., Ltd.'s (SHSE:600566) 26% Share Price Plunge

Unfortunately for some shareholders, the Hubei Jumpcan Pharmaceutical Co., Ltd. (SHSE:600566) share price has dived 26% in the last thirty days, prolonging recent pain. The recent drop has obliterated the annual return, with the share price now down 4.9% over that longer period.

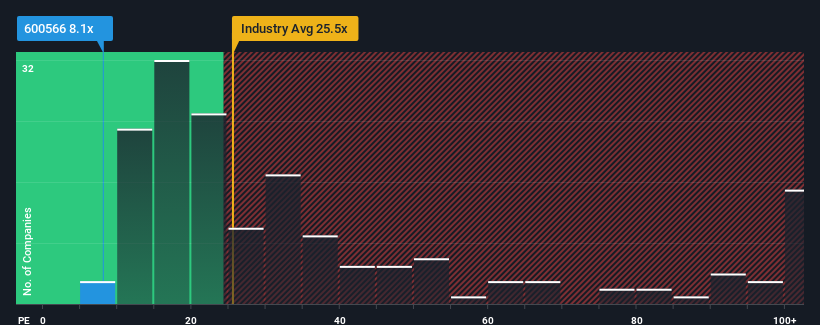

In spite of the heavy fall in price, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 27x, you may still consider Hubei Jumpcan Pharmaceutical as a highly attractive investment with its 8.1x P/E ratio. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Hubei Jumpcan Pharmaceutical has been doing quite well of late. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for Hubei Jumpcan Pharmaceutical

How Is Hubei Jumpcan Pharmaceutical's Growth Trending?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Hubei Jumpcan Pharmaceutical's to be considered reasonable.

Retrospectively, the last year delivered a decent 11% gain to the company's bottom line. This was backed up an excellent period prior to see EPS up by 84% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 10% per year as estimated by the three analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 20% per annum, which is noticeably more attractive.

With this information, we can see why Hubei Jumpcan Pharmaceutical is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Having almost fallen off a cliff, Hubei Jumpcan Pharmaceutical's share price has pulled its P/E way down as well. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Hubei Jumpcan Pharmaceutical's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Hubei Jumpcan Pharmaceutical that you should be aware of.

If you're unsure about the strength of Hubei Jumpcan Pharmaceutical's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Hubei Jumpcan Pharmaceutical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600566

Hubei Jumpcan Pharmaceutical

Engages in the research, development, manufacturing, and trading of Chinese traditional medicines, western medicines, daily use chemical based Chinese traditional medicines, and Chinese medicine health products in China.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets