Advertisement

- Singapore

- /

- Real Estate

- /

- SGX:Z59

Deceuninck And Two Other Promising Penny Stocks To Watch

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of tariff uncertainties and fluctuating economic indicators, investors are keenly observing potential opportunities amidst the broader market dynamics. Penny stocks, a term that may feel somewhat antiquated, continue to hold relevance as they often represent smaller or newer companies with untapped growth potential. In this article, we explore three intriguing penny stocks that stand out for their financial resilience and growth prospects, offering investors a chance to discover under-the-radar opportunities in today's market landscape.

Top 10 Penny Stocks

| Name | Share Price | Market Cap | Financial Health Rating |

| Bosideng International Holdings (SEHK:3998) | HK$3.85 | HK$44.77B | ★★★★★★ |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.53 | MYR2.73B | ★★★★★★ |

| Polar Capital Holdings (AIM:POLR) | £4.945 | £476.68M | ★★★★★★ |

| Warpaint London (AIM:W7L) | £3.99 | £321.93M | ★★★★★★ |

| Datasonic Group Berhad (KLSE:DSONIC) | MYR0.33 | MYR959.84M | ★★★★★★ |

| Begbies Traynor Group (AIM:BEG) | £0.934 | £148.85M | ★★★★★★ |

| Hil Industries Berhad (KLSE:HIL) | MYR0.85 | MYR283.81M | ★★★★★★ |

| MGB Berhad (KLSE:MGB) | MYR0.70 | MYR414.16M | ★★★★★★ |

| Lever Style (SEHK:1346) | HK$1.13 | HK$717.31M | ★★★★★★ |

| Embark Early Education (ASX:EVO) | A$0.79 | A$144.95M | ★★★★☆☆ |

Click here to see the full list of 5,706 stocks from our Penny Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

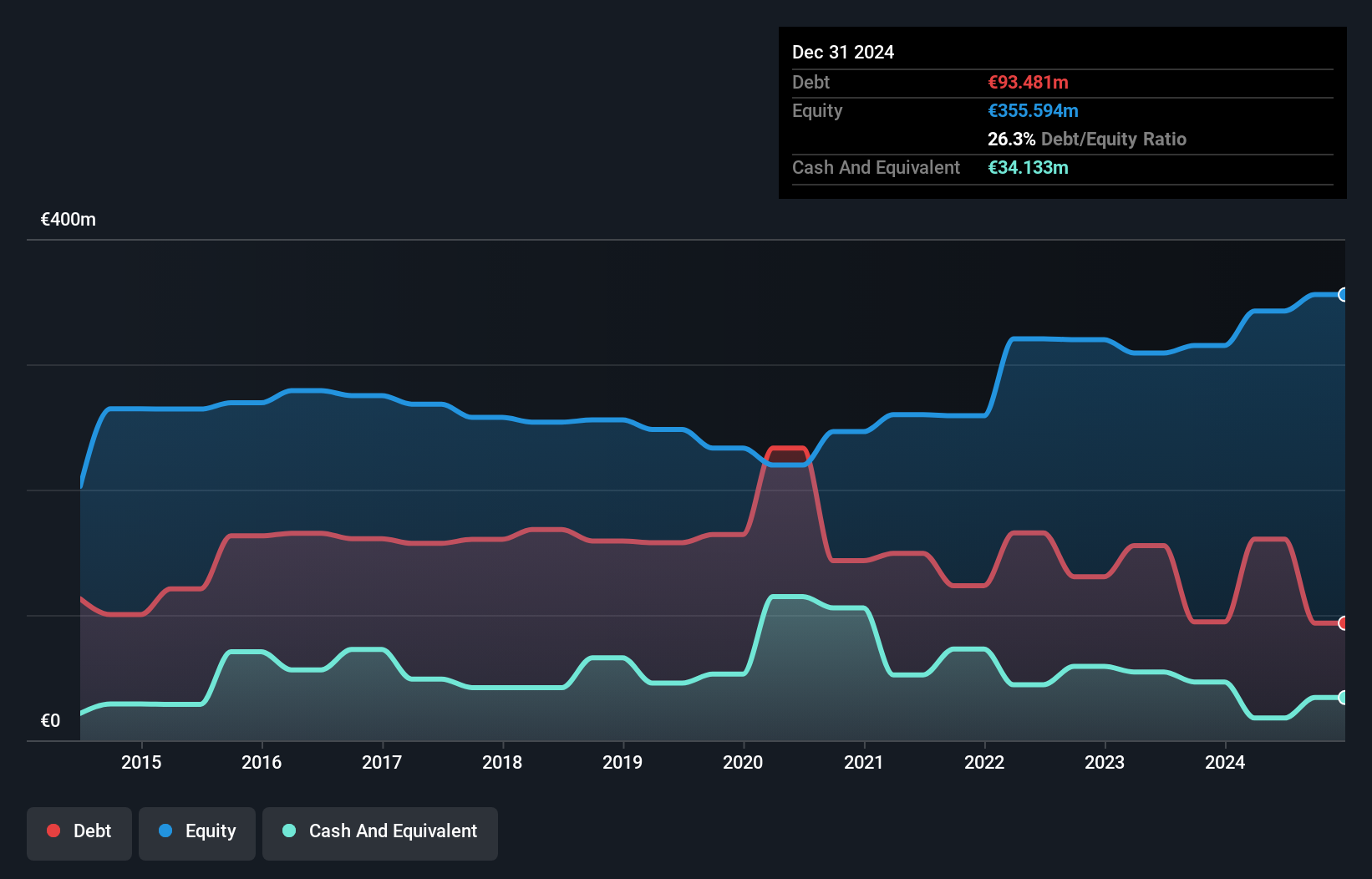

Deceuninck (ENXTBR:DECB)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Deceuninck NV is involved in the design, manufacture, recycling, and distribution of multi-material window, door, and building solutions across Europe, North America, Turkey, and other international markets with a market cap of €330.76 million.

Operations: The company's revenue is primarily derived from its Window and Door Systems segment, which accounts for €788.34 million, followed by Home Protection at €44.13 million and Outdoor Living at €27.98 million.

Market Cap: €330.76M

Deceuninck NV, with a market cap of €330.76 million, has faced financial challenges recently, including a significant €19.7 million one-off loss impacting its latest results. Despite past profit growth averaging 13.8% annually over five years, the company experienced negative earnings growth last year and reduced net profit margins to 0.2%. While trading at a good value relative to peers and industry, Deceuninck's high debt levels are concerning, though operating cash flow covers debt well at 39.6%. The management team is relatively new with an average tenure of 1.1 years, indicating potential for strategic shifts ahead.

- Jump into the full analysis health report here for a deeper understanding of Deceuninck.

- Learn about Deceuninck's future growth trajectory here.

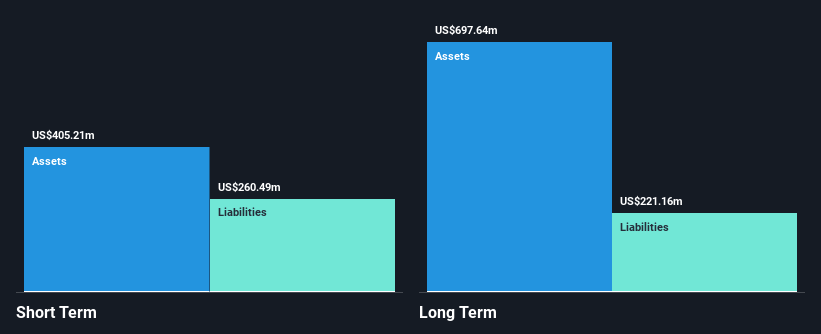

Yoma Strategic Holdings (SGX:Z59)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Yoma Strategic Holdings Ltd. is an investment holding company operating in real estate, motor, leasing, mobile financial services, food and beverages, and other investments across Singapore, Myanmar, and the People's Republic of China with a market cap of SGD188.72 million.

Operations: The company's revenue segments include Myanmar - Leasing ($7.83 million), Yoma F&B in Myanmar ($30.52 million), Investments across Myanmar/PRC ($7.92 million), Yoma Land Services in Myanmar ($16.54 million), Yoma Land Development in Myanmar ($99.09 million), Mobile Financial Services in Myanmar ($38.67 million), and Yoma Motors excluding Financial Services in Myanmar ($10.07 million).

Market Cap: SGD188.72M

Yoma Strategic Holdings Ltd., with a market cap of SGD188.72 million, has transitioned to profitability in the past year, driven by diverse revenue streams across Myanmar and China. However, its recent financials were notably impacted by a one-off gain of $42.9M, complicating earnings comparisons. The company's short-term assets ($405.2M) comfortably cover its liabilities, and debt management appears prudent with a net debt to equity ratio of 11.8%. Despite stable weekly volatility at 10%, its share price remains highly volatile over the past three months. While interest coverage is low at 2.1x EBIT, operating cash flow adequately covers debt obligations at 29.8%.

- Dive into the specifics of Yoma Strategic Holdings here with our thorough balance sheet health report.

- Gain insights into Yoma Strategic Holdings' historical outcomes by reviewing our past performance report.

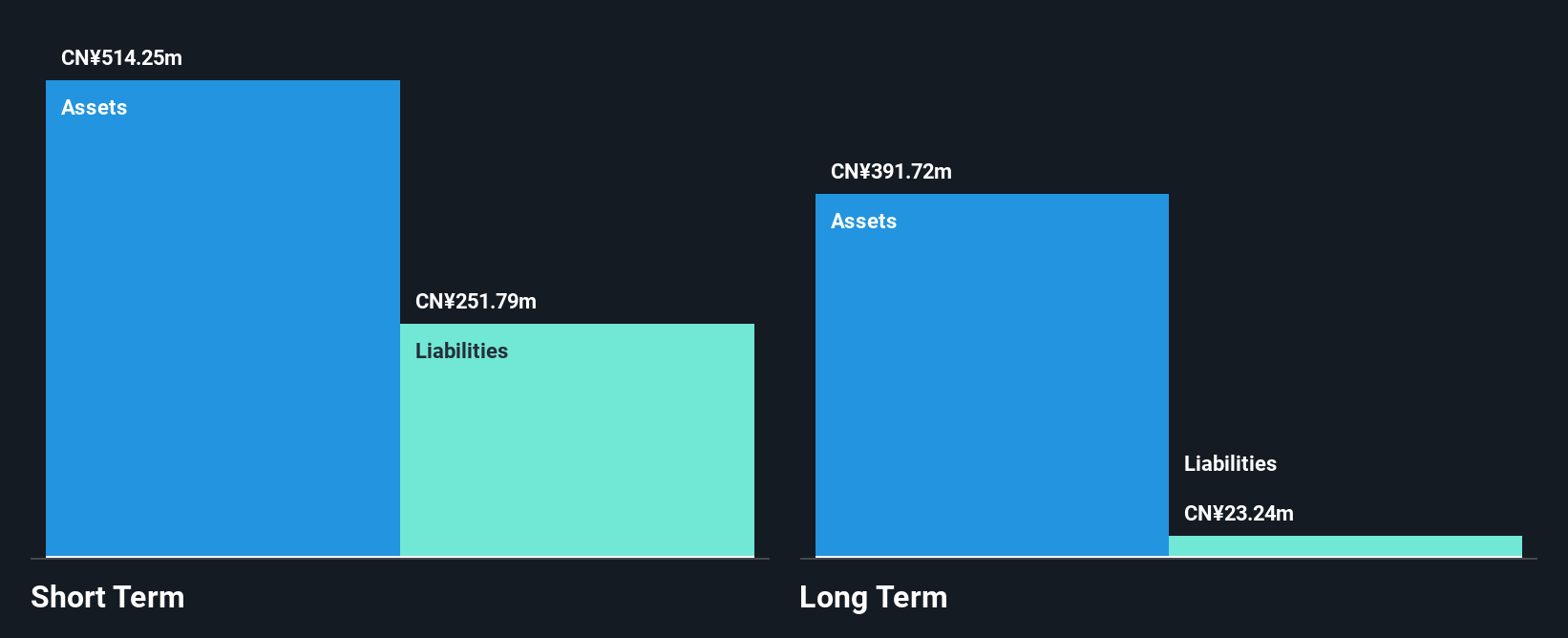

Zhejiang Juli Culture DevelopmentLtd (SZSE:002247)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Zhejiang Juli Culture Development Co., Ltd. operates in the cultural industry and has a market capitalization of CN¥2.31 billion.

Operations: No revenue segments have been reported for the company.

Market Cap: CN¥2.31B

Zhejiang Juli Culture Development Co., Ltd. has shown significant financial improvement, becoming profitable this year with a high Return on Equity of 36%. The company is debt-free, enhancing its financial stability, and its short-term assets (CN¥596.7M) exceed both short-term (CN¥333.9M) and long-term liabilities (CN¥46.5M). Despite being pre-revenue in the cultural industry, it has maintained a stable weekly volatility of 8%, indicating consistent performance. Its Price-To-Earnings ratio of 10.5x suggests potential value compared to the broader Chinese market average of 37.1x, though investors should consider the high level of non-cash earnings reported.

- Unlock comprehensive insights into our analysis of Zhejiang Juli Culture DevelopmentLtd stock in this financial health report.

- Review our historical performance report to gain insights into Zhejiang Juli Culture DevelopmentLtd's track record.

Next Steps

- Navigate through the entire inventory of 5,706 Penny Stocks here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:Z59

Yoma Strategic Holdings

An investment holding company, engages in the real estate, motor, leasing, mobile financial, food and beverages, and investment businesses in Singapore, Myanmar, and the People’s Republic of China.

Adequate balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.6% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|14.9% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.2% undervalued

AG

Community Contributor