As global markets navigate a landscape marked by easing trade tensions and mixed economic signals, investors are increasingly turning their attention to Asia's dynamic economies. In this environment, dividend stocks can offer a compelling blend of income and stability, making them an attractive option for those seeking to balance growth with resilience amidst ongoing market fluctuations.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Wuliangye YibinLtd (SZSE:000858) | 4.92% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.43% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.85% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 4.19% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.17% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.54% | ★★★★★★ |

| E J Holdings (TSE:2153) | 4.97% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.49% | ★★★★★★ |

| Soliton Systems K.K (TSE:3040) | 4.12% | ★★★★★★ |

| Japan Excellent (TSE:8987) | 4.39% | ★★★★★★ |

Click here to see the full list of 1226 stocks from our Top Asian Dividend Stocks screener.

Let's dive into some prime choices out of the screener.

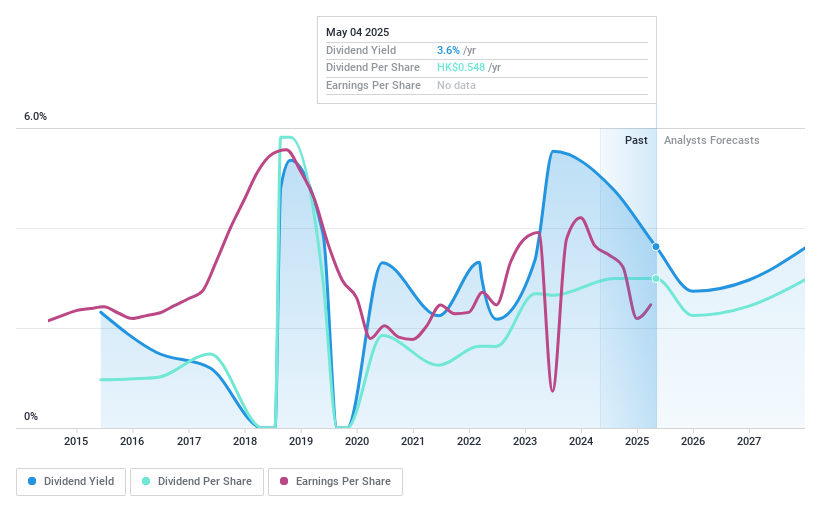

Yangtze Optical Fibre And Cable Limited (SEHK:6869)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Yangtze Optical Fibre And Cable Joint Stock Limited Company produces and sells optical fiber preforms, optical fibers, optical fiber cables, and integrated solutions both in China and internationally, with a market cap of HK$19.44 billion.

Operations: Yangtze Optical Fibre And Cable Joint Stock Limited Company generates revenue from the production and sale of optical fiber preforms, optical fibers, optical fiber cables, and integrated solutions.

Dividend Yield: 3.6%

Yangtze Optical Fibre And Cable Limited's dividend payments have been volatile over the past decade, though they are covered by earnings and cash flows with a payout ratio of 39.2%. Despite trading at a good value compared to peers, its dividend yield of 3.63% is low relative to top payers in Hong Kong. Recent financials show improved net income for Q1 2025 at CNY 151.7 million, but profit margins have declined year-over-year.

- Dive into the specifics of Yangtze Optical Fibre And Cable Limited here with our thorough dividend report.

- Our comprehensive valuation report raises the possibility that Yangtze Optical Fibre And Cable Limited is priced lower than what may be justified by its financials.

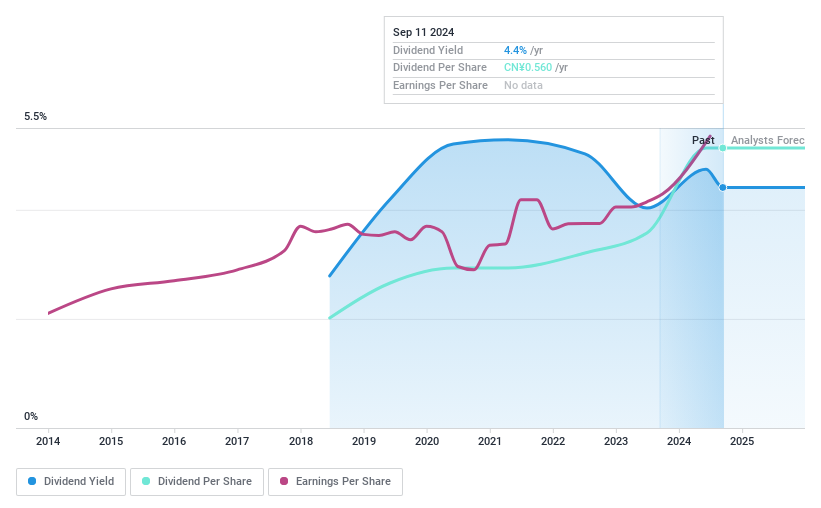

Shandong Publishing&MediaLtd (SHSE:601019)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Shandong Publishing&Media Co., Ltd, with a market cap of CN¥20.49 billion, operates in China through its subsidiaries by publishing textbooks, supplementary materials, general books, periodicals, electronic audio-visual products, and digital products.

Operations: In 2022, Shandong Publishing&Media Ltd generated revenue from the publication of textbooks and supplementary materials (CN¥7.32 billion), general books (CN¥1.65 billion), periodicals (CN¥1.15 billion), electronic audio-visual products (CN¥0.45 billion), and digital products (CN¥0.31 billion).

Dividend Yield: 3.2%

Shandong Publishing&Media Ltd. offers a dividend yield of 3.16%, placing it among the top 25% of dividend payers in China, though its payments have been volatile over the past seven years. Despite this instability, dividends are well-covered by earnings and cash flows with payout ratios of 47% and 54.4%, respectively. Recent Q1 results show improved net income at CNY 323.28 million, yet profit margins have decreased from last year’s figures.

- Click to explore a detailed breakdown of our findings in Shandong Publishing&MediaLtd's dividend report.

- Our valuation report unveils the possibility Shandong Publishing&MediaLtd's shares may be trading at a discount.

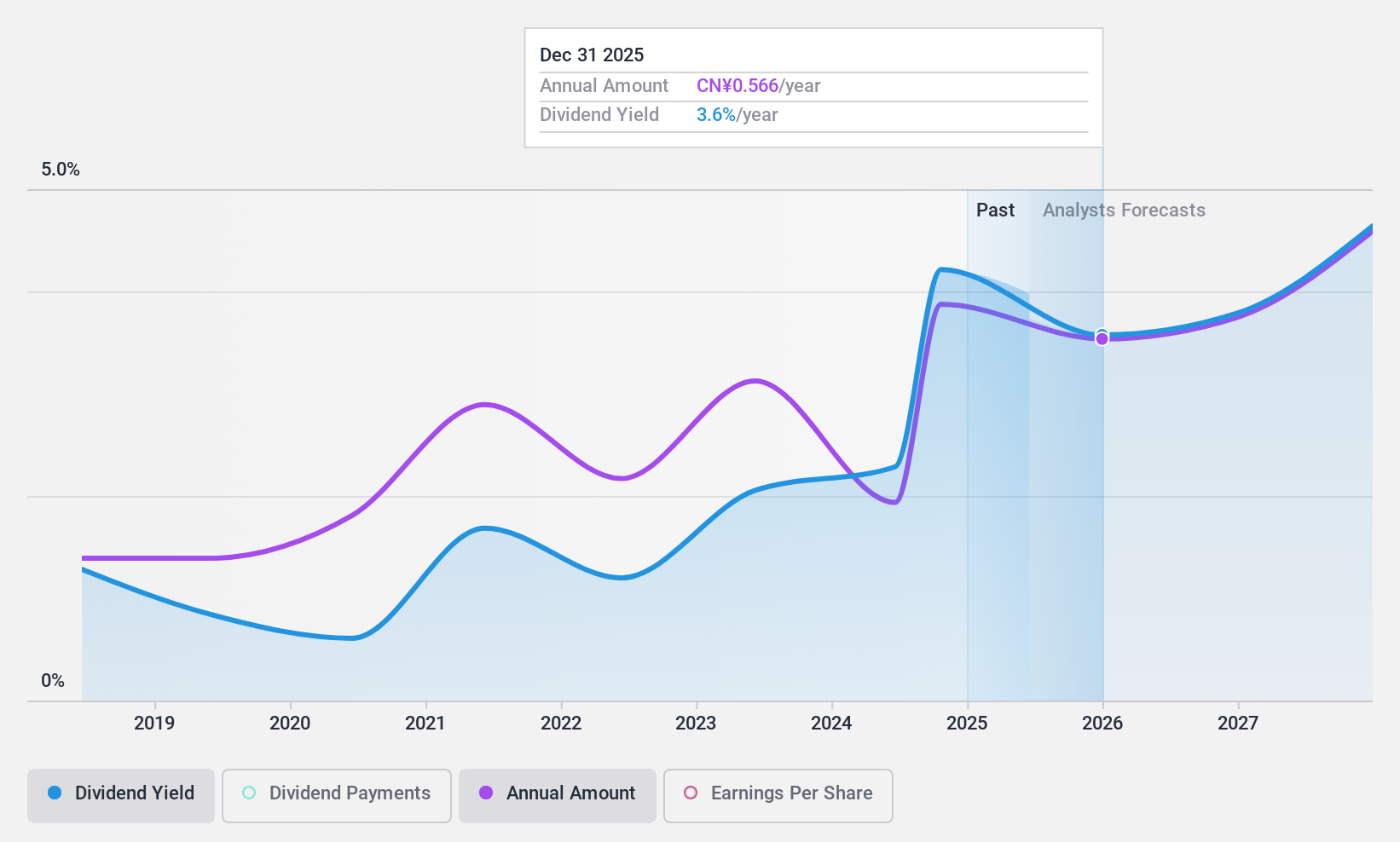

DaShenLin Pharmaceutical Group (SHSE:603233)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: DaShenLin Pharmaceutical Group Co., Ltd. operates in China, focusing on the manufacturing, wholesale, and retail of pharmaceutical products with a market cap of CN¥21.55 billion.

Operations: DaShenLin Pharmaceutical Group Co., Ltd. generates revenue through its operations in the manufacturing, wholesale, and retail sectors of pharmaceutical products within the Chinese market.

Dividend Yield: 3.3%

DaShenLin Pharmaceutical Group's dividend yield of 3.28% ranks in the top 25% of Chinese payers, but its seven-year track record is marked by volatility. Despite this, dividends are supported by earnings and cash flows with payout ratios of 82.8% and 43.3%, respectively. Recent Q1 results indicate sales growth to CNY 6,956 million and net income improvement to CNY 460 million from the previous year, though annual net income declined in 2024 compared to 2023.

- Click here and access our complete dividend analysis report to understand the dynamics of DaShenLin Pharmaceutical Group.

- Insights from our recent valuation report point to the potential undervaluation of DaShenLin Pharmaceutical Group shares in the market.

Next Steps

- Discover the full array of 1226 Top Asian Dividend Stocks right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Shandong Publishing&MediaLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:601019

Shandong Publishing&MediaLtd

Engages in the publication of textbooks and supplementary materials, general books, periodicals, electronic audio-visual products, and digital products in China.

Flawless balance sheet average dividend payer.

Market Insights

Community Narratives