Advertisement

- China

- /

- Entertainment

- /

- SZSE:300052

Subdued Growth No Barrier To Shenzhen Zqgame Co., Ltd (SZSE:300052) With Shares Advancing 52%

The Shenzhen Zqgame Co., Ltd (SZSE:300052) share price has done very well over the last month, posting an excellent gain of 52%. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 12% in the last twelve months.

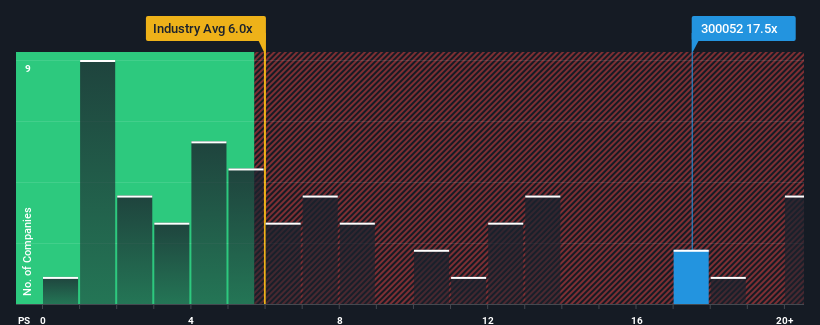

After such a large jump in price, you could be forgiven for thinking Shenzhen Zqgame is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 17.5x, considering almost half the companies in China's Entertainment industry have P/S ratios below 6x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Shenzhen Zqgame

How Has Shenzhen Zqgame Performed Recently?

Recent times haven't been great for Shenzhen Zqgame as its revenue has been rising slower than most other companies. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Shenzhen Zqgame's future stacks up against the industry? In that case, our free report is a great place to start.How Is Shenzhen Zqgame's Revenue Growth Trending?

Shenzhen Zqgame's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.1% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 23% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 20% as estimated by the one analyst watching the company. With the industry predicted to deliver 27% growth, the company is positioned for a weaker revenue result.

In light of this, it's alarming that Shenzhen Zqgame's P/S sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Final Word

Shares in Shenzhen Zqgame have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

It comes as a surprise to see Shenzhen Zqgame trade at such a high P/S given the revenue forecasts look less than stellar. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

You need to take note of risks, for example - Shenzhen Zqgame has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about.

If you're unsure about the strength of Shenzhen Zqgame's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300052

Shenzhen Zqgame

Engages in the development, operation, and distribution of online games in China.

Adequate balance sheet with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor